Public signal of financial health, Capital injected, Full suspension, Books examined

Other: Depositors were asked to grant extensions on their deposits (depositor extensions) and officers/stockholders collected cash (~$400,000) to enable resumption; stock capitalization reduction/reorganization was planned.

Description

Depositors' heavy withdrawals amid the 1893 financial stringency forced a temporary suspension on Aug 4–5, 1893. Examiners/receiver (D. W. Lawler) were appointed; the bank was reorganized and reopened Oct 30–31, 1893. Cause is systemic loss of confidence (national financial stringency) rather than a discrete misinformation incident.

Events (6)

1.May 9, 1883Chartered

Source

historical_nic

2.August 4, 1893Run

Cause

Macro News

Cause Details

Prolonged drain of deposits amid the national financial stringency and loss of confidence; steady withdrawals since January left the bank unable to convert assets quickly enough to meet demands.

Measures

Appointed Dan W. Lawler as special bank examiner to take charge temporarily; solicit extensions from depositors and realize upon assets; cooperation with Comptroller for resumption.

Newspaper Excerpt

Owing to the continual withdrawal of deposits the bank has been compelled to suspend.

Source

newspapers

3.August 4, 1893Suspension

Cause

Macro News

Cause Details

Temporary suspension declared because continual withdrawals during the broader financial stringency made it impossible to meet demands despite ample assets; needed time to realize securities.

Newspaper Excerpt

The National German-American bank not open for business tomorrow morning...the prolonged drain upon the assets...has forced the step upon the officers and directors.

Source

newspapers

4.August 5, 1893Receivership

Newspaper Excerpt

Daniel W. Lawler has been appointed receiver / Daniel W. Lawler has been appointed to assume charge of the affairs of the bank.

Source

newspapers

5.October 30, 1893Reopening

Newspaper Excerpt

It has been decided to reopen the National German-American bank of St. Paul on Oct. 30. / The reorganized National German-American Bank...reopened yesterday.

Source

newspapers

6.November 27, 1912Voluntary Liquidation

Source

historical_nic

Newspaper Articles (21)

1.August 4, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

FUNDS TIED UP. AL GERMAN-AMERICAN BANK NOT TO OPEN TODAY. EPOSITORS TO BEE FULLY PAID Which Led to the Suspension-Official Statement of the Oficers-Over $4,000,000 Bills Receivable to $2,400,000 De-. posits-Early Payment of Di> idends to Depositors Expected. meeting of the directors of the NaGerman-American bank was at 3:30 yesterday afternoon, and it after 6 p. m. when it was adUpon its conclusion the folstatement was given to the pubThe National German-American bank not open for business tomorrow morning. The prolonged drain the assets, which has been steady unceasing for many months past, at of the year when our agricultand business community are awaitthe gathering of the crops, and ineasing just when the financial skies apparently brightening.ha forced step upon the officers and directors. universal distrust which has perall parts of this country for the four months has been felt both and West. This bank has felt n drain by its depositors, and has been withdrawn $1,562,since January, while it has impossible to correspondingly its loans at a period of the year every one in agricultural sections ours is so largely relying upon the taring harvest. The bank has susno serious losses of any nature. has ample assets to meet all its bilities, but when the temper of its positors is SO unreasonable and unreiting, no other course but temporary spension was possible." The above brief official statement tells story of the first serious reverse has come to St. Paul during this paralleled financial stringency. accordance with the usual custom banking business. a large amount of of the customers of the bank had rediscounted in the East, and a nsiderable sum was rapidly maturing. had up to date been promptly paid due, but as the financial strinprevented the bank's cusfrom meeting their paper, by renewal, and as this same ingency caused the Eastern correondents to decline renewais and inon payment. it was impossible, in face of the continued withdrawal of posits, to do otherwise than temposuspend. It was not because of proper management, or losses or invency, but simply the sheer impossiof being able to realize upon aswith sufficient rapidity to meet the mands for cash, and the only way to the crisis was to temporarily stop siness. A Call on President Lockey. GLOBE representative called upon esident Joseph Lockey at his Summit residence last evening. Mr. said there was little to add to official statement given above. You can, however, say," he added, the depositors will be paid every in full. We have over four milldollars in bills receivable to twentyhundred thousand dollars in deand it is only a question of the required to realize upon our assets enable us to pay depositors the entire

