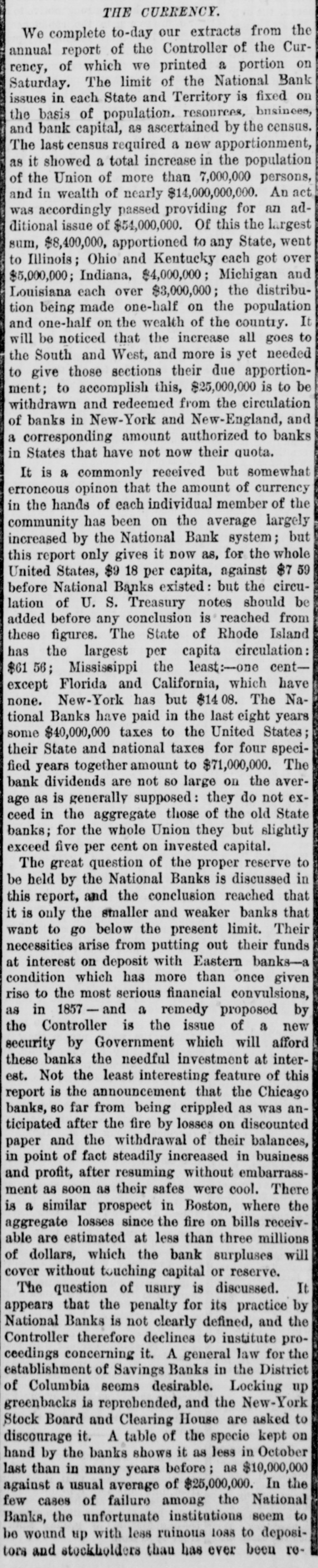

Click image to open full size in new tab

Article Text

CHICAGO, TUESDAY, OCTOBER 14, 1873.

NEWS.

