Click image to open full size in new tab

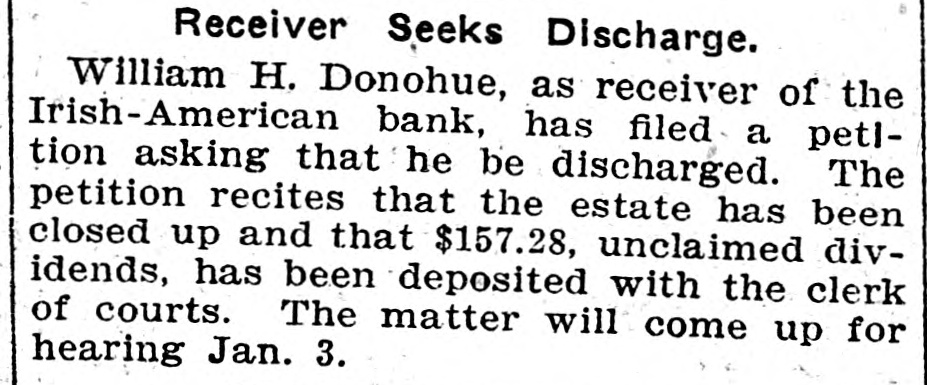

Article Text

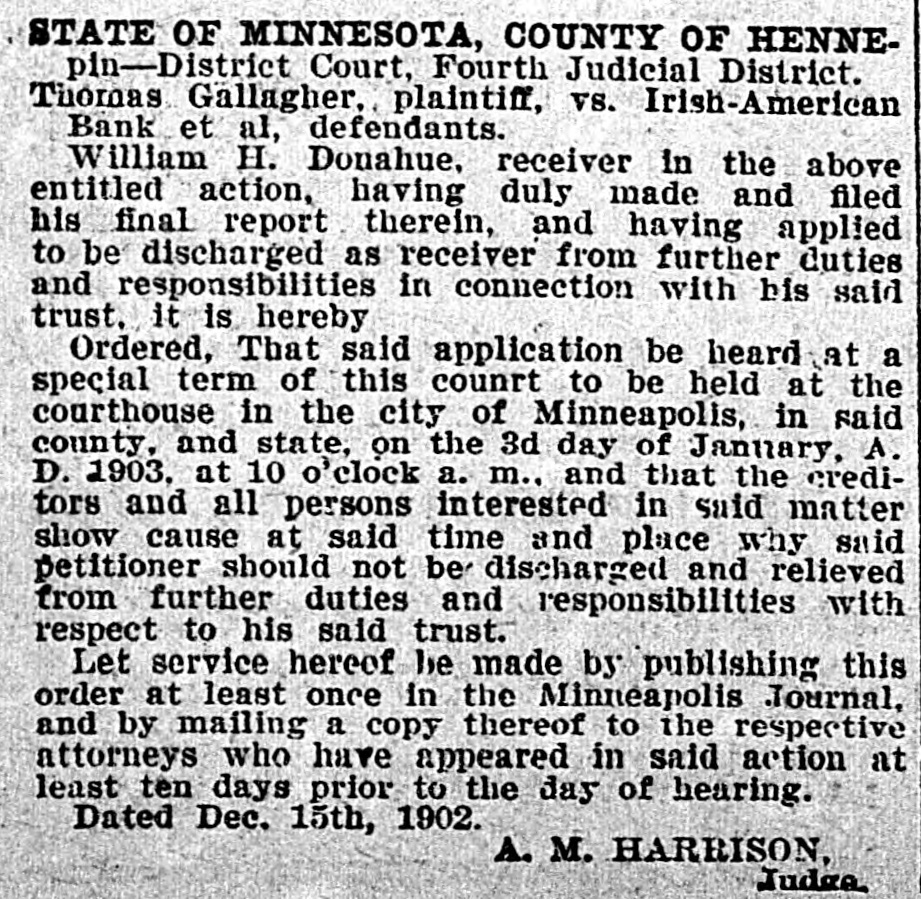

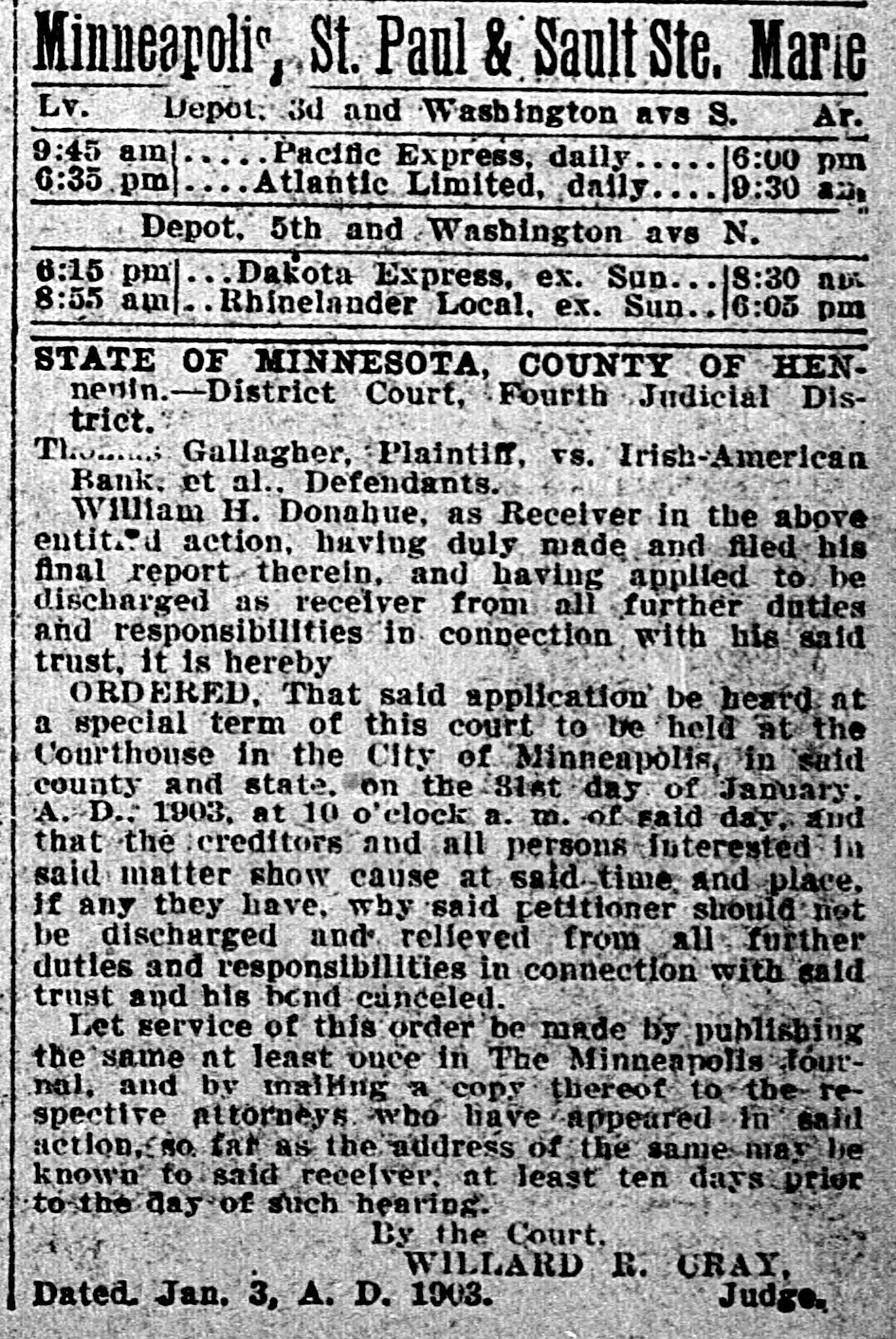

Minneapolis, St. Paul & Sault Ste. Marie Lv. Depot. 3d and Washington avs S. Ar. 9:45 am Pacific Express, daily 6:00 pm 6:35 pm Atlantic Limited, daily 9:30 any Depot. 5th and Washington ave N. 6:15 pm 8:30 am Dakota Express, ex. Sun... 8:55 am Rhinelander Local, ex. Sun. 6:05 pm STATE OF MINNESOTA, COUNTY OF HENnewin.-District Court, Fourth Judicial District. Thomas Gallagher, Plaintiff, vs. Irish-Amerlcan Bank. et al., Defendants. William H. Donahue, as Receiver in the above entit. action, having duly made and filed his final report therein, and having applied to be discharged as receiver from all further duties and responsibilities in connection with his said trust, it is hereby ORDERED, That said application be heard at a special term of this court to be held at the Courthouse in the City of Minneapolis, in said county and state. on the S1st day of January. A. D., 1903, at 10 clock a. m. of said day, and that the creditors and all persons Interested In said matter show cause at said time and place, if any they have, why said petitioner should not be discharged and relieved from all further dutles and responsibilities in connection with said trust and his bond canceled. Let service of this order be made by publishing the same nt least once in The Minneapolis fournal, and by malling a copy thereof to the respective attorneys who have appeared in said action, SO. far as the address of the same may be known to said receiver, at least ten days prior to the day of such hearing. By the Court. WILLARD R. GRAY, Dated. Jan. 3, A. D. 1903. Judge,