2.August 5, 1893The Roanoke TimesRoanoke, VA

Click image to open full size in new tab

Article Text

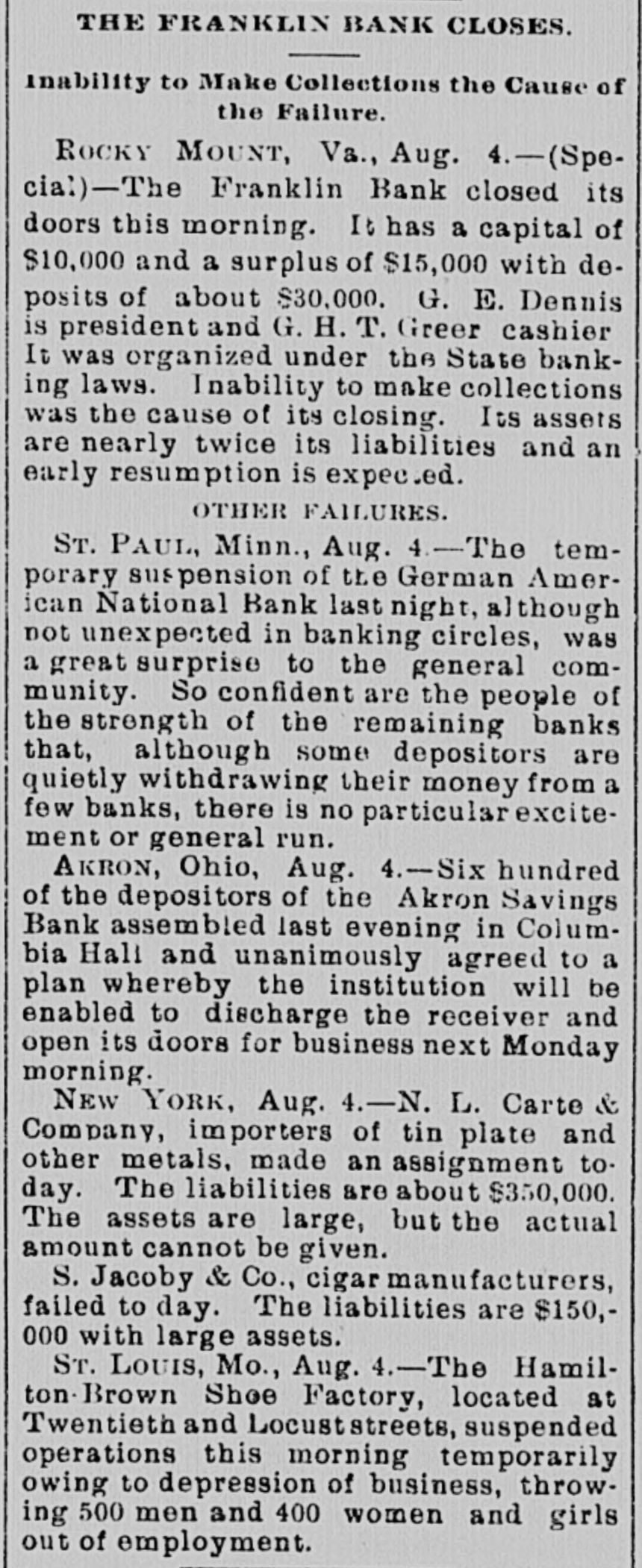

THE FRANKLIN BANK CLOSES. inability to Make Collections the Cause of the Failure. ROCKY MOUNT, Va., Aug. 4.-(Special)-The Franklin Bank closed its doors this morning. It has a capital of $10,000 and a surplus of $15,000 with deposits of about $30,000. G. E. Dennis is president and G. H. T. Greer cashier It was organized under the State banking laws. Inability to make collections was the cause of its closing. Its assets are nearly twice its liabilities and an early resumption is expected. OTHER FAILURES. ST. PAUL, Minn., Aug. 4.-The temporary suspension of the German American National Bank last night, although not unexpected in banking circles, was a great surprise to the general community. So confident are the people of the strength of the remaining banks that, although some depositors are quietly withdrawing their money from a few banks, there is no particular excitement or general run. AKRON, Ohio, Aug. 4.-Six hundred of the depositors of the Akron Savings Bank assembled last evening in Columbia Hall and unanimously agreed to a plan whereby the institution will be enabled to discharge the receiver and open its doors for business next Monday morning. NEW YORK, Aug. 4.-N. L. Carte & Company, importers of tin plate and other metals, made an assignment today. The liabilities are about $350,000. The assets are large, but the actual amount cannot be given. S. Jacoby & Co., cigar manufacturers, failed to day. The liabilities are $150,000 with large assets. ST. LOUIS, Mo., Aug. 4.-The Hamilton- Brown Shoe Factory, located at Twentieth and Locuststreets, suspended operations this morning temporarily owing to depression of business, throwing 500 men and 400 women and girls out of employment.

3.August 5, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

AFTER THE STORM. National German - American May Speedily Resume. PLANS SUGGESTED TO THAT END Lawler in Charge Until Examiner Thorne Arrives. BUSINESS CIRCLES TRANQUIL. Ringing Utterances From Archbishop Ireland, JAMES J. HILL AND OTHERS. The present indications are decidedly favorable to some plan being evolved for the reorganization and speedy resumption of business by the National German-American bank. So tar as paying the depositors in full is concerned, the bank is overwhelmingly solvent, the assets. including stockholders' liabilities, aggregating at least three dollars for every one on deposit, and the universal sentiment is that such a instution great should be saved to the city, state and the Northwest. It has long been realized, by the parties that the interested, capitalization but was so large as to be unwieldy; on R reduced capitalization, say of $1,000,000 or $1,200,000, it would not be a difficult matter to make arrangemente for speedy resumption. All that is needed is a little time to realize upon assets, and this the suspension secures. It is a heroic and not pleasant remedy, it is true, but far better than to allow the institution to go out of existence. As the bills receivable exceed the deposits by over sixteen hundred thousand dollars, the impairment of the capital is not likely to be severe; and if the capitalization should be reduced, the stock would undoubtedly stand in the market at least at 150, and perhaps higher. The stock is largely held by wealthy people, a good deal of it by Eastern financial institutions, who would undoubtedly prefer a reduced capitalization to liquidation. The co-operation of the depositors in such a scheme is also suggested, and to a very considerable extent this could undoubtedly be secured. It seems reasonably probable that Gustav Willius, the former president, will he selected by Comptroller Eckels AS the receiver. No better man couldbe round to handle its affairs. His familiarity with the business of the bank and its customers, having been one of its leading officers from its inception until within the past two years, with together his experience in his the banking business, would make selection inspire confidence at once in the plan for speedy resumption. Comptroller Eckels, in selecting Mr. Lawler as bank examiner to tempora rily take charge of the bank, instructed him to aid the officers in every way in any plans for resumption, as he regards the bank as perfectly solvent, and only compelled to suspend by the abnormal financial stringency. With the co-operation of the comptroller, the stockholders, the depositors and the general business public, it is not too much to expect the speedy reopening of the doors of the National German-American, with its position in the financial world really improved by the temporary halt in its active business while the work of realization on the undoubted assets is taking place.