indication, and gave a tone to the

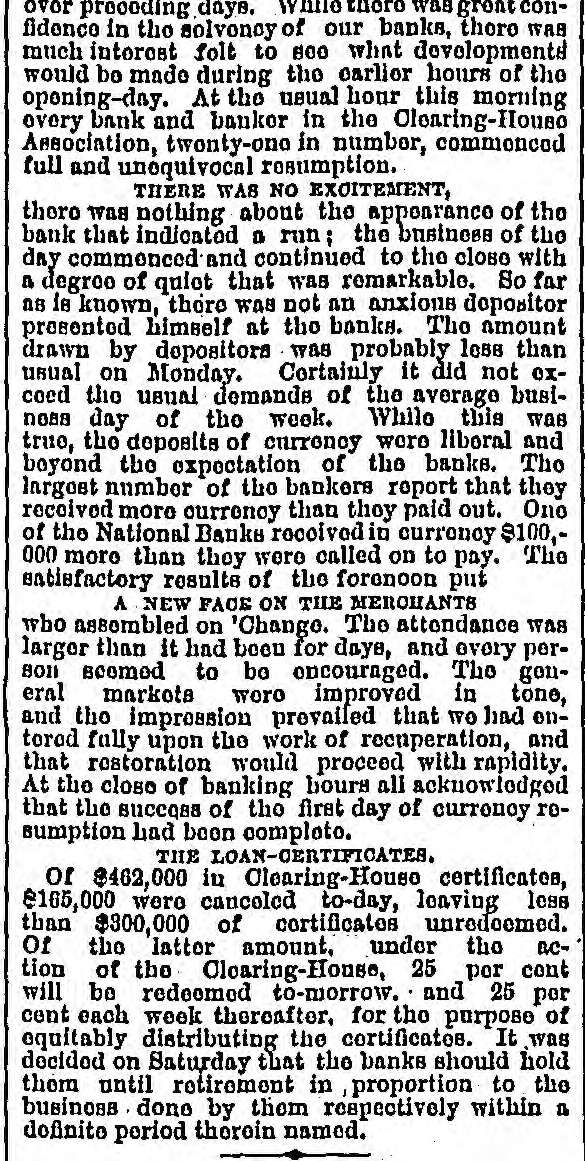

general markets that was in improvement

over preceding days. While there was great con-

fidence in the solvency of our banks, there was

much interest felt to see what developments

would be made during the earlier hours of the

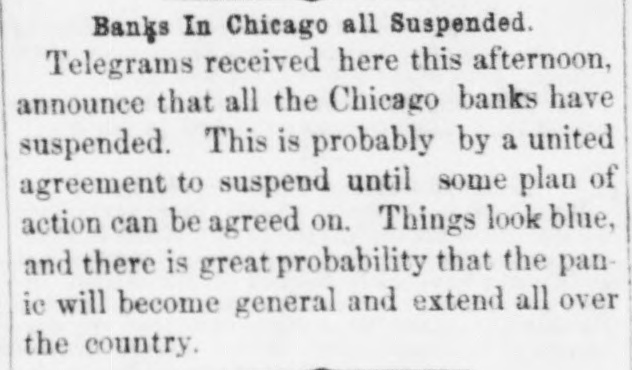

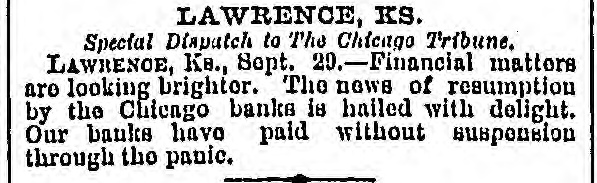

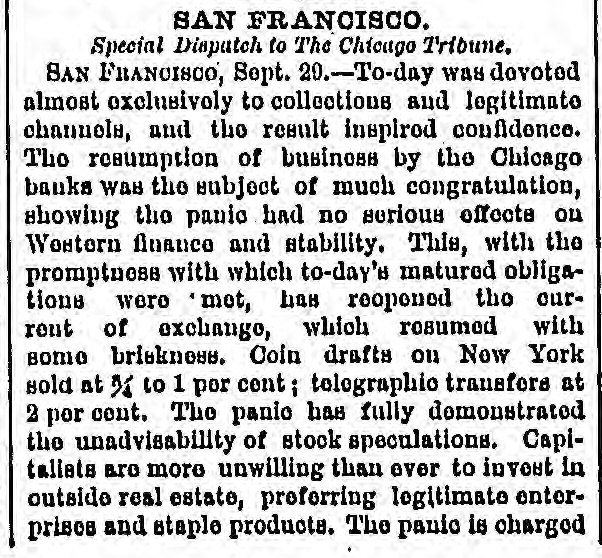

Bank to Re- opening-day. At the usual hour this morning

This every bank and banker in the Clearing-House

Association, twenty-one in number, commenced

full and unequivocal resumption.

THERE WAS NO EXCITEMENT,

there was nothing about the appearance of the

bank that indicated a run; the business of the

day commenced and continued to the close with

ply to the a degree of quiet that was remarkable. So far

nts. as is known, there was not an anxious depositor

presented himself at the banks. The amount

drawn by depositors was probably less than

usual on Monday. Certainly it did not ex-

ceed the usual demands of the average busi-

noss day of the week. While this was

true, the deposits of currency were liberal and

boyond the expectation of the banks. The

largest number of the bankers report that they

received more currency than they paid out. One

e Cincinnati of the National Banks received in currency $100,-

Ex- 000 more than they were called on to pay.

Satisfactory results of the forenoon put

A NEW FACE ON THE MERCHANTS

who assembled on 'Change. The attendance was

larger than it had been for days, and every per-

son seemed to be encouraged. The gen-

o Injunction eral markets were improved in tone,

n South- and the impression prevailed that we had en-

tered fully upon the work of recuperation, and

that restoration would proceed with rapidity.

At the close of banking hours all acknowledged

that the success of the first day of currency re-

sumption had been complete.

THE LOAN-CERTIFICATES.

