Click image to open full size in new tab

Article Text

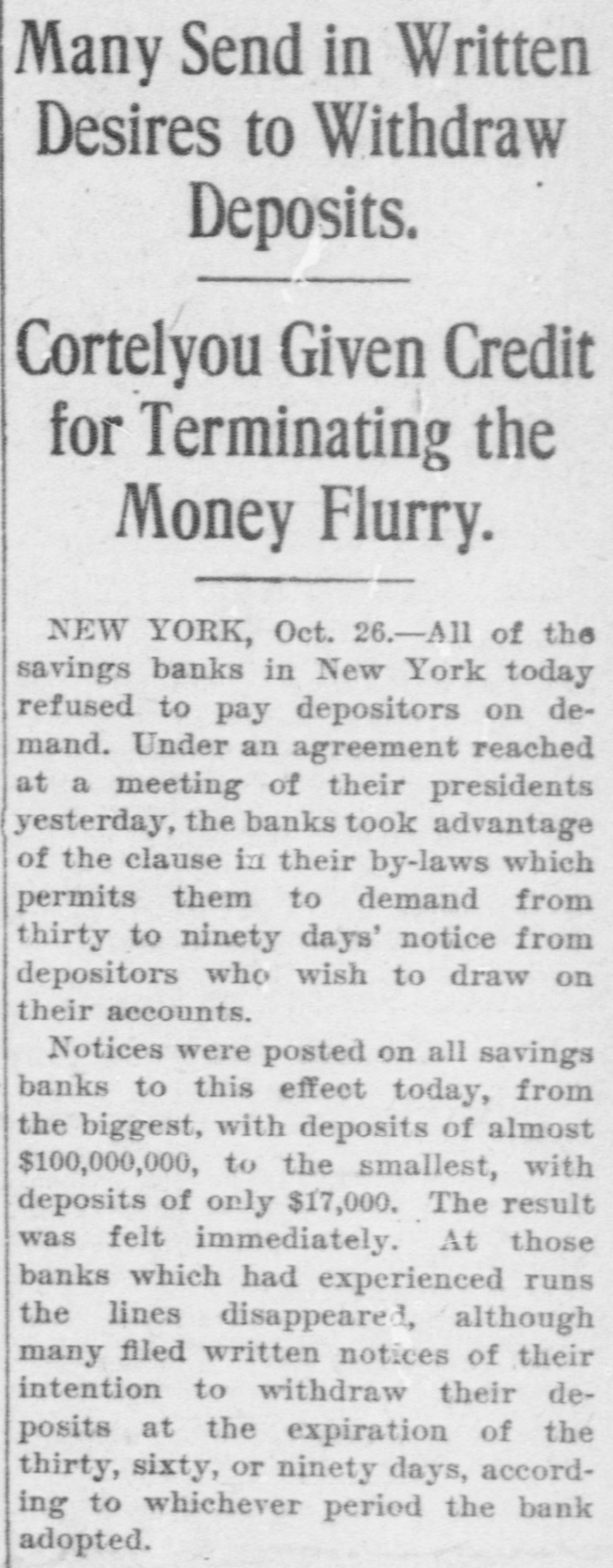

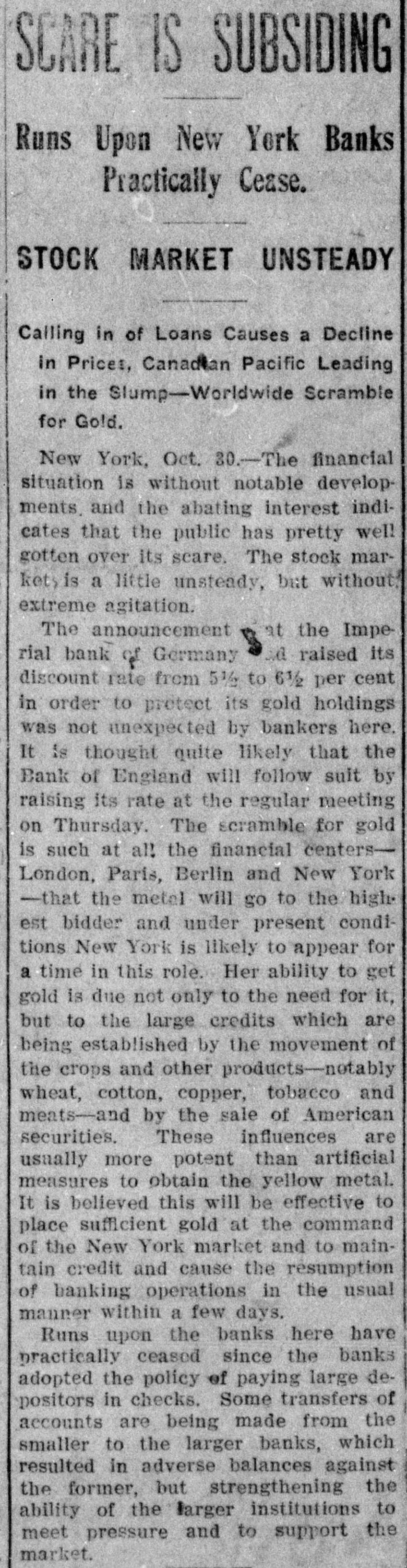

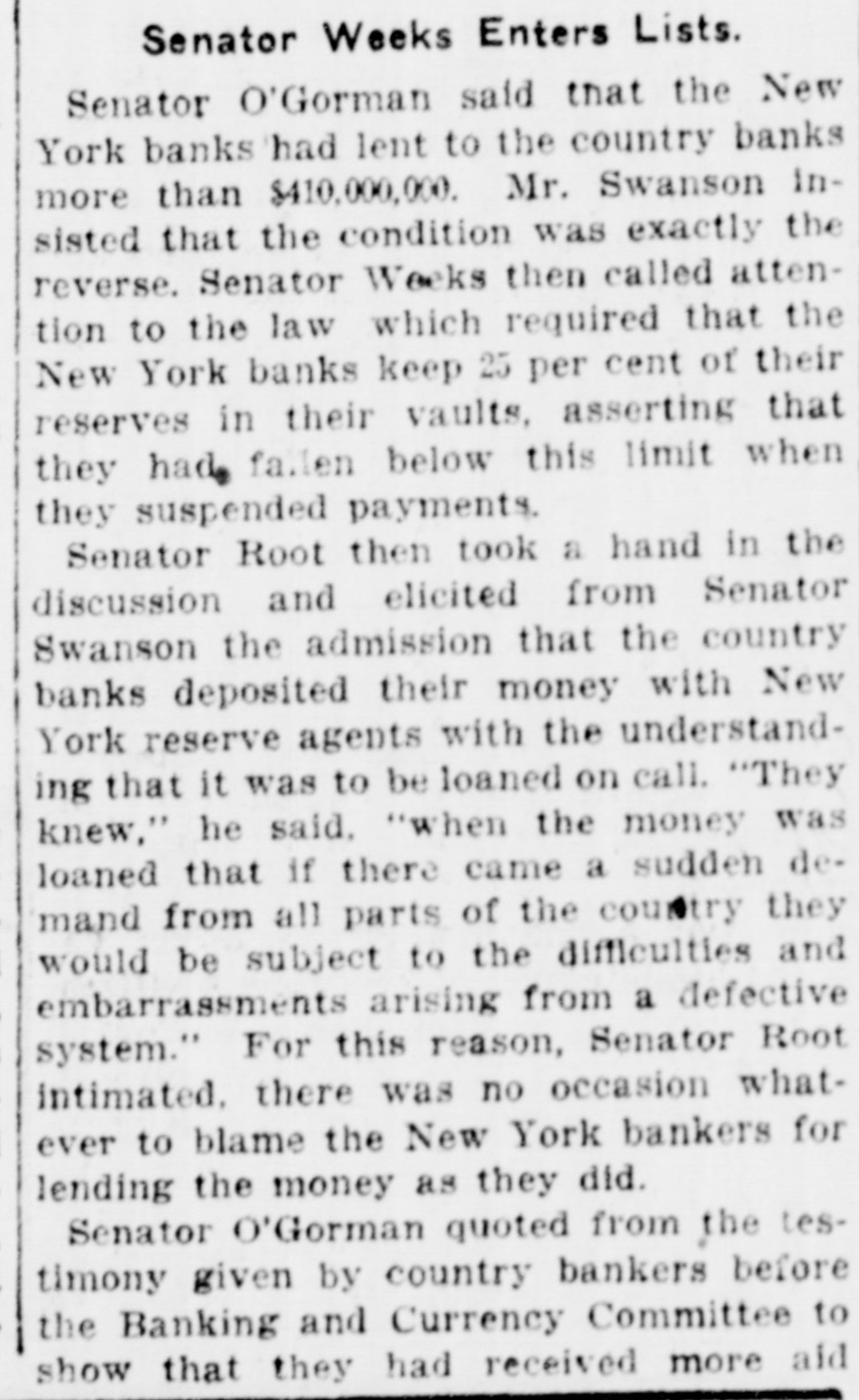

James C. Hallock, of Brooklyn, whose father originated the clearing house in America, and who has himself studied the subject of clearing houses for many years, said yesterday in an interview with a representative of The Washington Herald: "Thirty-two thousand depositors in Brooklyn, probably 100,000 in Greater New York, had accounts in failed banks last winter. of the "Millions have citizens distrust throughout Wall Union come to street as a stewpot of panics, which boils over unexpectedly. The American people would rejoice to see Congress enact a law which would protect the country against financial disturbance from that quarter. Favors Legislative Action. a few men in New York scream as If were to killed. would "Possibly they be than But even in battle many more are killed think they are going to be. However, it is true, I wish our Representatives would rise as one man and render harmless some New York/ bankers, who could be crushed as easily as a spider. "Understand that the principal banks in the city belong to a union; yet they let one of their number suspend and deserted five, forcing four to fail, so that for months there have been closed banks on whose dusty windows the passing throng have been reading a shameless advertisement of desertion in the soiled letters, 'Member of the New York Clearing House. "Cannot even its members be trusted? Now, though these broken banks suffered losses which their shareholders have had to bear, every one of the six will resume or pay depositors in full. "Their funds would have far exceeded their liabilities to depositors. if a little time had been allowed them to realize on their assets. Banking in New York Safe. in New York is conducted more safely than suppose. much "Banking