4.August 5, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

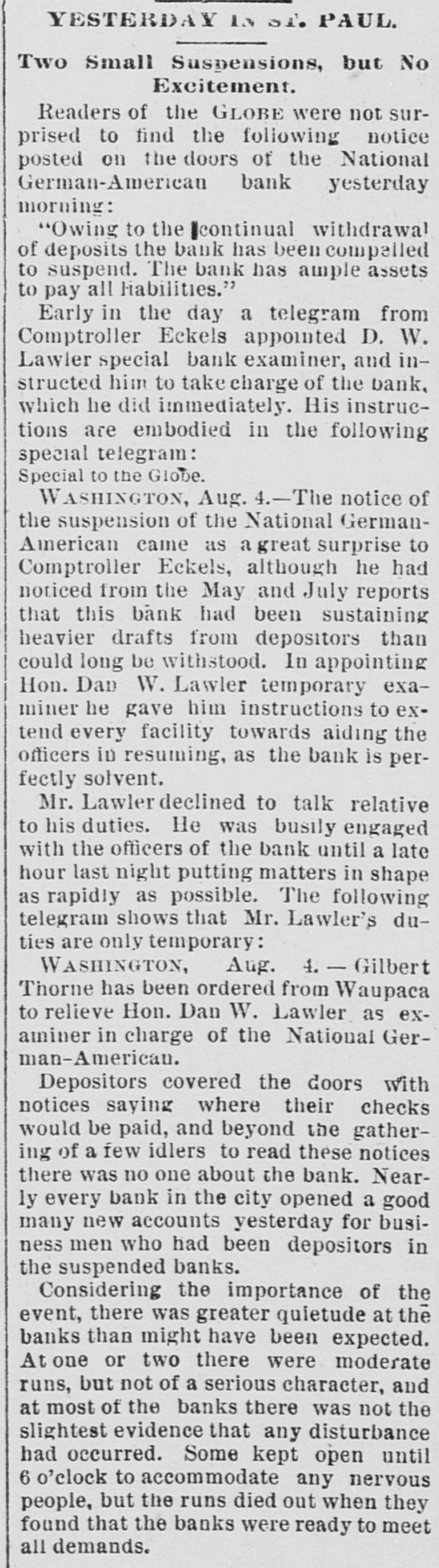

YESTERDAY PAUL. Two Small Suspensions, but No Excitement. Readers of the GLOBE were not surprised to find the following notice posted on the doors of the National German-American bank yesterday morning: "Owing to the continual withdrawal of deposits the bank has been compelled to suspend. The bank has ample assets to pay all liabilities." Early in the day a telegram from Comptroller Eckels appointed D. W. Lawler special bank examiner, and instructed him to take charge of the bank, which he did immediately. His instructions are embodied in the following special telegram: Special to the Globe. WASHINGTON, Aug. 4. - The notice of the suspension of the National GermanAmerican came as a great surprise to Comptroller Eckels, although he had noticed from the May and July reports that this bank had been sustaining heavier drafts from depositors than could long be withstood. In appointing Hon. Dan W. Lawler temporary examiner he gave him instructions to extend every facility towards aiding the officers in resuming, as the bank is perfectly solvent. Mr. Lawler declined to talk relative to his duties. He was busily engaged with the officers of the bank until a late hour last night putting matters in shape as rapidly as possible. The following telegram shows that Mr. Lawler's duties are only temporary: WASHINGTON, Aug. 4. - Gilbert Thorne has been ordered from Waupaca to relieve Hon. Dan W. Lawler as examiner in charge of the National German-American. Depositors covered the doors with notices saying where their checks would be paid, and beyond the gathering of a few idlers to read these notices there was no one about the bank. Nearly every bank in the city opened a good many new accounts yesterday for business men who had been depositors in the suspended banks. Considering the importance of the event, there was greater quietude at the banks than might have been expected. At one or two there were moderate runs, but not of a serious character, and at most of the banks there was not the slightest evidence that any disturbance had occurred. Some kept open until 6 o'clock to accommodate any nervous people. but the runs died out when they found that the banks were ready to meet all demands.

