Click image to open full size in new tab

Article Text

First National Bank, Apparently Insolvent, Kept Open for Business by Sheldon Brothers While They Get Under Cover

Indicate That Splitup Made Several Reports a Years Ago Gave Sheldon the Money, Gave A. M. Sheldon the Debts, and Left the Depositors to Hold the Bag

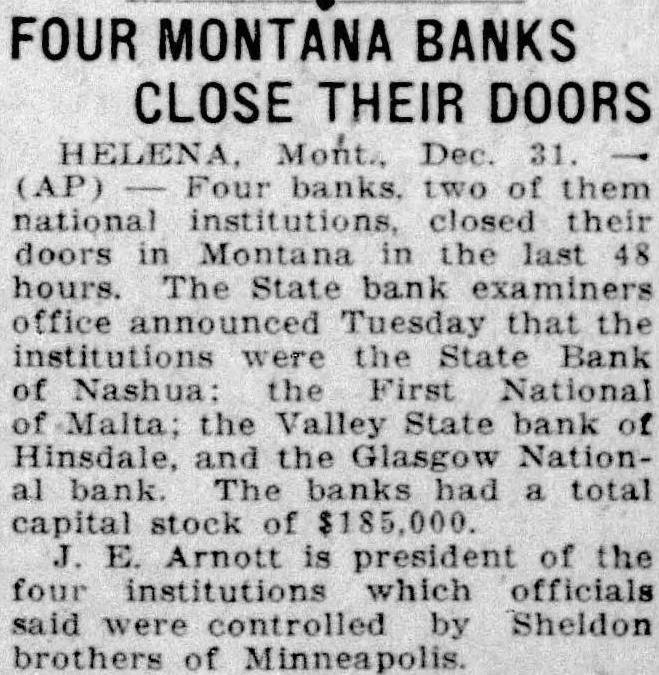

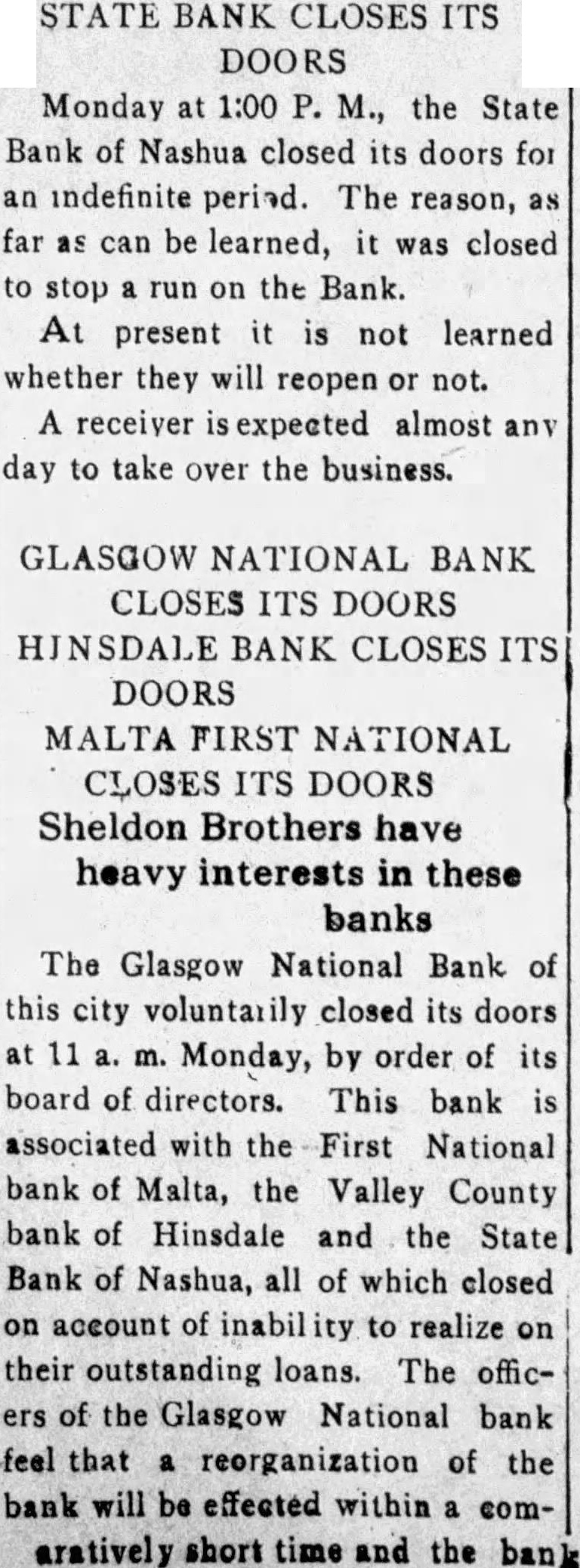

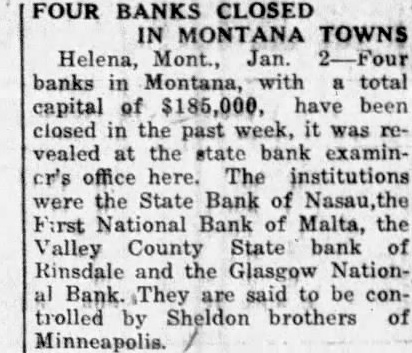

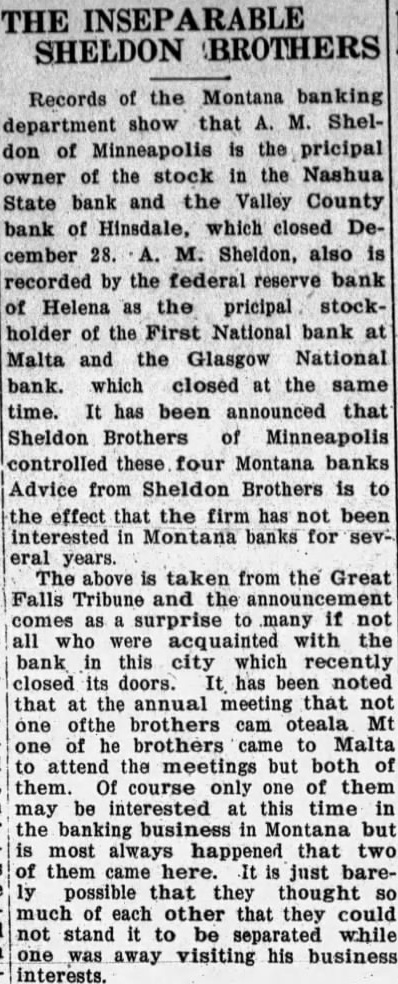

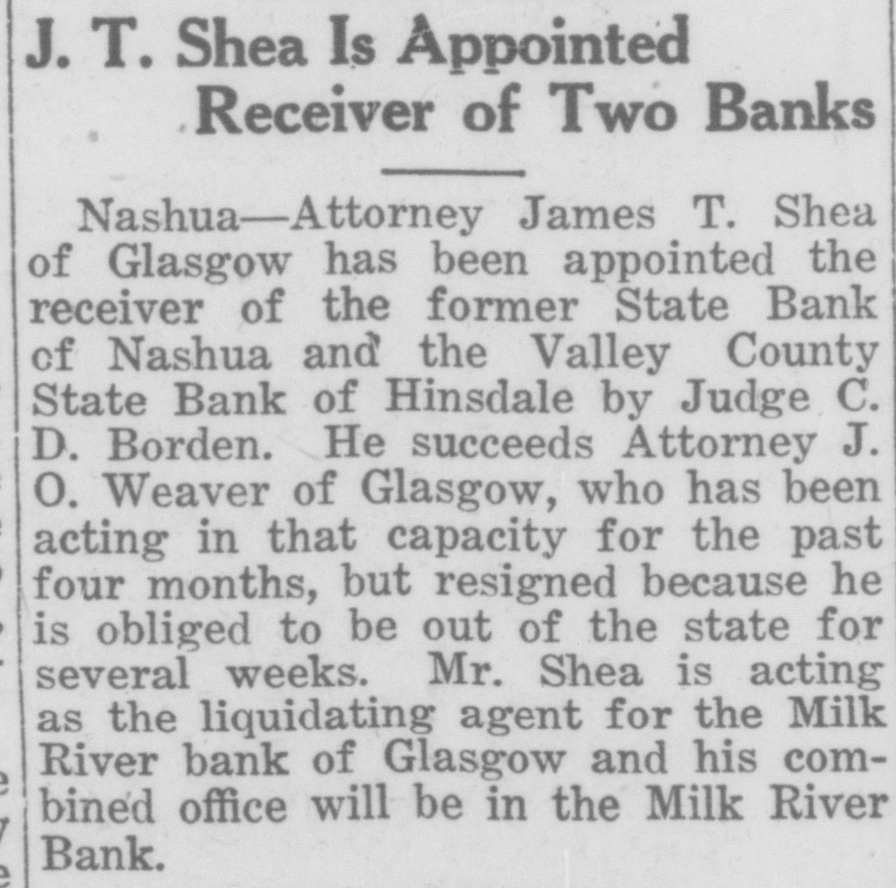

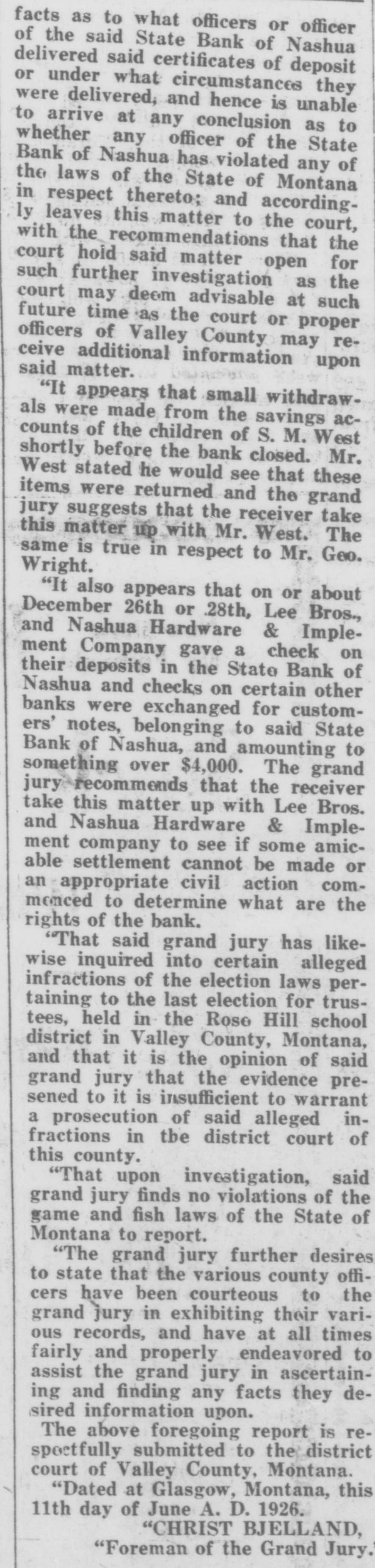

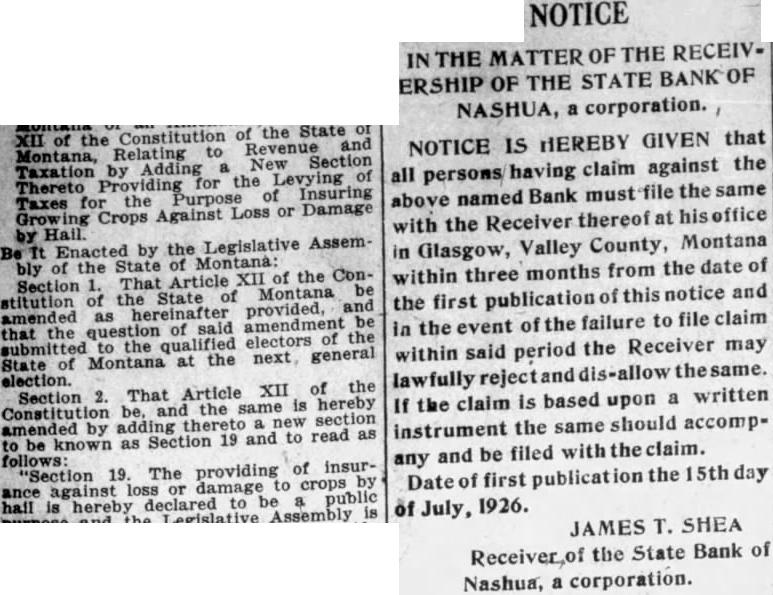

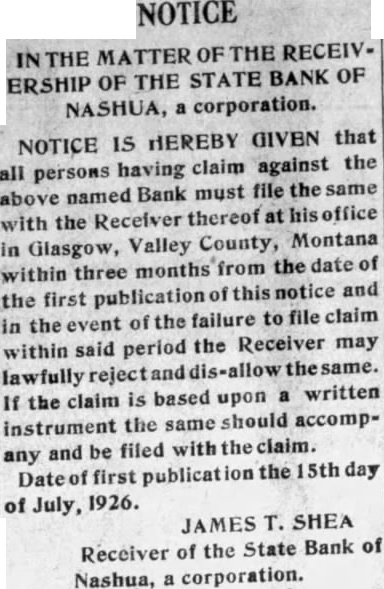

According to the records of the Montana A. M. Sheldon of Sheldon brothers, Minneapolis, is the principal owner of stock in the four banks of the Sheldon-Arnot combination in the Milk river valley that collapsed Monday, December 30th. Advice from Sheldon brothers conveys the information that the firm has not been Montana for several interested years. Reports from Minneapolis, traceable directly to A. M Sheldon, are to the effect that A. M Sheldon is unable to meet his obligations in the closed Montana banks. and that F. P. Sheldon is not responsible for those obligations because several years ago, he had sold out his Montana interests to A. M. Sheldon. The logical inference of all this is that "several