Click image to open full size in new tab

Article Text

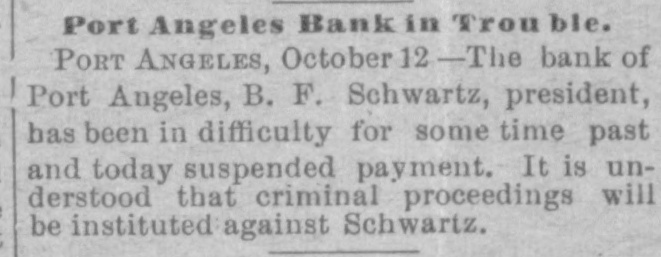

Port Angeles' Fugitive ExBanker in St. Louis Jail. THE SHERIFF GOES AFTER HIM. Rehearsal of His Misdeeds and How He Came to Be Captured. The Mogul Smallpox Sensation-Cellector Wasson's Statement-The Roslyn RobberSuspectBound Over-Colville River Overflows Its Banks PORT ANGELES, April 6.-(Special.) The bunko banker, Benjamin F Schwartz, formerly of this city, has been arrested in St. Louis, where he is now held in jail awaiting requisition papers. The POST INTELLIGENCER proved the medium through which the arrest was made. Some two weeks ago in correspondence sent from the Chicago bureau of the POST-INTELLIGENCER it was learned that Schwartz was in Chicago, dressed well, smoking cigars and was living at the Palmer house, Sheriff Morse at once began to investigate. Telegrams were sent to the Chicago chief of police, which gave as a reference the correspondent of the POST-INTELLI< GENCER. Schwartz was located in Chicago on April 17 through the POST-INTELLIGENCER, as stated. That day Chicago's chief of police telegraphed to Sheriff Morse for full information, so as to swear out a warrant, which was furnished. In the meantime Schwartz, from some source, was informed of impending arrest and suddenly skipped from Chicago, but he was later located in St. Louis, Mo. and there arrested yesterday by the chief of police of that city. Tomorrow Sheriff Morse will start for Olympia for the governor's warrant. being detained today owing to the burial of his father. In two weeks Schwartz will be returned to serve out his sentence. The public is fully informed regarding Schwartz and his operations in this city. He was by all odds the boldest swindler that has ever appeared in this city. Coming here with scarcely any money he at once began stupendous operations, organizing the First National bank as his first venture. In this his smooth tongue induced others to turnish the money and elect him as president. Fortified with this standing he began to speculate in real estate, street contracts, water and electric light franchises, until at an opportune hour the officers of the bank began to investigate, when it was found that for the good of the bank Schwartz should be retired. This was promptly done on April 14, 1891. Schwartz was then known to be entirely stranded, but he hustled around, borrowed a few dollars here and there, when he organized the Bank of Port Angeles with a "capital of $50,000. It was suspicioned that the "bank' was Schwartz and that Schwartz was the "bank.' He maintained, however, with much effrontery that be was backed by a syndicate of San Francisco and other California capitalists. Not many of the citizens of Port Angeles gave him their deposits, but enough was given so that he was enabled to make a pretense at business. He would loan money and when it became due would give receipts against the notes, pretending that the notes were lost. All the time he was either using them with other bankers as collateral or else had sold them. Thus his operations continued for fourteen months, up to October 8 last, when he was compelled to suspend business, being unable to meet the demands by checks. A superficial examination showed that his entire operations had been fraudulent and that there was no redeeming or mitigating circumstances that spoke in his behalf. He was arrested for embezzling trust funds the treasurer of the Western Washington Improvement Company, but owing to technicalities got clear. He was next arrested for the embezzlement of a note and mortgage, the property of M. W. Gay. He was arraigned, tried and convicted. He made a great fuss over this, saying that he was being persecuted, but the evidence was overwhelming, all, in fact, being in his own writing and representations, which he could not deny. Schwartz was sentenced to only eighteen months in the penitentiary, which was regarded as merciful and light. His attorney at once gave notice of appeal, but on the night of December 29 last he made his escape, the jailer claiming that Schwartz ran out of the door while he was putting a stick of wood in the stove. He ran in the darkness, and little e investigation showed that, at least on the outside, Schwartz had had confederates. Many theories were advanced, but the one mostly believed was that he had at once gone aboard a vessel bound for San Francisco or taken passage on a fishing schooner for Victoria, thence east on the Canadian Pacific, However this may be, the boldness of the convicted felon in going to Chicago, there mingling with his fellow-men in public places. is only another evidence of his utter carelessness. He believed that he was secure; that no such fate as the penitentiary would overtake him: that his crimes were but mistakes, which would be forgotten and overlooked as soon as he was away from his victims and the scenes of his bold operations. In this, as in all others, he is undeceived, and can but begin to realize that the "way of the transgressor is hard. CHICAGO, April -[Special. -The police department here had what the average Chicago detective would call a "picnic' trying to locate Ben Schwartz, of Port Angeles bank fame. Acting on the information published in the POST INTELLIGENCER, Sheriff Morse telegraphed on here and a fugitive warrant was taken out. Schwartz, however, had taken fright at meeting several Washingtonians and failed to show up at his old headquarters at the Palmer house as frequently as formerly. It was thought he had skipped to Omaha. Sheriff Morse was extremely desirous of capturing him, as his dispatch to the department here must have cost at least $30. This was, though, the fault of detective who wired that he had located Sehwartz, when, as a matter of fact, he had not. THE MOGUL SMALLPOX CASE.