5.August 5, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

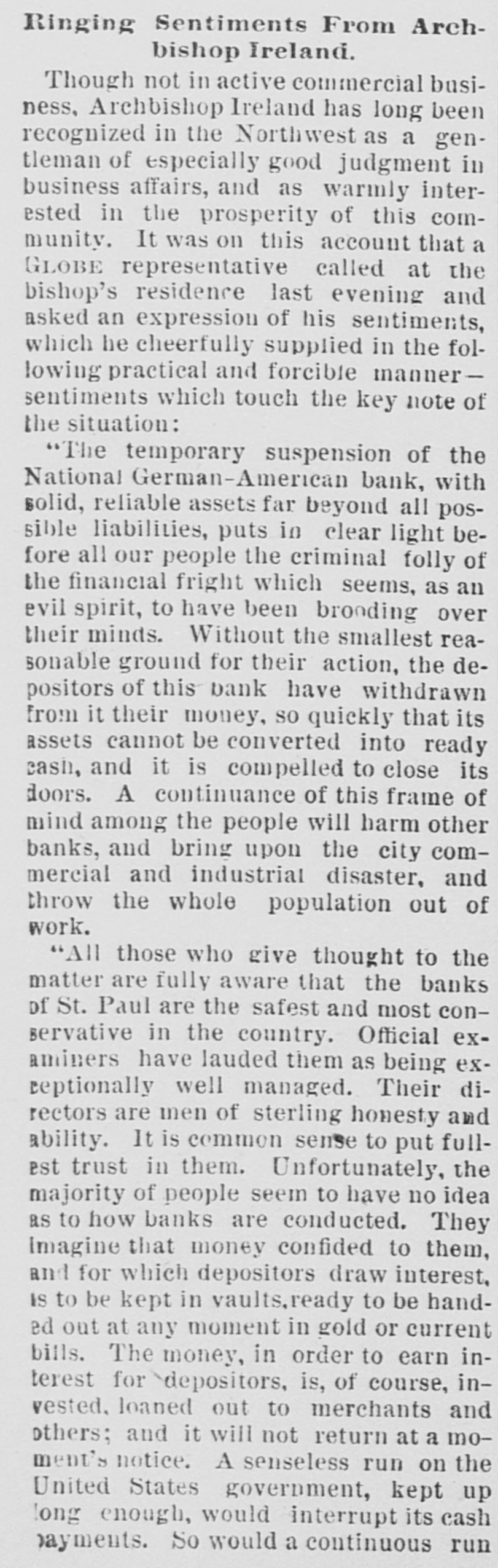

Ringing Sentiments From Archbishop Ireland. Though not in active commercial business, Archbishop Ireland has long been recognized in the Northwest as a gentleman of especially good judgment in business affairs, and as warmly interested in the prosperity of this community. It was on this account that a GLOBE representative called at the bishop's residence last evening and asked an expression of his sentiments, which he cheerfully supplied in the following practical and forcible mannersentiments which touch the key note of the situation: "The temporary suspension of the National German-American bank, with solid, reliable assets far beyond all possible liabilities, puts in clear light before all our people the criminal folly of the financial fright which seems, as an evil spirit, to have been brooding over their minds. Without the smallest reasonable ground for their action, the depositors of this bank have withdrawn from it their money, SO quickly that its assets cannot be converted into ready cash, and it is compelled to close its doors. A continuance of this frame of mind among the people will harm other banks, and bring upon the city commercial and industrial disaster, and throw the whole population out of work. "All those who give thought to the matter are fully aware that the banks of St. Paul are the safest and most conservative in the country. Official examiners have lauded them as being exreptionally well managed. Their directors are men of sterling honesty and ability. It is common sense to put fullest trust in them. Unfortunately, the majority of people seem to have no idea as to how banks are conducted. They Imagine that money confided to them, and for which depositors draw interest, is to be kept in vaults, ready to be handed out at any moment in gold or current bills. The money, in order to earn interest for depositors, is, of course, invested, loaned out to merchants and others; and it will not return at a moment's notice. A senseless run on the United States government, kept up long enough, would interrupt its cash payments. So would a continuous run

6.August 5, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

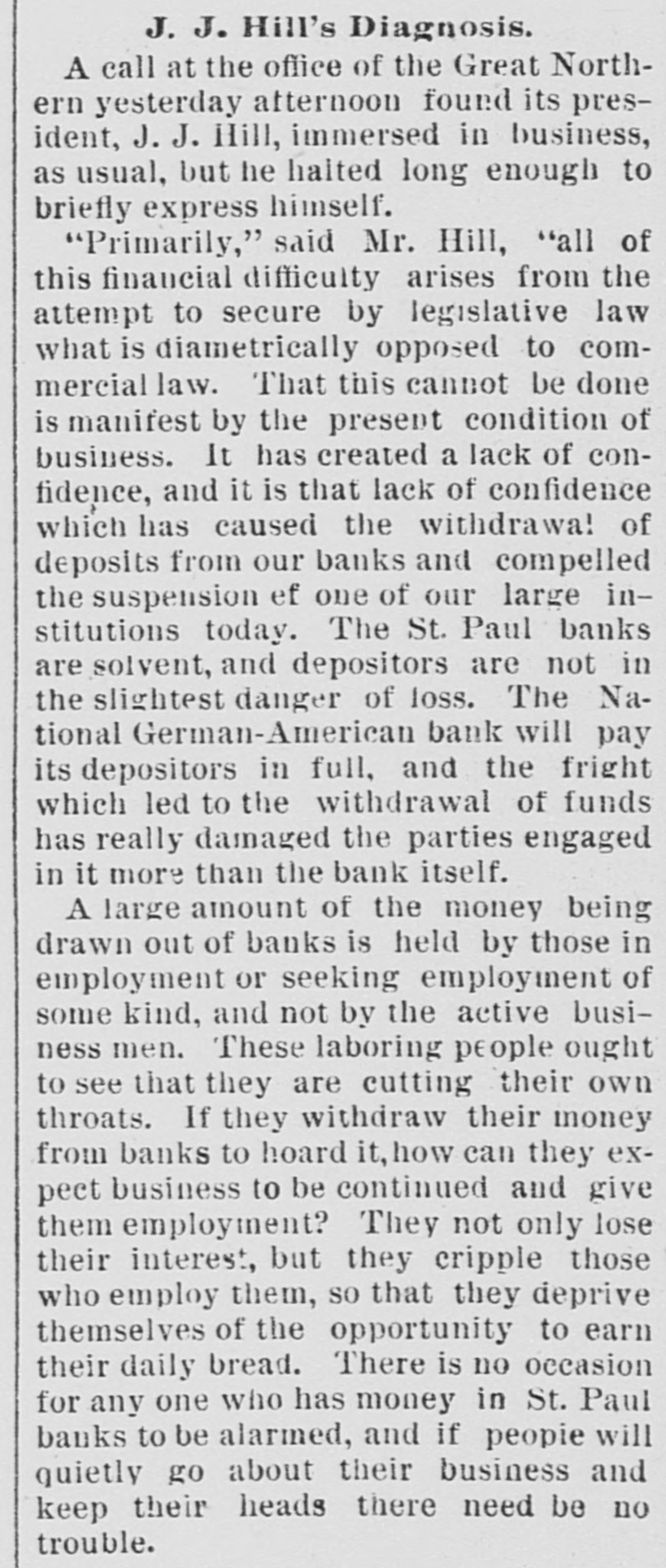

J. J. Hill's Diagnosis. A call at the office of the Great Northern yesterday atternoon found its president, J. J. Hill, immersed in business, as usual, but he halted long enough to briefly express himself. "Primarily," said Mr. Hill, "all of this financial difficulty arises from the attempt to secure by legislative law what is diametrically opposed to commercial law. That this cannot be done is manifest by the present condition of business. It has created a lack of confidence, and it is that lack of confidence which has caused the withdrawal of deposits from our banks and compelled the suspension ef one of our large institutions today. The St. Paul banks are solvent, and depositors are not in the slightest danger of loss. The National German-American bank will pay its depositors in full, and the fright which led to the withdrawal of funds has really damaged the parties engaged in it more than the bank itself. A large amount of the money being drawn out of banks is held by those in employment or seeking employment of some kind, and not by the active business men. These laboring people ought to see that they are cutting their own throats. If they withdraw their money from banks to hoard it, how can they expect business to be continued and give them employment? They not only lose their interest, but they cripple those who employ them, SO that they deprive themselves of the opportunity to earn their daily bread. There is no occasion for any one who has money in St. Paul banks to be alarmed, and if people will quietly go about their business and keep their heads there need be no trouble.

