Click image to open full size in new tab

Article Text

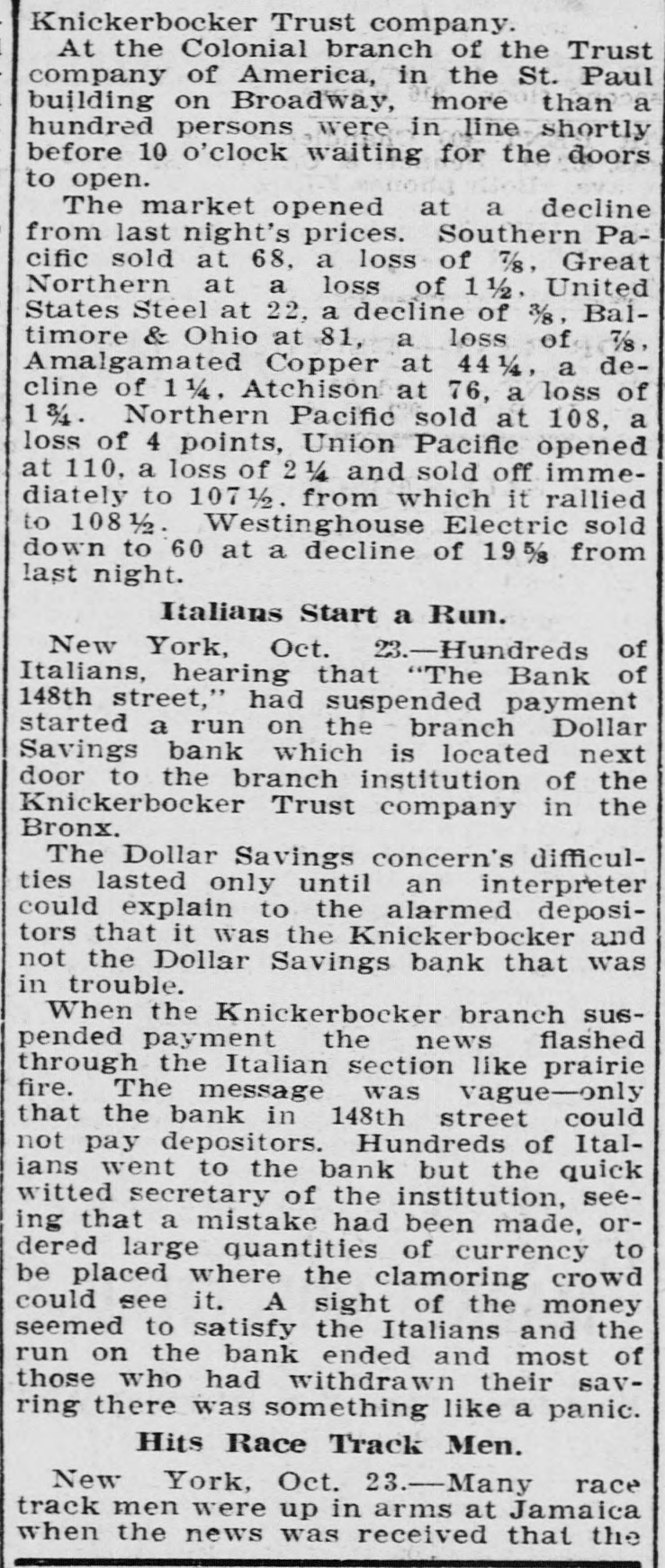

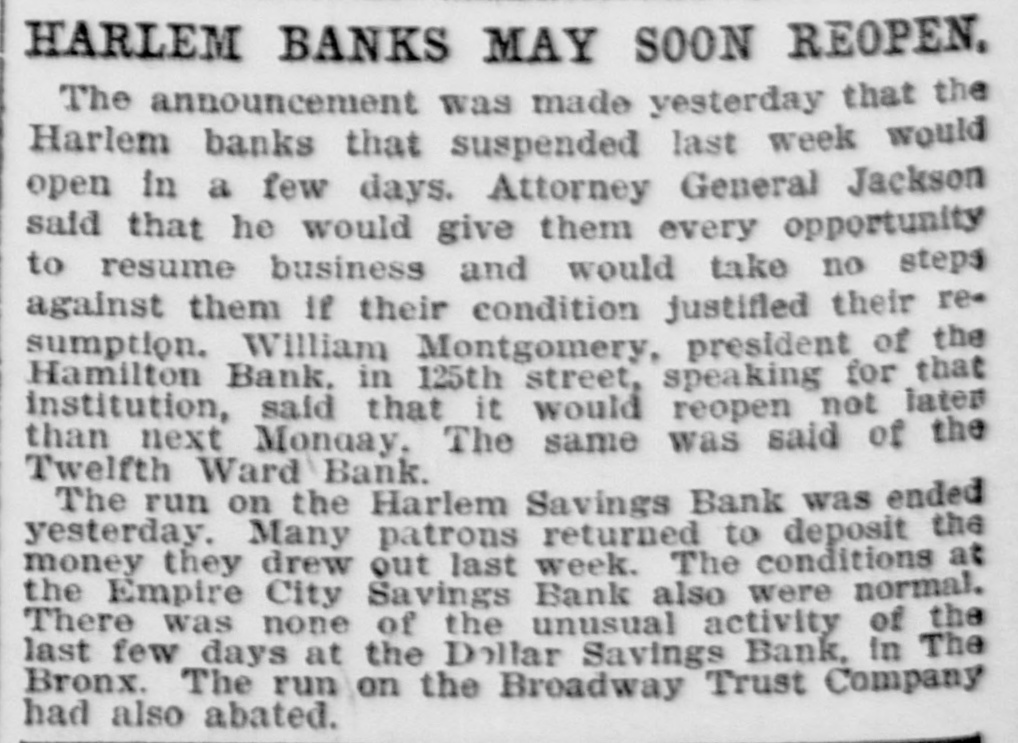

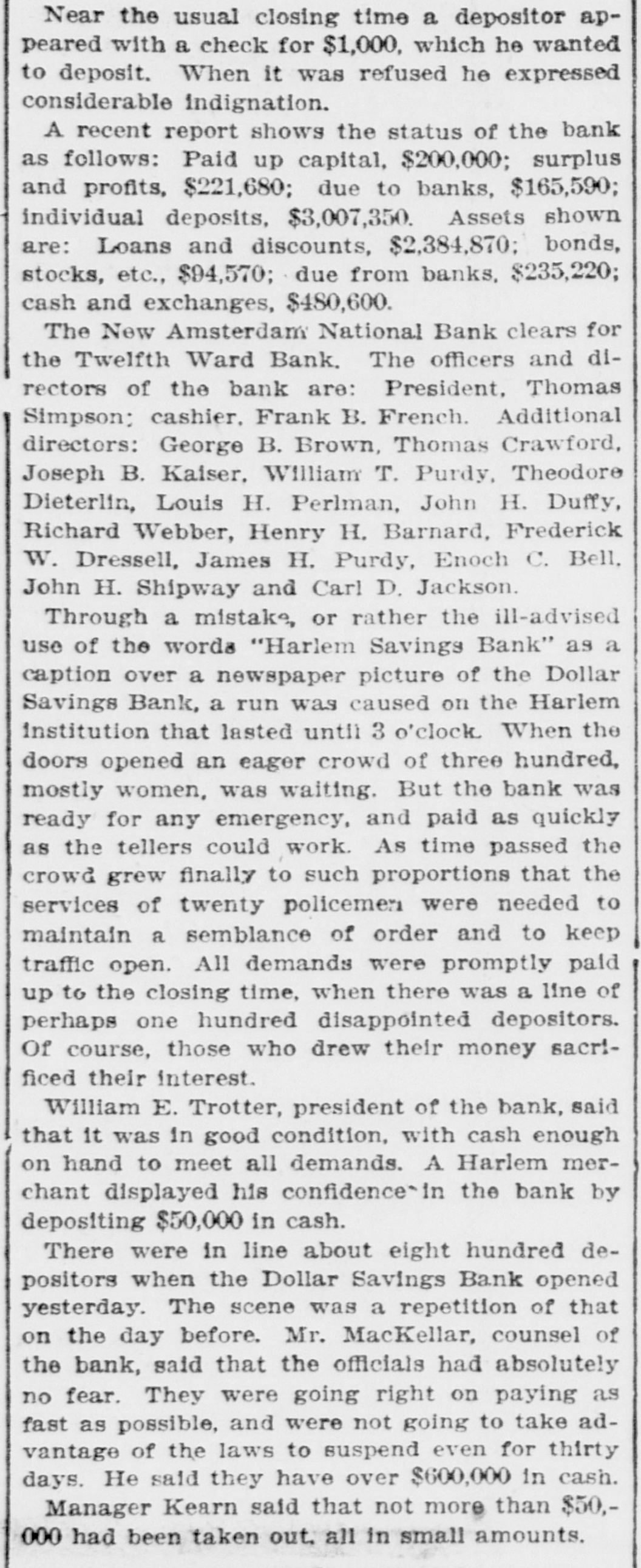

Near the usual closing time a depositor appeared with a check for $1,000, which he wanted to deposit. When it was refused he expressed considerable indignation. A recent report shows the status of the bank as follows: Paid up capital, $200,000; surplus and profits, $221,680; due to banks, $165,590; individual deposits, $3,007,350. Assets shown are: Loans and discounts, $2,384,870; bonds, stocks, etc., $94,570; due from banks, $235,220; cash and exchanges, $480,600. The New Amsterdam National Bank clears for the Twelfth Ward Bank, The officers and directors of the bank are: President, Thomas Simpson; cashier. Frank B. French. Additional directors: George B. Brown, Thomas Crawford, Joseph B. Kaiser, William T. Purdy, Theodore Dieterlin, Louis H. Perlman, John H. Duffy, Richard Webber, Henry H. Barnard, Frederick W. Dressell, James H. Purdy, Enoch C. Bell. John H. Shipway and Carl D. Jackson. Through a mistake, or rather the ill-advised use of the words "Harlem Savings Bank" as a caption over a newspaper picture of the Dollar Savings Bank, a run was caused on the Harlem institution that lasted until 3 o'clock When the doors opened an eager crowd of three hundred, mostly women, was waiting. But the bank was ready for any emergency, and paid as quickly as the tellers could work. As time passed the crowd grew finally to such proportions that the services of twenty policement were needed to maintain a semblance of order and to keep traffic open. All demands were promptly paid up to the closing time, when there was a line of perhaps one hundred disappointed depositors. Of course, those who drew their money sacrificed their interest. William E. Trotter, president of the bank, said that it was in good condition, with cash enough on hand to meet all demands. A Harlem merchant displayed his confidence in the bank by depositing $50,000 in cash. There were in line about eight hundred depositors when the Dollar Savings Bank opened yesterday. The scene was a repetition of that on the day before. Mr. MacKellar, counsel of the bank, said that the officials had absolutely no fear. They were going right on paying as fast as possible, and were not going to take advantage of the laws to suspend even for thirty days. He said they have over $600,000 in cash. Manager Kearn said that not more than $50,000 had been taken out. all in small amounts.