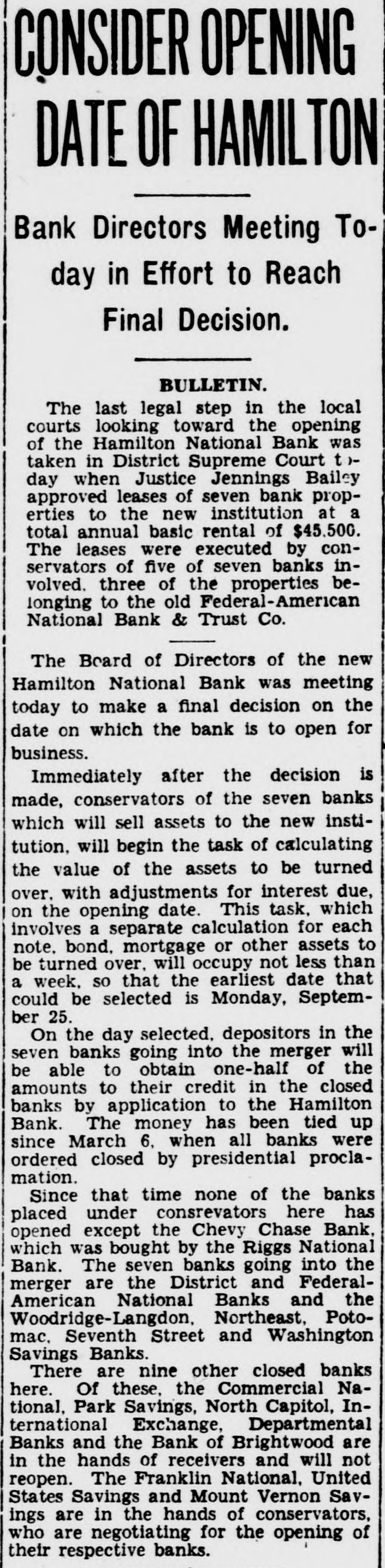

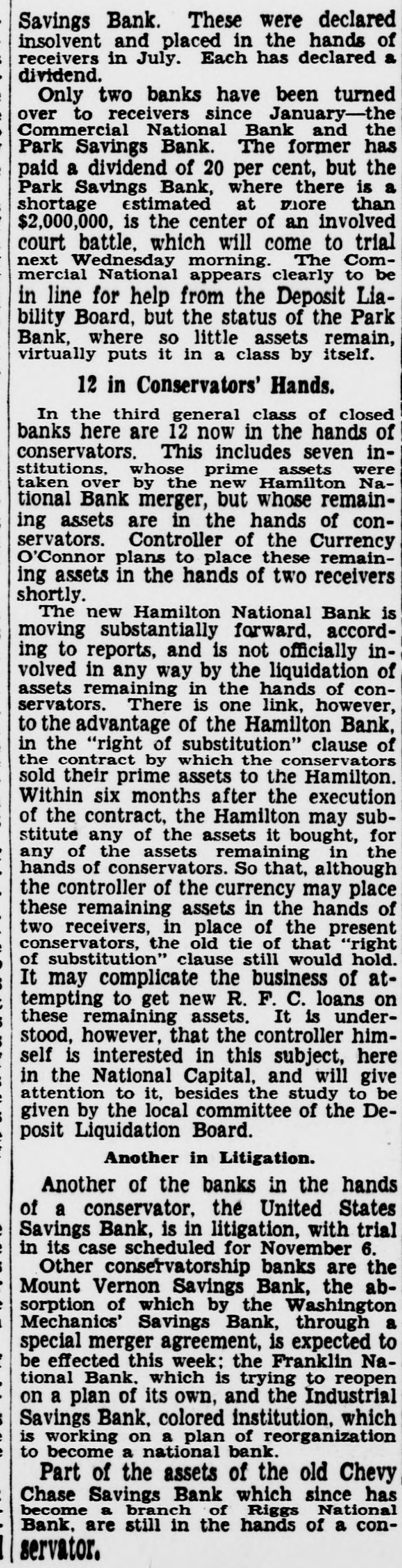

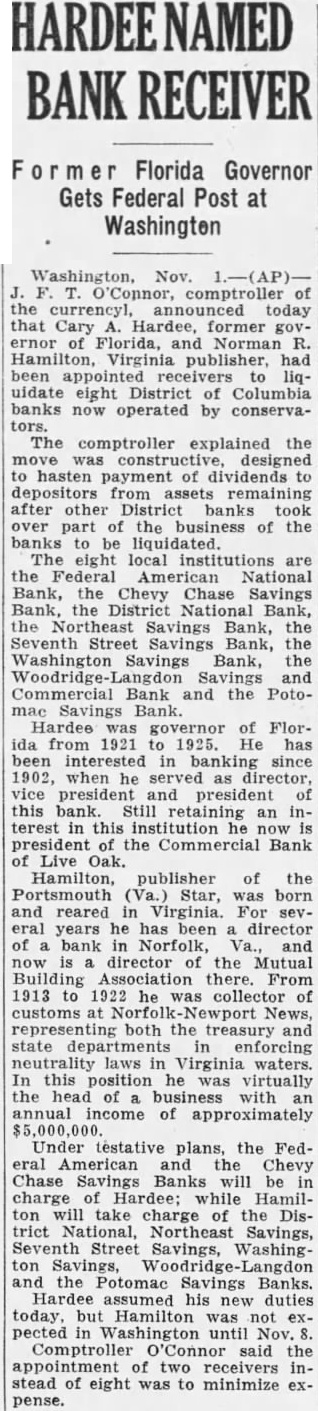

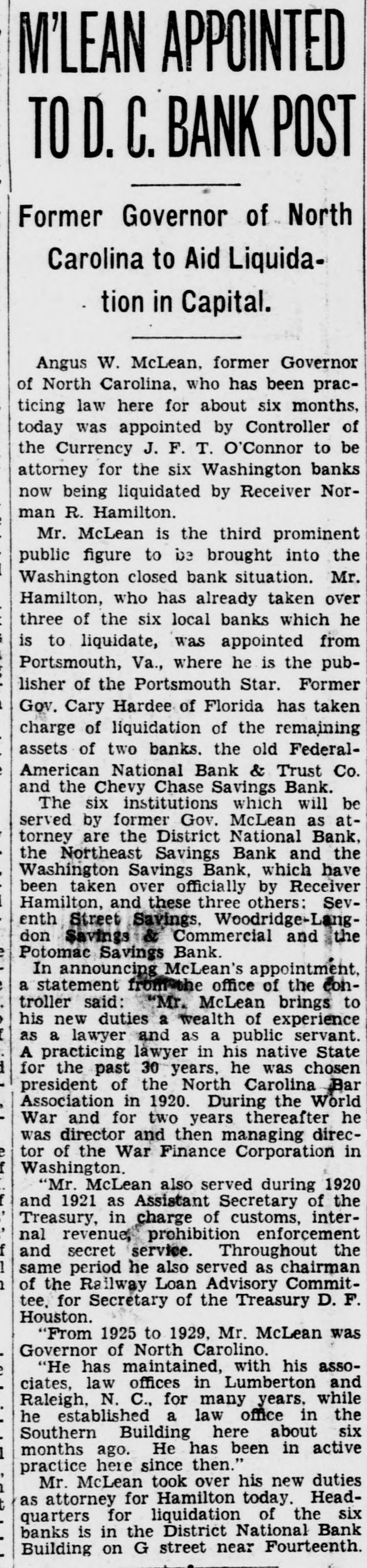

Article Text

LOCAL BANKS ACT TO PROTECT FUNDS District National Limits Withdrawals-Others Invoke 60Day Clause on Savings. The District National Bank opened today on a 5 per cent withdrawal basis, following action taken by the directors early this morning, for the protection of depositors. President Joshua Evans, jr., announced. (The following notice was addressed today to the depositors in the bank: "Owing to heavy withdrawals of deposits during the last few days, and in order to safeguard all of our depositors, the board of directors has passed a resolution allowing depositors to withdraw 5 per cent of their balances in this bank at the close of business February 28, 1933, until further notice. All new deposits and new accounts opened March 1, 1933, and thereafter are subject to 100 per cent withdrawal at any time after actual realization cf funds by the bank." 60-Day Clause Invoked. The officials stressed the fact that all deposits made today and after this date can be withdrawn in full at any time. It was announced in the financial district that most of the local building and loan associations have invoked their time clauses on withdrawals, limiting the amount to $100. For larger amounts notice must be given in advance. Officials said the rule would be in force for the present. Several savings banks here invoked the 60-day clause on withdrawal of savings accounts. Some of these banks permit the withdrawal of 10 per cent up to $100. Above that amount, the 60day or two-month notice, is being required. Protective Measure. Among the local banks which have