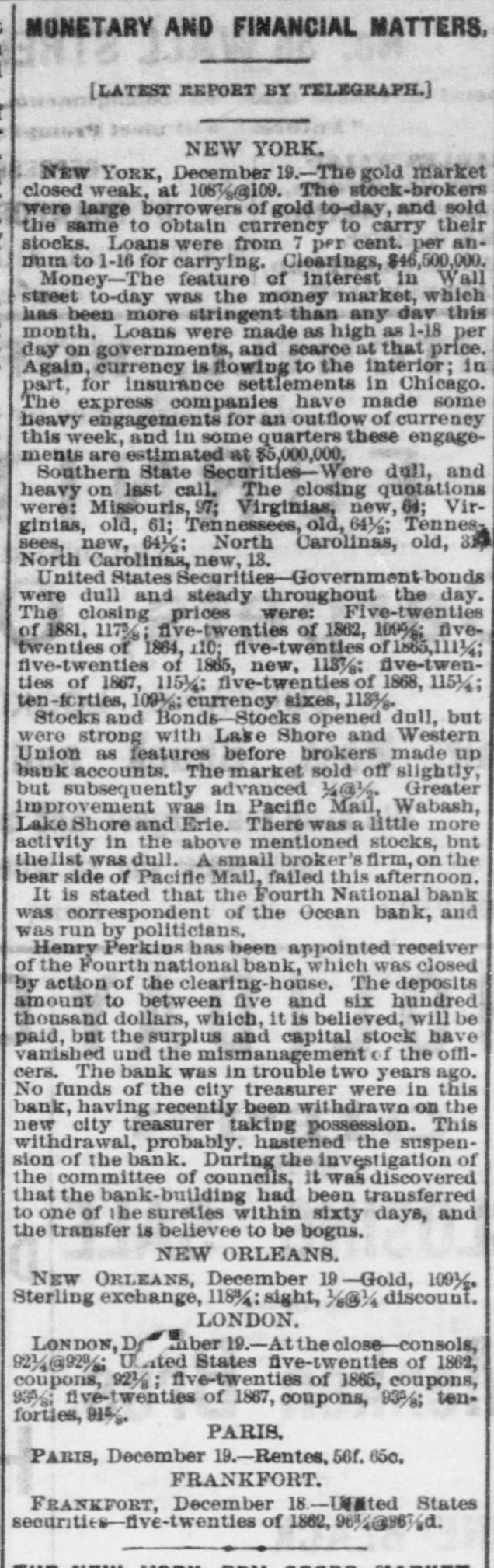

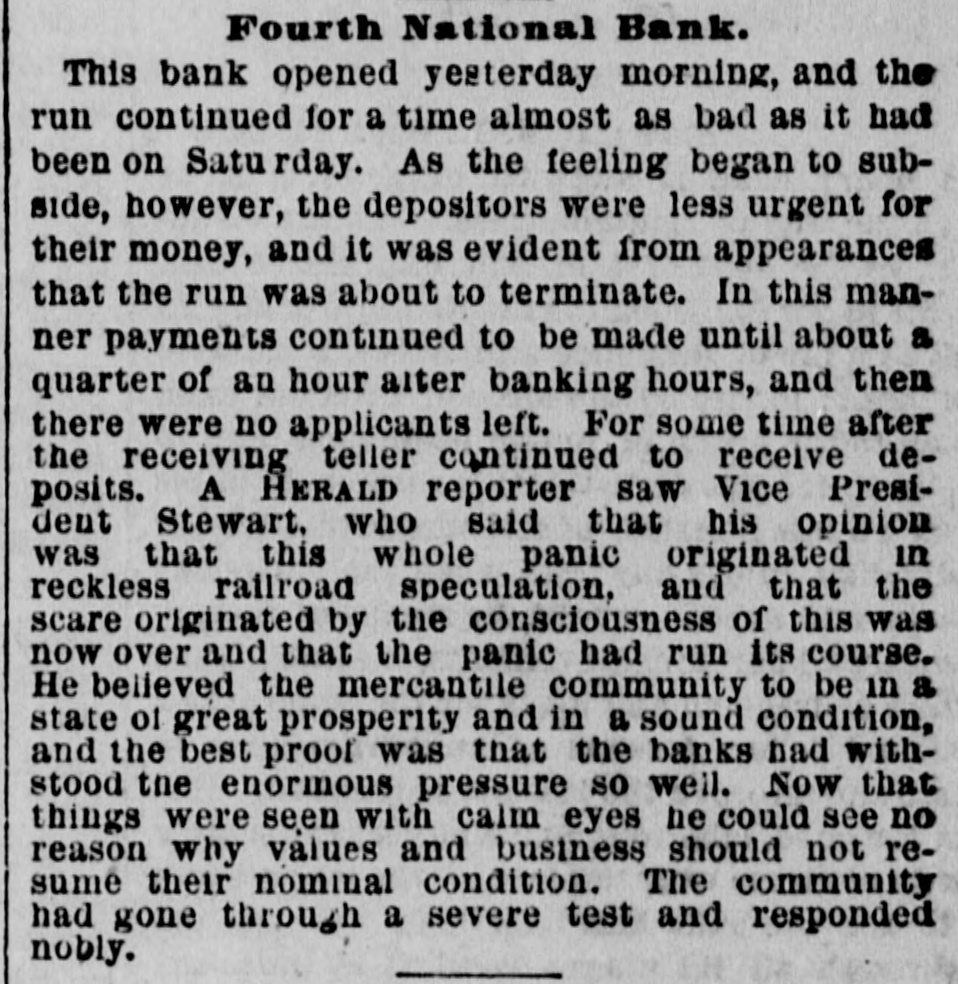

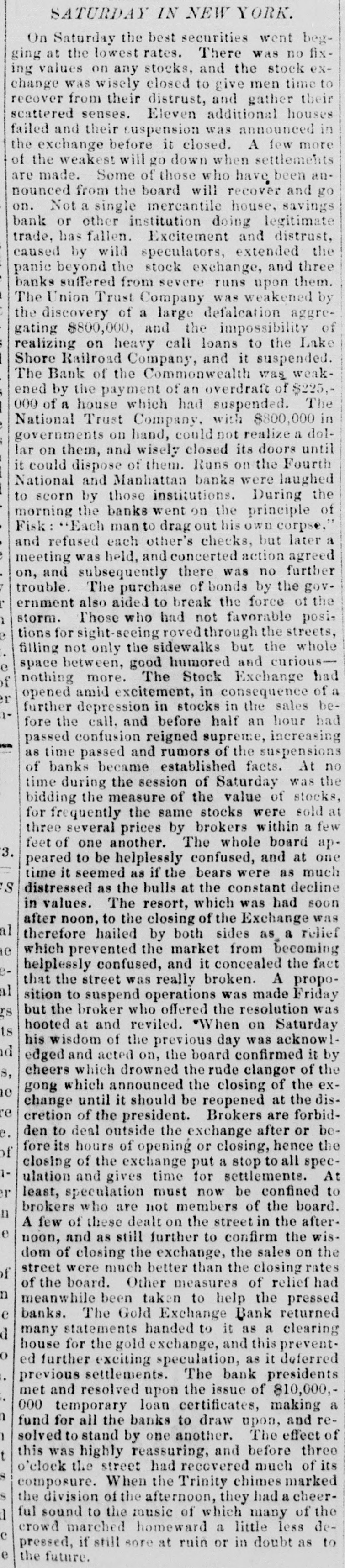

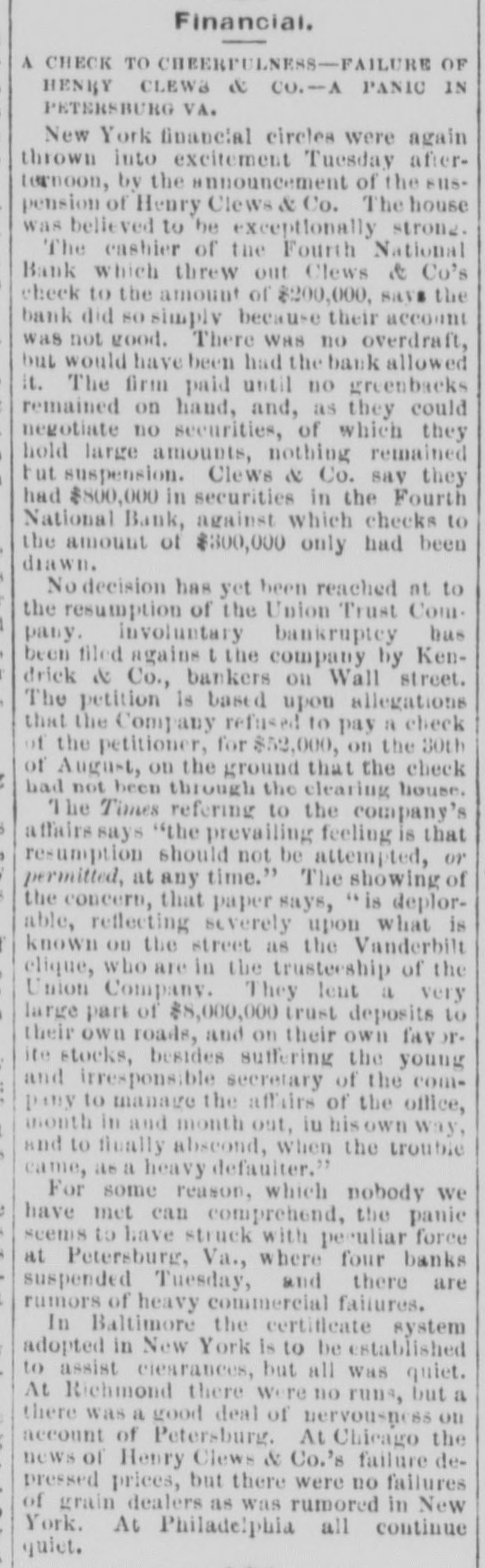

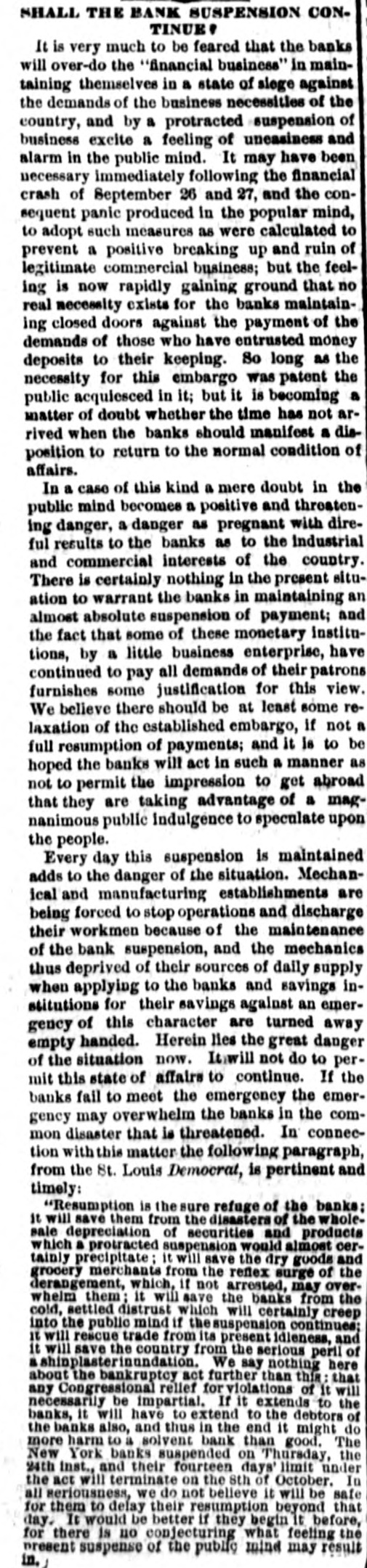

Article Text

coincidence that the gold corner of September, 1869, when so many persons were ruined, and the culmination of the panic of 1873, when the finances of the entire country have been placed in the most dangerous condition, happened upon the same day of the week and in the same month. Many men who appeared prominently in the first of these disturbances have also figured extensively in the last. Houses identified with the interests of the Government have been forced to succumb to the tremendous pressure brought to bear from damaging rumors and an unparalleled tightness of money. Jay Gould, too, who bulled gold in 1869 until it touched 162, is engaged in the present trouble. There have been two Black Fridays in the history of the country, and the sixth day of the week will hereafter be looked upon with suspicion in Wall street.

