Click image to open full size in new tab

Article Text

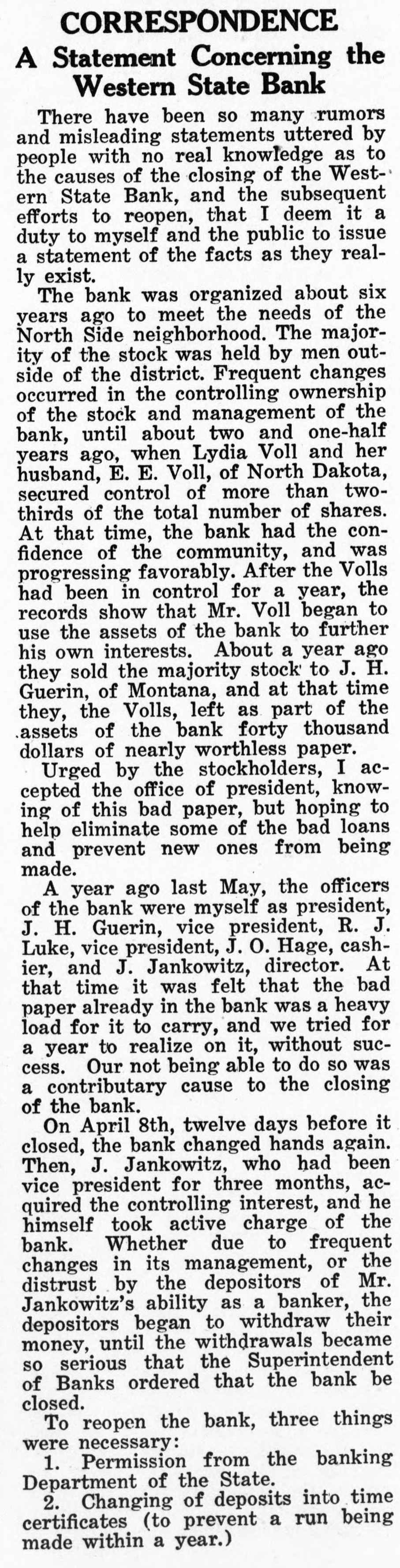

CORRESPONDENCE A Statement Concerning the Western State Bank There have been so many rumors and misleading statements uttered by people with no real knowledge as to the causes of the closing of the Western State Bank, and the subsequent efforts to reopen, that I deem it a duty to myself and the public to issue a statement of the facts as they really exist. The bank was organized about six years ago to meet the needs of the North Side neighborhood. The majority of the stock was held by men outside of the district. Frequent changes occurred in the controlling ownership of the stock and management of the bank, until about two and one-half years ago, when Lydia Voll and her husband, E. E. Voll, of North Dakota, secured control of more than twothirds of the total number of shares. At that time, the bank had the confidence of the community, and was progressing favorably. After the Volls had been in control for a year, the records show that Mr. Voll began to use the assets of the bank to further his own interests. About a year ago they sold the majority stock to J. H. Guerin, of Montana, and at that time they, the Volls, left as part of the assets of the bank forty thousand dollars of nearly worthless paper. Urged by the stockholders, I accepted the office of president, knowing of this bad paper, but hoping to help eliminate some of the bad loans and prevent new ones from being made. A year ago last May, the officers of the bank were myself as president, J. H. Guerin, vice president, R. J. Luke, vice president, J. O. Hage, cashier, and J. Jankowitz, director. At that time it was felt that the bad paper already in the bank was a heavy load for it to carry, and we tried for a year to realize on it, without success. Our not being able to do so was a contributary cause to the closing of the bank. On April 8th, twelve days before it closed, the bank changed hands again. Then, J. Jankowitz, who had been vice president for three months, acquired the controlling interest, and he himself took active charge of the bank. Whether due to frequent changes in its management, or the distrust by the depositors of Mr. Jankowitz's ability as a banker, the depositors began to withdraw their money, until the withdrawals became so serious that the Superintendent of Banks ordered that the bank be closed. To reopen the bank, three things were necessary: 1. Permission from the banking Department of the State. 2. Changing of deposits into time certificates (to prevent a run being made within a year.)