7.August 5, 1893Pawtucket TribunePawtucket, RI

Click image to open full size in new tab

Article Text

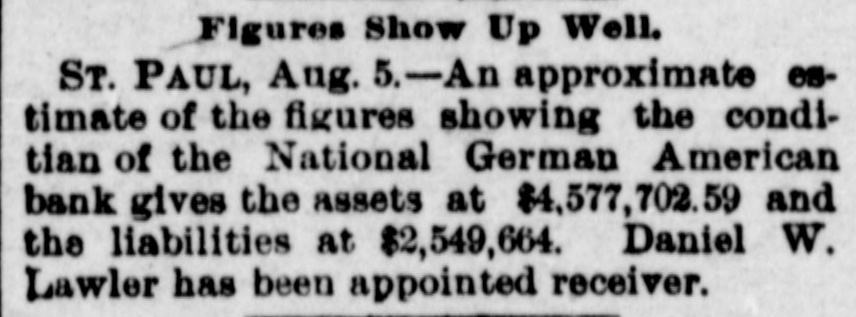

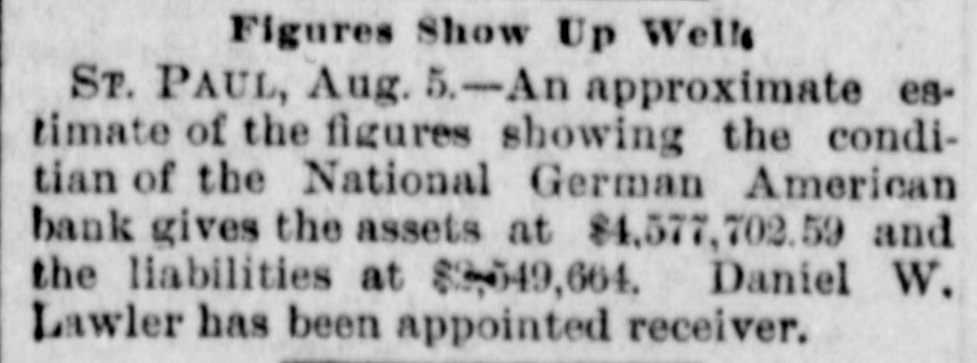

Figures Show Up Well. ST. PAUL, Aug. 5.-An approximate estimate of the figures showing the conditian of the National German American bank gives the assets at $4,577,702.59 and the liabilities at $2,549,664. Daniel W. Lawler has been appointed receiver.

8.August 5, 1893The Providence NewsProvidence, RI

Click image to open full size in new tab

Article Text

Figures Show Up Wells Sr. PAUL, Aug. 5.-An approximate estimate of the figures showing the conditian of the National German American bank gives the assets at $4,577,702.59 and the liabilities at $3,549,664. Daniel W. Lawler has been appointed receiver.

9.August 5, 1893Fort Worth GazetteFort Worth, TX

Click image to open full size in new tab

Article Text

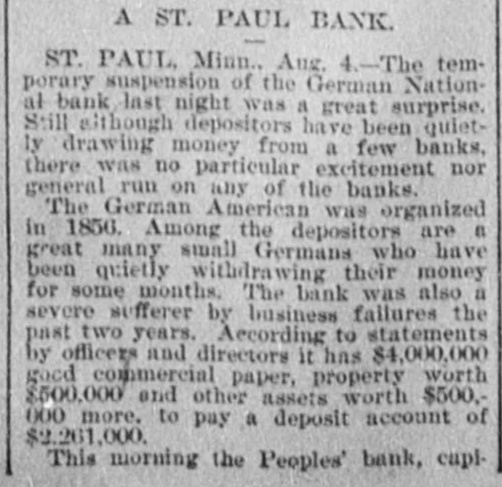

A ST. PAUL BANK. ST. PAUL, Minn., Aug. 4.-The temporary suspension of the German Nationat bank last night was a great surprise. Still although depositors have been quietly drawing money from a few banks, there was no particular excitement nor general run on any of the banks. The German American was organized in 1856. Among the depositors are a great many small Germans who have been quietly withdrawing their money for some months. The bank was also a severe sufferer by business failures the past two years. According to statements by officers and directors it has $4,000,000 good commercial paper, property worth $500,000 and other assets worth $500,000 more. to pay a deposit account of $2,261,000. This morning the Peoples' bank, capi-