Commercial men, bankers, brokers, and the financial public generally, gathered in Wall street long before 10 o'clock yesterday morning. There was reason for it too. The rumors which had gained currency were not at all reassuring to people who had money to invest, or who wished to borrow it. Many persons had long lines of stocks which they were carrying; a panic would swallow up their margins, and leave them—wealthy the day before—in a state of penury. Some had money deposited in banks; a panic might force these institutions to suspend. Others were in a state of indecision, and did not know what to do.

The consequence was that thousands of people who are seldom seen down-town thought it worth their while to arrive on the scene of action early in the morning, so as to be on hand for anything which might turn up. It was a universal case of looking out for "number one," and so everybody who had anything to lose, or aught to gain, was on hand.

When the hour of 10 arrived, the time for the opening of the Stock Exchange, one of the most turbulent crowds of humanity ever seen in Wall street surged about the doors eager to obtain entrance. As soon as admittance was accorded there was a general rush to reach the floor of the Long Room, and in a moment afterward quotations for stocks were in order. No one knew what to offer, and everybody was undecided as to selling prices. It was at least a minute before quotations could be made, owing to the general uncertainty regarding the situation. The adherents of the bear clique thought that Western Union ought to sell at 70, and graded their bids accordingly. The few believers in a bull movement thought it was cheap at 80, and accordingly stood at that figure. When an average was reached, it appeared that the bears were the strongest, and so prices began to decline. Western Union, as on the day before, was the bone of contention, and the bears subjected it to their fiercest attacks.

The failure of Jay Cooke & Co. on the previous day had inspired such a distrust in wealthy banking-firms and in financial institutions of every class, that it soon became evident that the street was completely demoralized, and that there was not the slightest chance for the bulls to resist the onset. The Vanderbilt stocks, which are held at high prices, and which in ordinary times are regarded as among the safest of all investments, gave way shortly, and a tumble of a remarkable nature ensued.