Of $462,000 in Clearing-House certificates,

$165,000 were canceled to-day, leaving less

Have to Say to than $300,000 of certificates unredeemed.

entions. Of the latter amount, under the ac-

tion of the Clearing-House, 25 per cent

will be redeemed to-morrow, and 25 per

cent each week thereafter, for the purpose of

equitably distributing the certificates. It was

decided on Saturday that the banks should hold

them until retirement in proportion to the

adelphia Pre- business done by them respectively within a

eduction definite period therein named.

NEW YORK.

Special Dispatch to The Chicago Tribune.

THE INJUNCTION AGAINST SALES OF STOCK.

NEW YORK, Oct. 13.-Judge Blatchford ren-

ONAL. dored, to-day, in the United States District

ors of the Union Court, the following decision in the case of

, it was unani- George Bird Grinnell & Co., modifying the in-

iness as usual at junction obtained by Henry Myers, restraining

Blake Bros. & Co. from disposing of certain bonds

and stocks:

ommunication of In this matter on motion of Blake Bros. & Co., let an

in THE TRIBUNE order be entered modifying the injunction, so as to

adopted: allow them to sell, according to the method of the

CHICAGO, Oct, 13. New York Stock Exchange, all stocks and bonds re-

umercial National maining in their hands, specifying the same, men-

tioned in the affidavit of W. O. Olcott

as having been deposited with Blake Bros.

with profound & Co. by George Bird Grinnell & Co.

n of the 10th inst., as collateral security, and to use the proceeds as if

Bank should re- they were their own moneys, subject, however, and

ausiness at once. receiving the right and power of this Court in case an

r continued con- adjudication in bankruptcy and subsequent proceed-

institution. We ings thereon to ascertain and liquidate liens and

cois not misplaced. specific claims which have been or may be set up by

of the Currency, Blake Bros. & Co., in respect to all or any of said

meeting held this stocks and bonds, or of the proceeds of the same,

reopen the Union and to manage and dispose of such proceeds,

inst. Thanking and reserving the right to any Assignee in bank-

of good will and ruptcy who may be appointed herein to question

by suit or otherwise the validity of the pledge

of securities deposited with Blake Bros. & Co.

Св, by George Bird Grinnell & Co., on Sept. 10, 1873, name-

AUGH, President, ly: 500 shares of the capital stock of the Union Rail-

egrams from tho way Company, 400 shares of the common capital stock

stating that the of the Chicago & Northwestern Railway Company, and

the bank was il- 10,000 shares registered Lake Shore & Michigan South-

free to resume ern Railway Company's sinking-fund bonds; and the

ened. validity of the pledge of 30,000 of the last described

bonds deposited with Blake Bros. & Co. by George

informality con- Bird Grinnell & Co. on Sept. 26, 1873, and reserving

Le voto was takon the right of such Assignee to question, in like

n, some of the manner, the right of Blake Bros. & Co. to

creas the law re- hold the surplus securities given on one

oting shall bo by loan for a deficiency on any other loan, and reserving

"his provision of the right to such Assignee to compel Blake Bros. &

the time the ac- Co. to account to him in respect to the disposition and

application of the proceeds of all securities deposited

with Blake Bros. & Co., as mentioned in said affidavit

ago Tribune. of Olcott, whether such securities have been already

isdom of the do- sold or are yet unsold. This modification to be sub-

s city, on Satur- ject to the condition that Blake Bros. & Co. shall file

ments, has been in this Court, within two days after the future

Co-day. At near- sale of any of said securities, a sworn state-

gain in currency, ment of the particulars of the same. A pro-

ith unexpected vision must be inserted, in order that nothing

Juntarily retired contained in it shall be construed as a direction of

ertificates. The the Court for the same securities within meaning of

ely light, and the Sec. 22 of the Bankruptcy act, or otherwise as imply-

he banks are not ing any assent by George Bird Grinnell & Co. to the

sale, so far as such assent was or is necessary under

the terms of the contracts of pledge. This order will

be settled on notice to debtors and petitioning

The Clearing-House Committee appointed, on

application of President Ellis, of the Bank of the

Commonwealth, to investigate the condition of

that establishment, with a view to a refutation

of the statements of Receiver Bailey, reported

to-day fully sustaining the charges of Mr.