since people National Not the Marine Bank failed, in 1884, with a net loss to depositors of $765,800, has a dollar been lost by depositors of failed national banks in the city of New York. The only other net loss that ever occurred was $25,612 by the failure of the Croton National Bank, 1867; that is to say, less than $800,000 years of of less than a year, in in an forty-five average national $18,000 banking, with no net loss at all for the past twenty-four years. "St. Louis has had only one net loss from the failure of a national bank, $38.428, in 1887, an annual average of less than $860. with no net loss at all for over twenty years. Chicago has had four small aggregating $462,453 since 1675. for of only $14,000 thirty-three years, no net net an the average losses, past annually with loss since 1893. "In short, the national banks of New York are so absolutely safe that they could guarantee each other's deposits without practically any risk. When the occurred on the Mercantile National runs Bank, First National Bank of Brooklyn, National Bank of North America, and New Amsterdam National Bank, all the other national banks in the city receive could without peril have offered to checks on them for deposit. What Existing Lew Requires, "National banks are required by law at par any and all notes or by other national to bills to receive issued banks. power Conunder its constitutional gress, promote the general welfare, should also compel the national banks of New York to accept checks on any of their number. "There can be no question that it would promote the general welfare. History shows that in this country no great panic anywhere but in New York, could not be one if at has and there started bank all there times checks on every national were accepted by all. "Bank notes are always received, bank that issued them may So, in New York, na- on banks should be though the national have though failed. the