Two contemporaneous articles (dated June 9–10, 1931) report the Madison State Bank 'shut their doors' / 'closed today' to 'conserve assets.' No mention of a depositor run is given; the bank suspended and appears to have closed. The articles do not mention a receiver or reopening.

Events (1)

1.June 9, 1931Suspension

Cause

Voluntary Liquidation

Cause Details

Directors announced the bank 'shut their doors' to 'conserve assets' (voluntary suspension/closure).

Newspaper Excerpt

...Madison State Bank said they had shut their doors to conserve assets.

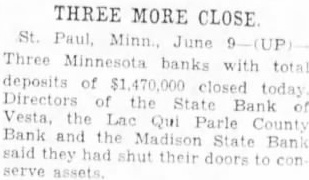

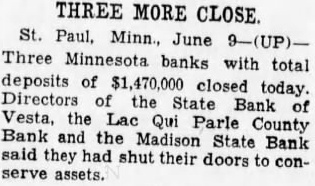

THREE MORE CLOSE St. Paul, Minn June 9. Three Minnesota banks with total deposits of $1. 170,000 closed today Directors of the State Bank of Vesta, the Lac Qui Parle County Bank and the Madison State Bank said they had shut their doors to serve

THREE MORE CLOSE Three Minnesota banks with total deposits of $1,470,000 closed today. Directors of the State Bank of Vesta, the Lac Qui Parle County Bank and the Madison State Bank said they had shut their doors to conserve assets.