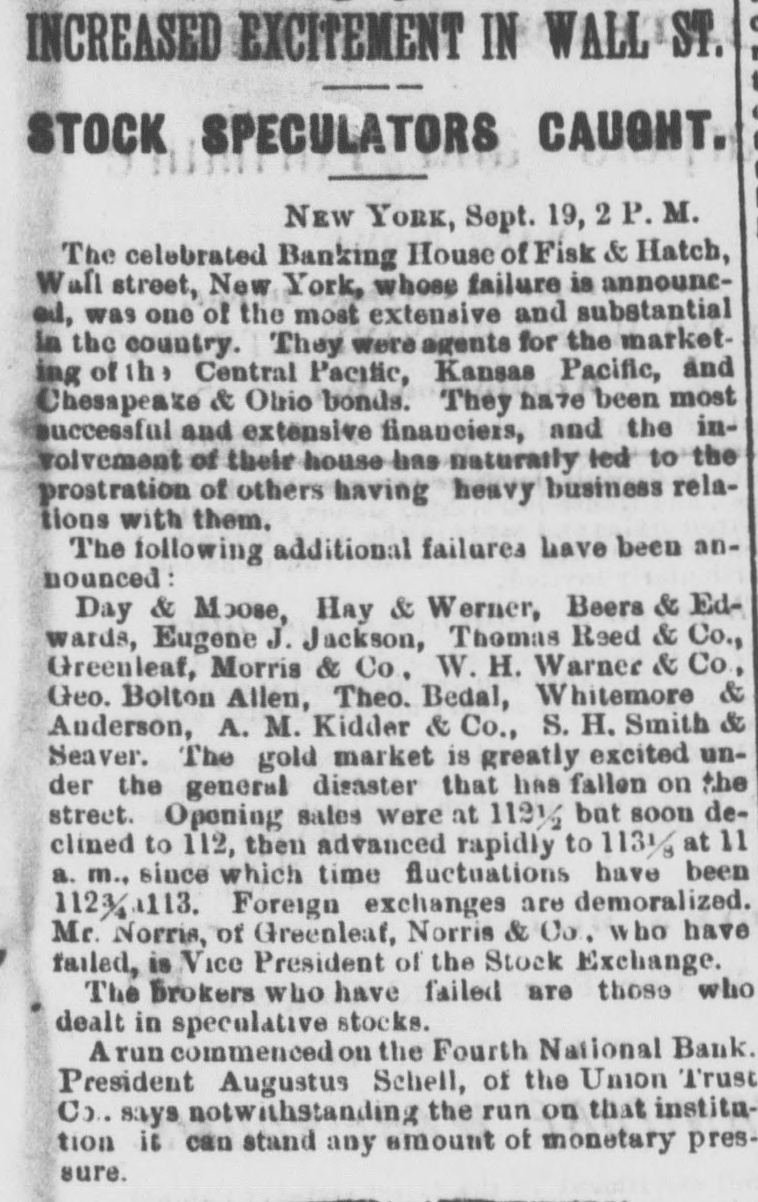

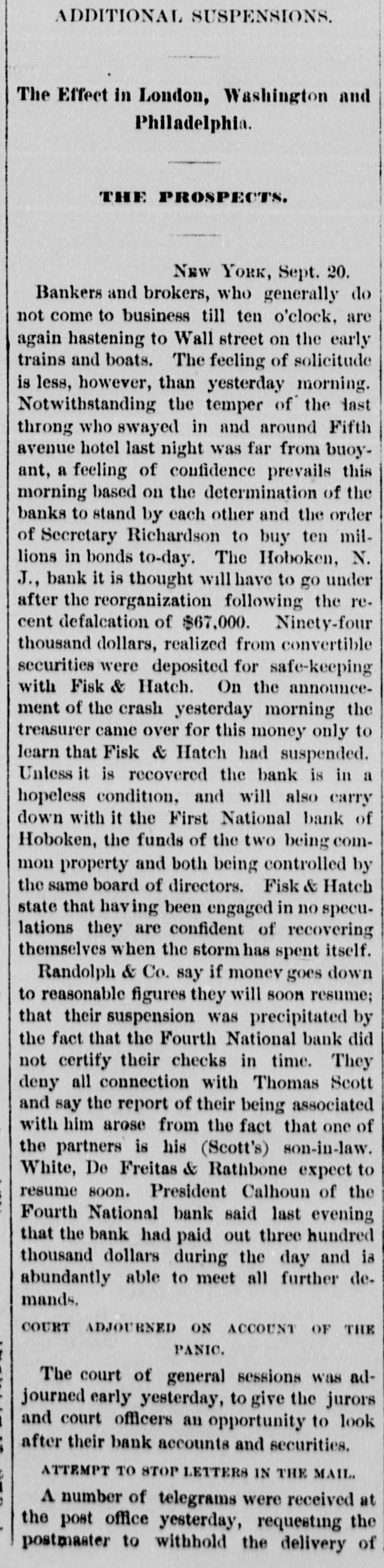

While prices were falling off rapidly, the news came of the suspension of Fisk & Hatch, supposed to be one of the strongest and most careful banking-houses in Wall street.

Up to this time, everything had been going in favor of the bears. As soon as the failure was announced on the Exchange, a tremendous panic ensued, and what appeared to be a sort of retreat on the part of the bulls and holders of stocks was turned into a frightful rout. There were no quotable prices for stocks for several minutes. Then a kind of "bottom" was found, when Western Union, New-York Central, Lake Shore, Harlem, and Rock Island, sold from five to twenty-five per cent. below the quotations of Thursday. Money, too, grew stringent, every one being afraid to loan upon any kind of stocks.

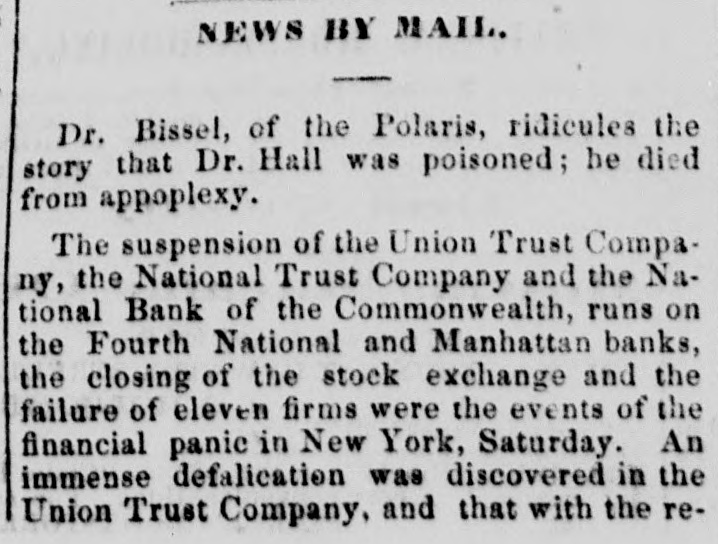

In addition to the failure of Fisk & Hatch, it was learned that the Fourth National Bank and the Union Trust Company were besieged by depositors, who were anxious to get their money. This was supplemented by a report that the Manhattan Company had refused to certify the checks of the Union Trust Company, in consequence of a dearth in deposits. This rumor proved to be correct, and had anything but a cheering influence upon the stock market and the rates for money.

