Click image to open full size in new tab

Article Text

Bank of W. C. Become Deposits Percent Basis Negotiable on

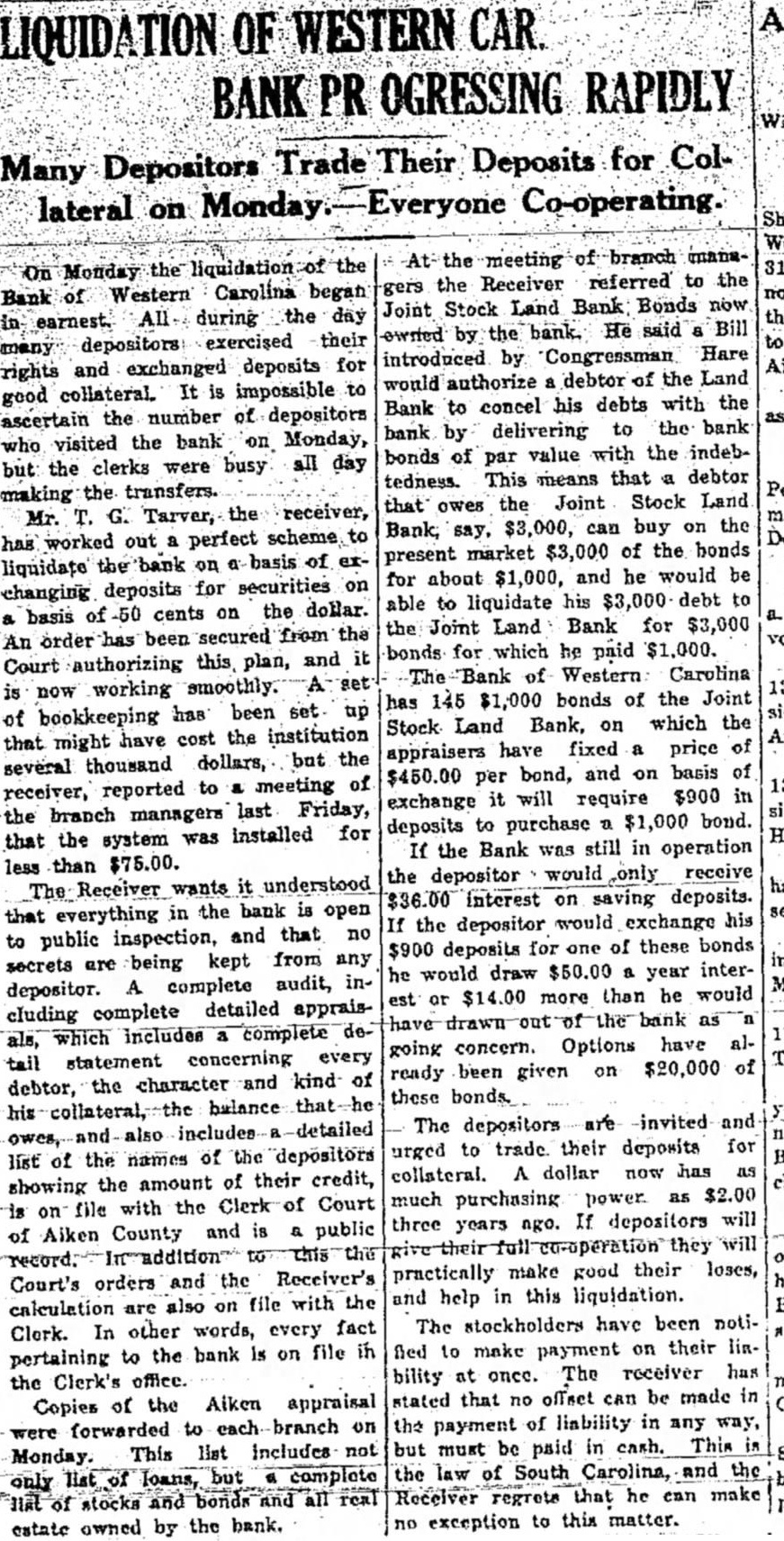

Appraisal of the assets of the Bank of Western Carolina completed last week and the value, as compared with the bank's liabilities, determined to be 50 percent, Judge E. C. Dennis at Barnwell, authorizes the bank's receiver, T. G. Tarver, to proceed with liquidation on this basis. The order of the Court specifically authorizes the receiver, as the first step efficient liquidation, to ac. the appraised value of each asset, plus interest to date of the transaction, on assets, or to exchange these assets with depositors or owners or assignees on Accordingly, the exchange of assets for deposits will become effective beginning Monday of next week, March 21, and as preliminary all agents of the bank, located at the several branches throughout the section formerly served by the Bank of Western Carolina, will meet in Aiken this (Friday) afternoon, at which time the plan will be thoroughly explained. Since the bank has among its assets a large number of amply secured loans on real estate and farm lands as well as on other securities and many notes secured by splendid endorsements, all or any of which are available to the depositor on the exchange plan, it is expected that there will be an immediate demand for these interest-bearing assets. Through the exchange plan, it is believed. the receiver will be enabled not only to progress more rapidly with liquidation, but under this plan the hardships usually incident to liquidation will be avoided. Instead of throwing the bank's assets on an unfavorable and depressed market and foreclosing mortgages and selling out the property of mortgagors for whatever it will bring, thus realizing only a small fraction of the value of the bank's assets for the depositors, transfers of assets will be made on the basis approved by the court. the effect of which will be that the bank's liabilities will be reduced in like ratio to its assets, depositors will receive in exchange for their now dormant deposits securities which will begin immediately to pay them from 7 to percent, forced sales will be avoided and. mortgagors given time to meet their obligations, a much larger return will be assured. Although of primray importance since it is the first step toward tual liquidation and because it makes possible a larger return from the bank's assets. the exchange plan however, only one phase of liquidation. Any and all of the bank's assets are subject to sale or exchange and any particular asset may be selected by the depositor for exchange. It is believed that a very large portion the assets will be absorbed through the exchange arrangement within short period of time. Any depositor may participate in the exchange and the $100.00 or smaller depositor will be given the same attention as the $10,000 depositor. Heretofore the manner of determining the value of the bank's assets and the basis of exchange has been plained. In making the final audit the greatest care and the best