10.August 6, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

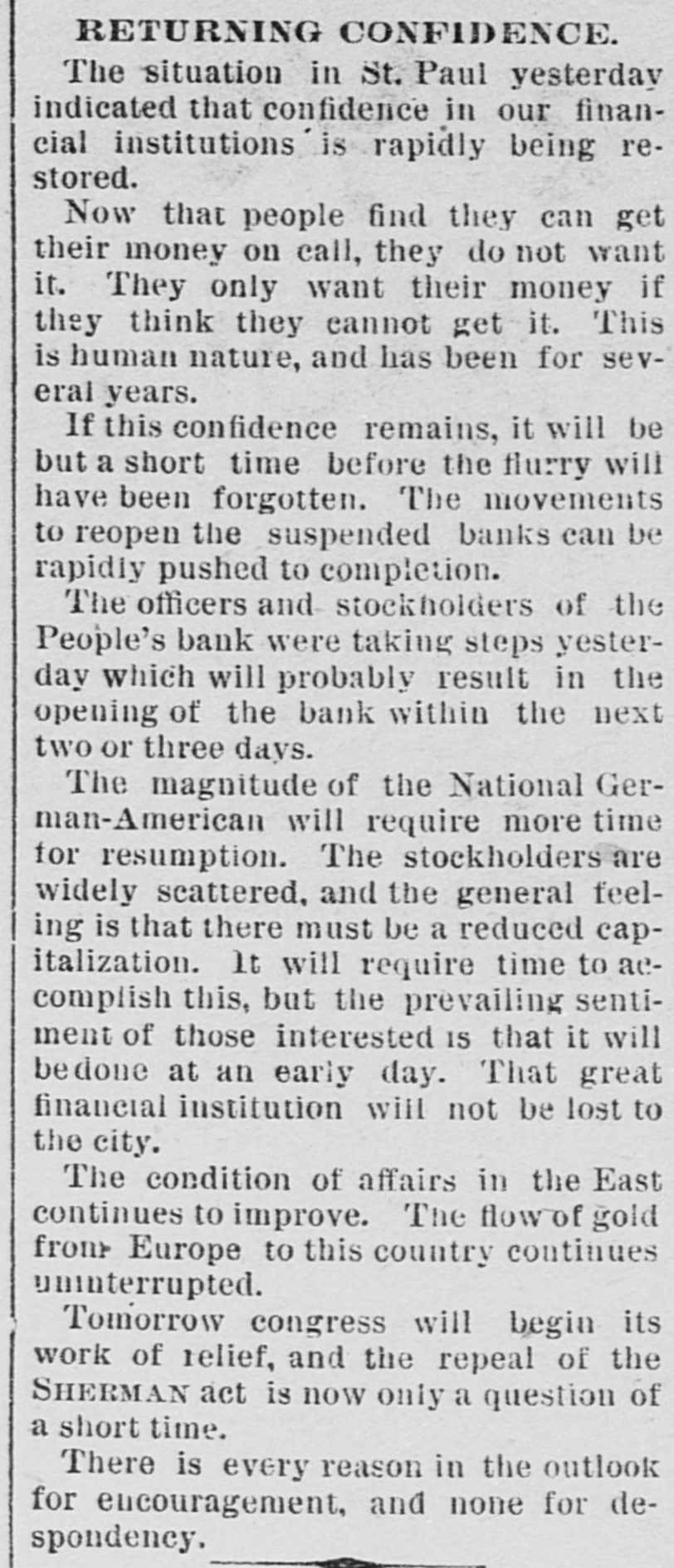

RETURNING CONFIDENCE. The situation in St. Paul yesterday indicated that confidence in our financial institutions is rapidly being restored. Now that people find they can get their money on call, they do not want it. They only want their money if they think they cannot get it. This is human nature, and has been for several years. If this confidence remains, it will be but a short time before the flurry will have been forgotten. The movements to reopen the suspended banks can be rapidly pushed to completion. The officers and stockholders of the People's bank were taking steps yesterday which will probably result in the opening of the bank within the next two or three days. The magnitude of the National German-American will require more time for resumption. The stockholders are widely scattered, and the general feeling is that there must be a reduced capitalization. It will require time to accomplish this, but the prevailing sentiment of those interested IS that it will bedone at an early day. That great financial institution will not be lost to the city. The condition of affairs in the East continues to improve. The flow of gold from Europe to this country continues uninterrupted. Tomorrow congress will begin its work of relief, and the repeal of the SHERMAN act is now only a question of a short time. There is every reason in the outlook for encouragement, and none for despondency.

11.August 8, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

ARRANGING TO RESUME DIRECTORS OF NATIONAL GERMANAMERICAN BANK MEET. MR. LOCKEY AT WASHINGTON. Meeting of Stockholders Called for August 17-Decisive Resumption Measures Then to Be Taken - Everything as Usual at All the Banks-The People's to Resume Business. The situation in financial circles the city as as there no tranquil throughout though yesterday had been was storm last week. There was not the slightest run or anything unusual at any bank in the city. A visit to all of the leadieg banks made the GLOBE by representatives and conversation with the officers showed unusual in progress. nothing The of fact the is, there seems to be a clearing and a sort of a skies, drawing of the long Nabreath since the suspension of tional German-American last week. The difficulties of the bank were, of course, known to the other banks in the city. Whether they should have been averted by clearing house certificates or not is a mooted question, but as that not resorted to, it is needless to on "what measure speculate was might have been." While the bank was in a tremulous condition it was a shadow on the finaneial situation, and that shadow has now been removed. Active steps are being taken for the reorganization and resumption of the bank, as the GLOBE has already indicated. A full meeting of the board of directors of the National German-American bank was held at their rooms in the bank building at 10 o'clock yesterThe local and of the was situation day. country general fully financial discussed and considered. The feeling of the board of directors was not only in favor of resumpbut also that it was praction. unanimous speedy entirely ticable to secure such a result. The decision of the meeting was to call special meeting of the stockholders 17th at is on a the inst., which time will it decisive measures be will result in the expected taken, which enabling bank to resume business as soon as details can be arranged. The capitalization will, undoubtedly, to be reduced $1,000,000, and reduced the capi- bank will be stronger with the Italization than it was before. It is possible that it may not even be necessary to put the bank in the hands of a receiver, but to allow the bank examiner to remain in charge until arrangements can be completed. and the business and assets returned to the stockholders. events, it can be considered as practically sure that the National German-American bank is not going out of existence. and in a very short time will be on its feet again, really strengthened by the temporary disaster which has befallen it, in view of the opportunity thus afforded to reduce the capitalization. A call at the People's bank yesterday Rittenhouse, found his desk. Mr. Rittenhouse the president, at Mr. says arrangements are in progress for speedily resuming business, and from present indications they will be successful. The following announcement. in accordance with this view, appears in our advertising columns today: of certificates of deposit in bank are to "All the People's holders requested that call at the bank immediately arrangements may be made for resuming payment within a few days. C.E. Rittenhouse, President." The People's is so entirely solvent that the matter of resuming is not one of doubt, but a mere matter of adjustment among the parties interested.

12.August 8, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

IN WASHINGTON, Messrs. Lockey, Doran and Lawler Confer With Eckels. Special to the Globe. WASHINGTON, Aug. 7. - National Committeeman Doran, Hon. Dat W. Lawler and President Joseph Lockey, of the National German-American bank, were three prominent Minnesota arrivals at the national capital today. All three gentlemen were closeted with Comptroller Eckels a good part of the afternoon regarding the resumption of the Gerinan-American, and found him willing and anxious to lend all the aid in his power towards bringing out the reopening, of the bank. President Lockey presented a resolution of the board of directors calling a meeting of the shareholders on Aug. 17, and asking that a receiver be appointed until the results of that meeting are known. Comptroller Eckels promptly said that he would not only grant that request, but he would also give a reasonable time after that meeting to enable the bank officials to make arrangements for reopeniug. This was very gratifying to the St. Paul men, and President Lockey left feeling greatly encouraged.