years ago" A. M. Sheldon and F. P. Sheldon devised a split, and that F. P. Sheldon took the assets and A. M. Sheldon took the liabilities. Presumably, and to all legal intents and purposes, A. M. Sheldon, who owns the stock in the collapsed banks and whose name is attached to the bonds securing deposits in the banks, is broke, and F. P. Sheldon, who owns nothing in Montana and is liable for nothing in the collapsed banks has the money. This is the framework of the story that is now afloat for the consolation of the people who lost their money in the First National bank of Malta, the Valley County State bank of Hinsdale, the Nashua State bank and the Glasgow National bank. It now looks very much as if the two Sheldons, F. P. Sheldon A. M. Sheldon, "several years ago," deliberately set out to finish the First National bank of Malta, and it is the settled conviction of many people that that is exactly what they did do. For several years they seem to have run the Malta bank on bluff. It is said there never was a time during that two years that they could meet the demand deposits of the bank, and there was never an effort on the part of large depositor to get his money that the whining bluff was not set up that if the money was demanded the bank would have to close. In that time the county treasurer, the city officials and the depositors of the bank were patient and easy with the bank in the hope that it might eventually get in better condition. And everybody, depositors and the local officials of the bank alike, depended upon the supposed integrity of A. M. Sheldon and P.'Sheldon to use the time and opportunity to strengthen the bank's tottering foundation. It now seems A. M. Sheldon and P. Sheldon used that patience and that confidence to get under cover and to leave the depositors and stockholders of the bank high and dry. "Several years ago" F. P. Sheldon was the largest stockholder and the big bug in the Montana banks, and A. M. Sheldon had his chief interests the Imperial Elevator company. So far as the people who did business with them or their banks are concerned. however, they were considered ns equally responsible. It now develops that in that ominous "several years ago" M. Sheldon sold out his Imperial Elevator company holdings and bought from F. P. Sheldon his Montana banking liabilities for which he gave F. P. Sheldon his note! The so-called Sheldon banks continued to de business with the people none the wiser, and the credit and standing of the Montana banks was based on the financial standing of P. Sheldon as much ns on that of M. Sheldon. In that significant "several years ago" the two Sheldons formed n corporation known as The Sheldon Brothers company. and that company became and still is the harbor of safety for the personal responsibility of this foxy pair. The blunt facts of the situation seem to be that the First National bank of Malta has been insolvent "for several since the Sheldon brothers quit doing business firm tana The broad Inference forced the people by the actions of and F. Sheldon is that they knew that sooner or the bank would collapse, and the general conclusion that they were careful only to see that it. did not collapse around their own smooth heads. In view of all the stories that are told by some of the depositors of the bank about their efforts to get their money out of the bank, from a study of the published statements of the bank's condition, and from a general survey of business and banking conditions in northeastern Montana, there never were but two hopes of the First National bank continuing in business: One was that the land values on which they had most of their loans would enhance and a ready market be created for them SO they might become readily negotiable. A. M. Sheldon and F. P. Sheldon were too shrewd business men and too not to know that this was a forlorn hope. The other, and that was the delusion the depositors in the bank were brought under, was that Sheldon brothers would stand back of the bank, even in its extremity, and that proved to be only a broken stick were leaning on.