Bailey.

DREADSTTFFS.

The flour market was exceedingly dull and

heavy. Old family winter wheat and spring

extras are in reduced supply and firmly

hold. Good superfine steady and fairly

active. At the close the market was

lower for low and medium grades. Little change

in the value of wheat, but the unfavorable news

from Europe and liberal arrivals give buyers an

advantage. The only feature of the market to-

day is a more active demand for commercial

sterling. The market closed with a demand

chiefly for export.

FREIGHTS.

The market for freights was fairly active, but

rates were not materially changed, though

tending in shippers' favor. In the charter-

ing line there was a moderate demand for vessels

suitable to the grain trade at previous rates.

[To the Associated Press.]

NEW YORK, Oct. 13.-Papers were served to-

day in the suit of William Scott, of Erie, Pa.,

against Kenyon Cox & Co. This suit is intend-

ed to restrain Daniel Drew, who is a special

partner in the firm, from disposing of his prop-

erty, which, it is alleged, he is doing in order to

escape his liabilities in connection with the Can-

ada Southern Railroad bonds, which were said to

cause the failure of Kenyon Cox & Co.

The National Trust Company resumed busi-

ness to-day, paying its depositors in certified

checks on the Central National Bank, which is

their Clearing-House.

The bank of the Union Trust Company has

not yet begun to pay its depositors.

Judge Blatchford to-day modified the injunc-

tion sufficiently to permit Blake Bros. & Co. to

sell the securities held for money loaned to G.

Bird Grinnell & Co. This decision may throw

on the market 10,000 registered Lake Shore &

Michigan Southern sinking fund bonds.

The injunction was modified on condition that

Blake Bros. & Co. file a sworn statement of their

sales in the Clerk's office of the United States

District Court in bankruptcy, to await such ac-

tion as an Assignee in bankruptcy may take,

providing such Assignee be appointed to collect

and distribute the assets of Grinnell & Co.

Loading houses in the piano trade to-day deny

any intention of reducing wages. A few of the

smaller houses have ceased operations for a

short time owing to inability at present of mak-

ing collections.

THE WALL STREET FINANCIERS ON THE PRESI-

DENT'S VIEW OF THE PANIC.

Wall street bank officers ridicule President

Grant's views on the recent panic. Referring

to the latter's statement that silver is on a par

with currency, they deny it, and say there is a

difference of from two to four per

cent, and that so far as the

country being able to absorb between $200,000,-

000 and $300,000,000, it would probably use no

more than $40,000,000, the present amount

of fractional currency in circulation. Silver is

debased coin, and is not legal-tender for

more than $5, and when on a specie basis is re-

garded as something of a nuisance. They call

attention to the President's wishes for the re-

sumption of specie payment, and ask how he can

reconcile such a wish with the projected action

recommending the issue of the $44,000,000 reserve

which immediately starts the country upon a new

era of inflation. They characterize his scheme

for a Post-Office Bank as impracticable. While

he recommends the prohibition on the part of

National Banks of the payment of interest, he

proposes to establish a

POST-OFFICE BANK,

operated by the Government, which shall allow

4 per cent on deposits. The result of this would

be that 4 per cent would be the minimum rate

for interest. When capitalists had money which

they could not otherwise dispose of, they would

deposit it with the Government receiv-

ing 4 per cent, and when they could

loan it or could use it otherwise

they would draw it out. The same evil which

private bankers complain of would be felt by

the Government. At a time the deposits were

MOST NEEDED

they would be withdrawn. Again, the question

is asked, how the Government proposes to

secure 4 per cent interest. Does it propose to

go into a regular banking business? If so, an

era of

FRAUD, DEFALCATION, AND WILD-CAT OPERATIONS

generally will be the result. In addition to all

this, supposing that the bank was practicable,

it would be too great a centralization of power

in the hands of the Government; too great a

political instrument to be placed in its hands.