13.August 8, 1893New-York TribuneNew York, NY

Click image to open full size in new tab

Article Text

TROUBLES OF BANKS AND BANKERS. RECEIVERS FOR A NEW-BEDFORD INSTITUTION -A MILWAUKEE BANK TO RESUME New-Bedford, Mass., Aug. 7.-The savings bank commissioners have completed their examination of the affairs of the New-Bedford Safe Deposit and Trust Company. and express their entire satisfaction with the solvency of the institution. The bank has paid out over $200,000 in the last sixty days to depositors, and while the institution had over $40,000 in cash on hand at the time of the suspension, the bank could have at the latest kept on but a day or two longer. The affairs of the bank will be placed in the hands of two receivers, and two New-Bedford men have been nominated for the place. Manchester, N. H., Aug. 7.-Receiver Taggart, of the suspended Defryfield Savings Bank, states that the liabilities of the institution are $252,894. and assets $254,671. He could not state what the loss to stockholders will be as the figures representing the assets are the face value as seen on the books, and no allowance is made for the shrinkage in securities. Springfield, Mo., Aug. 7. The Green County Bank, the oldest in the city, assigned to-day. Liabilities. $137,2421 assets, $252,251. There is some excitement, but no other bank seems to be involved. Milwaukee, Wis., Aug. 7.-Stockholders of the Mil wankee National Bank held a meeting to-day and voted to resume business. Three hundred thousand dollars must be added to the capital stock, and it was voted to raise the money. Pittsburg. Aug. 7.-The principal bankers of Pitts burg. comprising the Clearing House Association, to gether with between thirty and forty of the leading financiers of the city, met at the Clearing House this morning to discuss the financial situation. Several plans were suggested to make the banking Institutions of the city formidable enough to overcome any possi ble emergency that might present itself. No definite plan was adopted. but several are under consideration and will be acted upon finally at a meeting to be held later on. St. Paul. Minn., Aug. 7 (Special).-A meeting of the board of directors of the National German American Bank was held to-day. 11 was decided to call a special meeting of the stockholders on August 17. It is expected that at this meeting arrangements will be perfected for the bank to resume business at an early date. The People's Bank reports that it will resume business soon.

14.August 9, 1893Morris TribuneMorris, MN

Click image to open full size in new tab

Article Text

Financial Flurry In St. Paul. Sr. PAUL, Aug. 7.-St. Paul experienced a financial flurry this week. Four banks suspended payment. They were the National German-American, West Side, Seven Corners and Peoples. They were all smali banks except the German-American, which had a capita! os $2,000,000. All but the Seven Corners bank will resume in a short time.

BUSINESS TROUBLES. Suspension at St. Paul. ST. PAUL, Minn., Aug. 5.-The National German-American bank failed to open its doors Friday and announced a temporary suspension consequent upon a steady drain of withdrawals for the past month. The bank officials announce that every liability will be made good dollar for dollar, but they require time to realize on their securities. No statement of liabilities and assets is as yet obtainable. An approximate estimate of the figures showing the condition of the bank gives the assets at $4,577,702.59, and the habilities at $2,549,664. Daniel W. Lawyer has been appointed to assume charge of the affairs of the bank. The People's bank, of St. Paul, which closed its doors at noon, has a capital stock of $240,000. No detailed statement of the affairs of this bank can be obtained before tomorrow. The same can be said of the West Side bank, a small concern, which closed its doors at 1 o'clock.

16.August 16, 1893Morris TribuneMorris, MN

Click image to open full size in new tab

Article Text

Winona papers contain complaint of the

slaughter of prairie chickens in that

vicinity.

D. L. Keible, state supervisor,

will resign to accept a position in

the state university.

Undertakers of North and South

Dakota will hold a convention at Min-

neapolis Sept. 12, 13 and 14.

St. Paul's crack boat club, the Min-

nesotas, took two races at Detroit last

week—the senior and junior fours.

Flour rates were reduced 2 1-2 cents

per 100 pounds from Duluth and Min-

neapolis to Eastern points Aug. 14.

D. N. Dumont, G. N. A. Fostier and

J. G. Milspaugh will be appointed pen-

sion examining surgeons at Little Falls.

The National German-American bank

at St. Paul will probably reorganize

without the appointment of a receiver.

Burglars cracked the safe of Matt

Smith at Cambridge. They secured

$200 cash and some watches and revol-

vers.

The Princeton village council has de-

cided to put in a system of waterworks

for fire protection and to establish fire

limits.

Emil Johnson of Spring Lake was

fined $10 and costs, amounting in all to

$19.15, by Justice Barton of Inver

Grove for spearing a buffalo fish.

The Polish Catholic controversy at

Winona is ended. The Poles met last

week and agreed to obey the bishop and

accept a priest other than Father Mic-

iszke.

While M. M. Crandall was cutting

grain near Verndale he was badly in-

jured by the accidental discharge of a

shotgun which he was carrying on the

binder.

Nearly 600 applications have been re-

ceived by the Minnesota state grain and

warehouse commission for elevator

licences under the new law that went

into effect Aug. 1.

Louis Freedman, a peddler living in

St. Paul, had his left ear nearly severed

while engaged in a fight with Charles

Baker and Fred Guion. Baker and

Guion were arrested.

Montana merchants have started a

boycott on St. Paul and Minneapolis

because of the attitude of these two

cities as reflected in their newspapers

on the financial question.

STATE OF OHIO, CITY OF TOLEDO,

ss.

Lucas County,

Frank J. Cheney makes oath that

he is the senior partner of the firm of

F. J. Cheney & Co., doing business

in the City of Toledo, County and

State aforesaid, and that said firm

will pay the sum of One Hundred

Dollars for each and every case of

Catarrh that cannot be cured by the

use of Hall's Catarrh Cure.

FRANK J. CHENEY.

Sworn to before me and subscribed

in my presence, this 6th day of De-

cember, A. D. 1886.

A. W. GLEASON,

Notary Public.

Hall's Catarrh Cure is taken in-

ternally and acts directly on the

blood and mucous surfaces of the

system. Send for testimonials, free.

F. J. CHENEY & CO., Toledo, O.

Sold by all druggists 75c.

17.August 24, 1893The Prison MirrorStillwater, MN

Click image to open full size in new tab

Article Text

The intense folly of withdrawing deposits from sound banks in times of commercial stress was never more clearly illustrated than by withdrawal of funds from the National German-American bank of St. Paul, which so depleted it of current funds as to force suspension. With assets nearly double its liabilities, a well conducted and prosperous bank was knocked out of the business swim by those who should have been its best friends. For fear of losing a small current deposit, these fools congest the whole financial condition of an aiready heavily burdened country.