In other words, it seems that if the First National bank had closed "several years ago," when it probably should have closed, F. P. Sheldon would have had to bear some of the burden of its losses, but in that several years, while the bank's condition was not improving, A. M. and F. P. Sheldon devised the nice little scheme by which M. Sheldon went legally broke, Sheldon kept the money in the family, and the innocent people who had their money tied up in the bank were left holding the bag. Up the First National bank did business in Malta, there was just one excuse for its remaining open, and that was that J. E. Arnot of Glasgow and A. M. Sheldon and F. P. Sheldon of Minneapolis would come to its rescue. A marvel to many business men and bankers is how the First National bank of Malta has gotten by the bank examiner for these past two years. The most plausible excuse is that the banking department labored under the same deception as the depositors and believed that Sheldon brothers would straighten out the bank's tangled affairs.

It is apparent that the bank had no realizable assets that were not pledged. During the last few days of the bank's existence one depositor got $500.00 in currency out of the bank and he was told that the bank had just $88.00 left in the till with which to do business. Apparently the bank had nowhere to look for cash in any sum except to the Sheldons and Arnot. To keep any bank open and accept deposits under such weakened condition could be excused only by a perfect confidence that the Integrity of the men at its head could be depended upon to furnish the money to hold it together. The stories that are told about the county treasurer starting a run on the bank seem to be pure unadulaterated poppycock. The county had $50,000.00 on deposit in the bank. It was subject to check. It was larger sum than was carried in efther of the other two Malta banks. The county treasurer was under the necessity of cutting the deposit down to equalize It with the other banks. Checks were written by the treasurer in the regular course of business, and when the first one cleared the bank the treasurer was informed that the bank could not stand it. The action did not in any wise affect the condition of the bank, It was only the occasion of proving that the bank was absolutely unable to meet, its demands. The very argument offered by the bank that it was not notified by the county treasurer that the county would begin checking against its deposits in plain confession that the bank had no money and no reserve to amount to anything. because the county's account was checking one and was supposed to be used. Neither of the other Malta banks required notice. and on the 18th day of December treasurer wrote checks totaling on one of the other Malta without notice, and the bank no grievance. There was no run on the bank. There have been run on It. The first two or three depositors to have at the bank run would appeared

Here Is the Fast Malta High Basketball Quinteț Which Gave the "Terrible Swedes" Battle Royal Tuesday a

In one of the fastest high school games ever seen on the local floor, the Malta team went down to defeat before the Harlem aggregation Tuesday night by a score of 18 to 30. Even though defented, the Multa boys played one of the best games of their career, time after time bringing the large erowd to their feet with their splendid floor work. The Malta team had the ball in their possession about sixty per cent of the time and took fully twice as many chances at the basket as the Harlem players. By the law of averages the game should have gone to Malta. Shooting is perhaps the main weakness of Malta. Their team work is fully as good as Harlem and their taking the ball through five man defense is perhaps better than that of any team in this section of the state. Time after time the Malta boys broke through the defense of their opponents only to miss comparatively easy shot at the basket. The game started with rush and the Harlem players made two baskets in quick succession. The Malta team then did some fine basket shooting and made ten points without allowing Harlem to score any more that quarter. Harlem was a little more accurate in shooting in the second quarter and the half ended with the score 16 to 12 in their favor. In the second half Malta made six points while Harlem made fourteen.

The players for Malta were: Johnson, center; Edwards, forward; Costello, forward: Koon, guard and Watson, guard. In the beginning of the second quarter Verzatt went in at forward. Costello was sent to guard and Watson taken out. Watson is developing into one of the star guards of this section of the state but because of inexperience was held as substitute the last three quarters. He a heavy, powerful guard and will be a hard man to keep off of the team as regular. As whole, the Malta team is very fast and as soon as they develop their shooting, will give a good account of themselves against any high school team of the state.