of judg- low: ment have been exercised. The audit and appraisal has represented a vast amount of detail work. In one column has been placed the total of the bank's assets appraised at valuation based not/upon what these assets, any particular piece of property or other asset, would forced sale this time; but at the intrinsic value. Men who know have been ployed to make the appraisal. Together with the assets, after allowing for all losses, depreciation, etc., has been included the liability of stockholders, accrued interest, estimated cost of liquidation, etc., over a period of two years. Against the total of assets thus determined is set up in another column the total of the bank's deposits, less secured and preferred claims, Thus determined that, for purposes of liquidation exchange, the basis should be 50 percent, or $1.00 of assets for $2.00 of deposits. The 50 percent basis is not arbitrary, however. This does not mean, for instance, that small depositors who do not exchange their deposits for securities will be limited to 50 percent in cash dividends. It is quite possible that in the long run they will receive a little more than 50 percent. perhaps 52 or 53 percent, possibly little more. But the depositor who exchanges his deposit for an note, mortgage or other security, will be getting a return on his money from the day he makes the exchange, and taking this interest return into consideration he will receive approximately 60 percent against the possible 52 or 53 percent which it is expected will be paid in cash dividends in units of ten percent from time to time during the expected period of liquidation. For example, depositor has $2,000 on deposit. This he exchanges for $1,000 mortgage paying 8 percent. Should he hold this mortgage for three years he will receive, in principal and interest. $1,316.40, or a fraction more than 65 percent on his deposit. On the other hand, should he retain his deposit and does not sell or exchange. leaving it to remain until the final dividend is paid, which will certainly take three years. assuming that he would get 60 percent on his $2.000 deposit. he would only receive $1,200 instead of $1,316.40 as mentioned above. and SO would be the loser in the long run. The advantage of trading deposits for assets thus becomes self-apparent. Every depositor. however, will receive the same uniform treatment and no favoritism will be practiced. In the first place. every depositor will have the same opportunity to select such assets as he or she may desire to cure in exchange for his or her deposit. Nothing will be forced upon any one. There are notes and mortgages. stocks and bonds. and the bank's holdings in real estate from which the selections of assets be may made. And those who do not. for any reason trade their dewill receive uniform dividends posits, as the becomes available money through collections and sales. There are. however. several important points bearing on the exchange arrangement with which the receiver desires the public to become familiar in advance that there will be no misunderstanding Some