adopted this rule-the same plan which has been adopted extensively in other cities-are: United States Savings Bank, Chevy Chase Savings Bank, Security Savings & Commercial Bank, Park Savings Bank, Seventh Street Savings Bank, Washington Savings Bank, Anacostia Bank, Mount Vernon Savings Bank and the Northeast Savings Bank. (In an earlier edition of The Star the name of the Washington Mechanics' Savings Bank was included with those involking the 60-day clause. This was incorrect.) Officials said the action was taken merely as a protective measure, both for the banks and for the depósitors. The Commercial National Bank. which closed yesterday, has been placed in the hands of Robert C. Baldwin, a receiver of the office of the controller of the currency. Mr. Baldwin has taken over the receivership from J. L. Bailey, who took charge when the bank was closed. It was explained that Mr. Bailey will remain for a while in his capacity as a national Bank examiner to assist Mr. Baldwin. Has Considerable Experience. In the meantime, it was said at the Treasury Department, the new receiver probably will use a large part of the staff of the bank for his work. The new receiver. before Joining the office of the Controller of th è Currency, had considerable liquidating experience. Under the auspices of the Government he has been receiver for e bank at Lynn, Mass., since the latter part of 1931, and has been directing its liquidation. An official of the Treasury said in regard to Mr. Baldwin: "By reason of his ability in liquidating that bank, the Treasury Department saw fit to transfer him to the Commercial National Bank. We have every confidence that he will administer the affairs of the institution in a manner satisfactory to all concerned."