18.October 1, 1893St. Paul Daily GlobeSaint Paul, MN

Click image to open full size in new tab

Article Text

DEPOSITORS' EXTENSIONS ABSOLUTELY NECESSARY FOR GERMAN-AMERICAN TO RESUME. TALK WITH EXAMINER LYNCH. Meeting of the Bank Directors Yesterday - Mr. Lynch Tells Them What Must Be DoneDepositors Hold the Key They Can Secure Resumption and Their Money Shortly. A largely attended meeting of the di rectors of the National German-American bank was held yesterday, every director in the city being present. A. D. Lynch, of Washington, the special national bank examiner, was present to confer with the directors. Mr. Lynch devotes his entire time to investigating suspended national banks and aiding in their resumption or liquidation, as the case may be. He made a lengthy address to the directors, setting forth what was necessary for the bank to resume business. His views were excellently received and heartily coincided with, and the directtors propose to act along the lines laid down by him. A GLOBE representative called upon Mr. Lynch after the meeting, and received in substance the following: "It is evident," said Mr. Lynch, "that further extensions on the part of depositors are absolutely necessary, and, if they are not granted, resumption of the bank may be defeated. 1 consider that the officers of the bank have done excel lent work. They have collected $400,000 in cash, and secured extensions of deposits amounting to $1,482,000; but this is not enough. If the depositors do not grant the extensions a receiver will necessarily be appointed, and under the best administration possible it is not improbable that four years, if not more, would be required for liquidation of the trust. Through the plan now.proposed, the bank can be placed in a going condition, and those having deposits can obtain their money in the ordinary course very much earlier than if the bank should be forced into liquidation, Depositors should not wait to be called upon, but should call at the bank without delay and grant extensions. Doing so, they act in their own interests. If this is done, the bank can resume in a very short time. I cannot too strongly impress upon the depositors their interests and their duties in this matter. The directors, through their committee, are making the necessary collections and obtaining money required to perform their duty, but they must have the co-operation of the depositors, or all this will come to naught. There must be enough money secured, together with the extensions of the depositors, to enable the bank to meet the demand liabilities, as well as for a working capiital. I shall send the comptroller in a day or two a report of the present condition of affairs, and it is probable some representatives of the bank will visit Washington very shortly

The National German-American bank of St. Paul will reopen its doors Oct. 23, and again do business. Its suspension was caused by the cowardly, who withdrew their cash just when the presence of cash was most needed and most unattainable. With assets almost double its liabilities, this sound concern was forced, for self-protection, to assign owing to foul blows from its supposed friends. Executive clemency in the case of Thompson the De Smet, S. D., murderer may be wisely exercised. But it would seem that when a jury and judge, these days. find a man guilty of a shocking, cold-blooded murder, and sentence him to be hanged in expiation, that that sentence should be carried out. Such cases of emotional leniency do not seem to benefit the cause of justice, law and order; but rather are inclined to antagonize the people towards them and incite disorder. In a speech in the Rotunda at Dublin. John Redmond, the Parnellite faction leader, clearly indicated that he and his followers had had enough of "the grand old" fraud, who had no more use for Ireland after the Irish had plucked the official chestnuts out of the political fire. Mr. Redmond declared that his faction would no longer vote with the Liberals on English questions. He eulogized Parnell and declared his belief in the lack of patriotism of the other wing of the Irish party. The closing scenes of the bi-metallic congress were pitifully ludicrous. A few earnest men striving to arouse enthusiam and attract the nation's attention which would not be attracted by their theories. Gov. Tillman mingled negro domination and Grant's bayonets with his belief that the South and West could control the presidency. Gov. Lewelling spoke of Kansas having sent ex-confederates to congress and the convention exhausted itself in cheering, and adjourned to meet at Atlanta, Ga., next year. The Ameer of Afghanstan shows his appreciation of Neil's genius, who during the Indian mutiny, promptly stopped assassinations by blowing the fanatics from a cannon's mouth. The dismemberd Moslem can not achieve his Paradise. To assassinate an infidel and be hanged is glorious martyrdom to the Moslem fanatic; to be shot to pieces is death and damnation combined. The Ameer saw the force of this argument and promptly put down his revolting soldiery by blowing the ringleaders to pieces,

20.October 20, 1893Daily Kennebec JournalAugusta, ME

Click image to open full size in new tab

Article Text

NEWS IN A NUTSHELL. The World's fair will close officially Oct. 30. The Ameer of Afghanistan is selling h's captives into slavery. The missing steamer Miowera isstranded in the harbor of Honolula. The ravages of the cholera epi- emic Il Constantinople is increasing, There was is serious wreck on the Cana dian Pacific, near Grand River. Lord Chelmsford says the Matabeles are the equals of the Zulus as fighters. Sir Julian Pauncefote and family have left Newport, R. L. for Washington. The Hutchinson National bank of Hutchinson, Kan., has closed its doors to business. It has been decided to reopen the National German-American bank of St. Paul on Oct. 30. The First National bank of Ouray, Colo., which suspended about two months ago, has resumed business. The president sent to the senate a con fidential communication in response to the resolution of Mr. Dolph asking for information as to whether the Chinese government had made any request for the suspension of the exclusion act. The doeument is very brief, and will not be opened except in executive session.

21.October 31, 1893The Evening WorldNew York, NY

Click image to open full size in new tab

Article Text

Business Ups and Downs. ST. PAUL. Minn., Oct. 31-The reorganized National German-Ainerican Bank. which closed its doors during the financial stringency ARE 1. reopened yesterday. ST. PAUL, Minn.. Oct. 31.-Judge Caldwell, of the United States Circuit Court. has appointed F. C. Hills, of Sioux City, receiver of the Sionx City, O'Neill and Western Railroad. on the upplication of the Manbattan Trust Company. of New York. TIFFIN, O., Oct. -The strike at the Sneath Glass Works occasioned by the management discharging a union blower was settled and the men 11 returned to work yesterday. BOULDER. Col., Oct. 81.-All the coal miners at Lafayette, Louisville and Erie have gone to work. MILWAUKEE. Oct. 31.-William Plankinton said yesterday that early in December he would pay. as assignee for the Plankinton Bank, a dividend of 15 or 20 per cent., and that that would be the only dividend paid this year. DULUTH. Minn., Oct. 31.-J. 11. Sutphin. for a number of years prominent in Duluth in busiless and politics. made an assignment yesterday.