received bank checks drawn by on or bad, open or banks have lost nothing the tional were tional good banks, notes. closed. by And receiv- Nspar national bank would lose New on receiving national ing nothing at in banks the end of by York checks under other national banks in the city, all circumstances. Bank Assassinations. "Investigation would show that more New of the closed banks in banks than one assassinated by other York were The offense of bank assassination dethere. in its nature. To protect is criminal against the effects of bank of as- repositors the criminal character national sassination, accept checks on other recognized banks fusals' of to New York, should be the law of the land. New in refuse checks drawn temporarily on a "To bank. which, though meet York has sufficient funds to is a them by mischief embarrassed, any process of liquidation, which, if it form of malicious the bank, may annoy results in closing thousands of citizens, credi- with and their injure wives, children, parents, and of tors. "In New York thy it brother?" is the old And story he anCain. 'Where know is not. Am my What brother's hast swered: 'I the Lord said, keeper?' Then voice of thy brother's from the blood thou done? crieth to The me earth. York, Concern in New Mutual New York banks assert the since right "The their brother's keeper. following Ever the to be 1884, in the month the June 4. Marine National Bank, emfailure committee has for clearing of house the considered been it whenever it examine the interest of the powered, of the association, to and the any bank member from any member association, securities as to require amount and character for the committee might resulting the of protection such exchanges an of the of balances deem clearing sufficient house. bank from or the every non-member member same institution "Since 1890 submit clearing to through the members a examinahas had to of are as required tions