The appraised value of assets has been approved by the court and in no is the receiver or his agents case mitted to accept less than this appraised value without an additional court order specifically applying to any particular asset. The appraised value is, therefore, not subject to bargaining and the ceiver or his agents will enter into bargaining of any assets. Direct offsets are to be allowed in accordance the law and the general custom of this state. All offsets have already been allowed ducted on the bank's books. These offmay mentioned, approximately $150,000 and all are direct offsets. Offsets claimed by endorsers not in accord with general practice which are in conflict with the general law of equity, the court's order specifically states, will not be allowed. There will be practically no offsets allowed to endorsers. The court order also provides that the receiver shall apply any dividends due endorsers to the liquidation, in part or in full, of any obligation owned by or owed to the bank on which the endorser is guarantor or surety The order also provides that the receiver shall not accept assignments of deposits owned by endorsers until the note or notes endorsed by them are paid or satisfactorily arranged. Every detail is now complete for putting the plan into operation on Monday of next week. The appraisals are mechanically fixed and not subject to negotiation. The nppraised values and the collateral supporting each and every paper are detailed. These appraisals are uniform at all branch banks. In addition. complete audit and recapitulation will be filed with the Clerk of Court for Aiken County as n permanent record. There is also on file with the Clerk of Court for each County and with each branch manager a list of the depositors giving the names and amounts of their deposits. This is public record. All transactions must he made at the local office or branch bank in which the obligation originated or in whose territory the secured proporty located. The home bank and all the branches will be prepared to deal directly with the depositors on the exchange basis beginning next Monday morning.

The order of the Court establishing the intrinsic value Bank of Western Carolina deposits at 50 cents the dollar makes these deposits, which have been lying dormant since the bank closed on October 15th. available for use by the depositor on a 50 percent basis. Deposits now become negotizble. and through the use of regular signment forms which have been prepared and which will be furnished by the bank in any quantity desired. the depositor is enabled to make such of his as he desire. money may In this issue of The Standard apa advertisement of pears composite number of Aiken merchants who will accept assigned déposits in change for merchandise or in ment of and other merchants will probably join in the plan as has inaugurated. The advantage of the of assignments is The himself owe the may owes him. The may assign any part of his deposit to the merchant, receiving therefor either merchandise or credit on a debt, for instance. His deposit in the closed bank becomes immediately available to him to supply himself with the necessities of life or his obligations. The merchant who the assignment in the course of trade is likewise enabled to apply the same on his indebtedness to the the bank, he may trade the assignment another merchant or he may purchase obligations from the bank. This is the practical application of the court's order.

While it should be remembered that the receiver and his agents are just as much interested in selling a $100 or smaller note as a Large note or mortgage, no one is compelled to ex. change. But there is advantage in the exchange plan in more than one way. For illustration, n person owes the bank $250.00. The bank holds his note for the same. He is unable at this time to pay the same and desires to pay it off at so much per month. In order to gain the time necessary to payment without embarrassment to himself. he may, if be so desires, arrange with friend or acquaintance to buy the note or exchange deposit for the same. In this case the bank would transfer the note to such a party. Either cash or deposits will be nccepted for assets. and a deposit nssignment on any branch in the chain is good on any other branch.

Gunter & Wilder have been retained as attorneys to represent the receiver in the collection of stockholder's liability, which will be called for immediately. The assessment of stockholders' liability has already been signed and an order of the court making this offective in expected to be received this week. J. B. Salley. it is understood. will represent the recever as general and associate counsel. Other attorney* will be employed in collections and foreclosures and other activities.

Within the past week new bank has been established at Barnwell, in the organization of which the receiver the Bank of Western Carolina has cooperated. To the new Bank of Barnwell the receiver has sold the building formerly occupied by the Barnwell branch of the Bank of Wes. Carolina and the new bank is now occupying this building The new bank begins life under the most favorable The receiver of the Bank of Carolina is working Laward the tablishment of other banks at additional points heretofore served by the Western Carolina chain. He has had long years of experience in handling rmall country banking and in spite of recent failures it is conviction that small banks can unquestionably be operated profitable basis. thought. in which many practical bank men that well-managed bank the must influence in the community. The function of a to first conserve with but to this money in gitimate for the of way and not the function of a invest in