Then the failures of different banking and brokerage houses were announced on the Exchange and news of these came so rapidly that each dealer was afraid to trust his neighbor, and so there was a difference in the cash and regular quotations of stocks of from one to five per cent. As fast as the failures were announced the news was carried out into the street by brokers, and in spite of a cold, drenching rain, hundreds of people gathered about the offices of fallen reputation and gazed curiously through the windows, trying to form some conception of the way in which the broken brokers were behaving.

Merchants up-town took a trip to Wall street and swelled the crowds who stood about inspired by their aimless curiosity to gaze upon the distress of neighbors, and nearly every house of deposit in the street was thronged by nervous customers who didn't care to draw out their money if they could have it, but who were terribly anxious to grasp the greenbacks if there were no funds on hand.

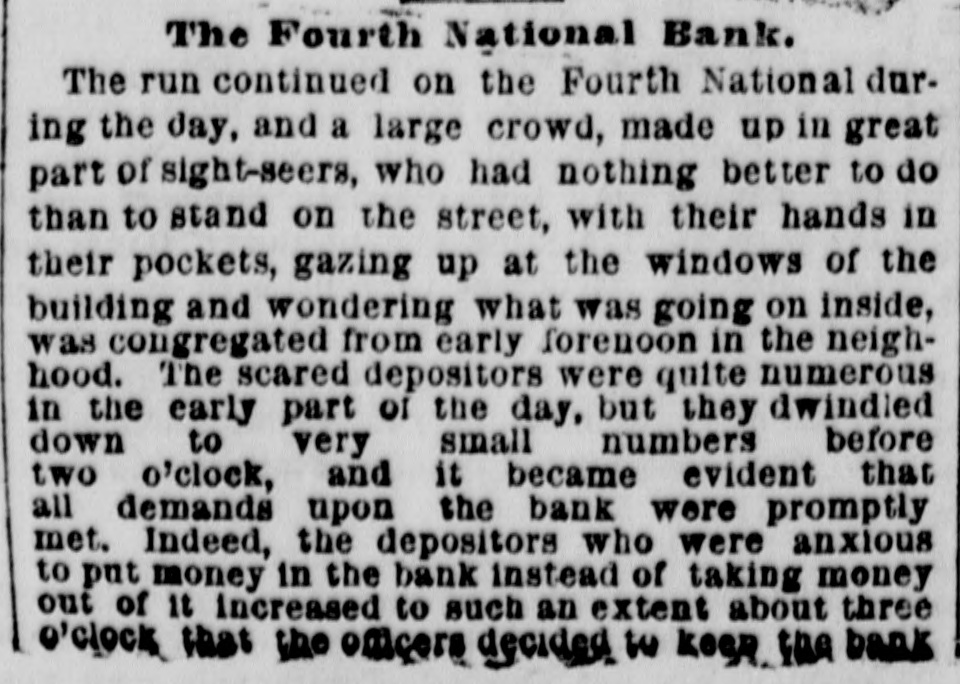

A long line of depositors extended outside of the Union Trust Company's building far into the street, waiting for money which had been put in, but which might remain longer than had been calculated upon. At the Fourth National Bank there was a like scene. Umbrellas were called into requisition, and the financial arena of the country resembled a stony pavement covered with black mushrooms.

The peculiar position of the steps of the Sub-Treasury, which affords a commanding view of both Wall and Broad streets, caused them to be used for convenient points of observation, and they were thronged with people for the entire day. The rain seemed to have no effect whatever upon the crowds, which, financially interested, cared nothing whatever for bodily discomfort.

Some time in the afternoon a rumor was prevalent that Secretary Richardson would deposit $10,000,000 in the various banks as a means of relief from the pressing monetary stringency, and in a few minutes the stock market began to show signs of strength.