Click image to open full size in new tab

Article Text

Deposits Insured-Bankers Howl

The News presents herewith an anylysis of the guarantee of bank deposits by the United States Government. By LOWELL LIMPUS. (Copyright 1934 by News Syndicate Co., Inc.) YOU deposit $2,500 (if you're lucky enough to have it) in your bank. The teller makes out a deposit slip. A bearded old gent, in a starspangled suit, leans across his shoulder and scrawls across the face of the deposit slip: "IF THIS BANK DOESN'T GIVE YOU BACK THIS MONEY, UNCLE SAM." And that's Federal Deposit Insurance. Of course, Uncle Sam doesn't really endorse your deposit slip. But he stands behind it. In the guise of the Federal Deposit Insurance Corporation (better known in these alphabetical days as the FDIC). That is to say, he does if your bank is one of the 13,832 out of 15,023 in the country that have signed up with him. Neither does he guarantee all of your money out of his own pocket. He pays part of it; the Federal Reserve System pays some more and the other banks the rest. But you get it all-up to $2,500. How does it work out? Well, it has worked fine so far for the depositors in the two small insured banks that have gone broke since the new system went into effect on Jan. 1, 1934. Each depositor got back his money up to the $2,500 guaranteed by Uncle Sam. The first person to benefit under the system was Mrs. Lydia Lobsiger of East Peoria, Ill. Mrs. Lobsiger, a widow, had $1,250-all the money she had in the world-in the Fond du Lac State Bank of East Peoria. It went broke and was closed by State authorities. On July 3 the FDIC handed her a check for $1,250.

Depositors Recover Total of $125,000.

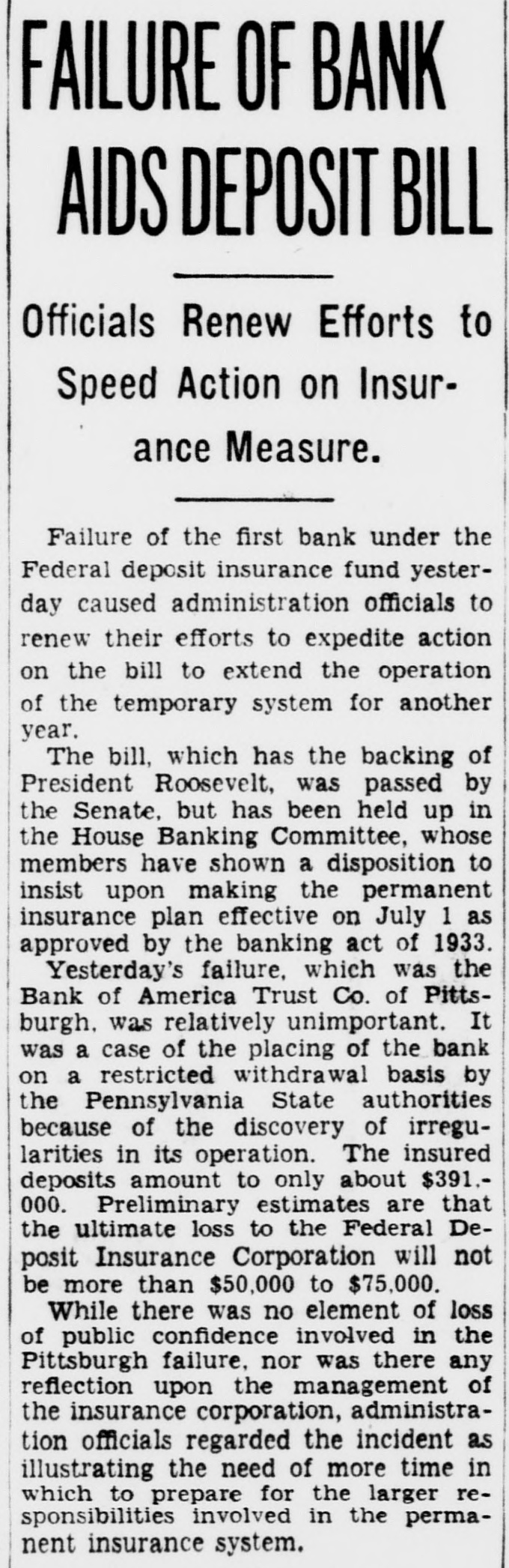

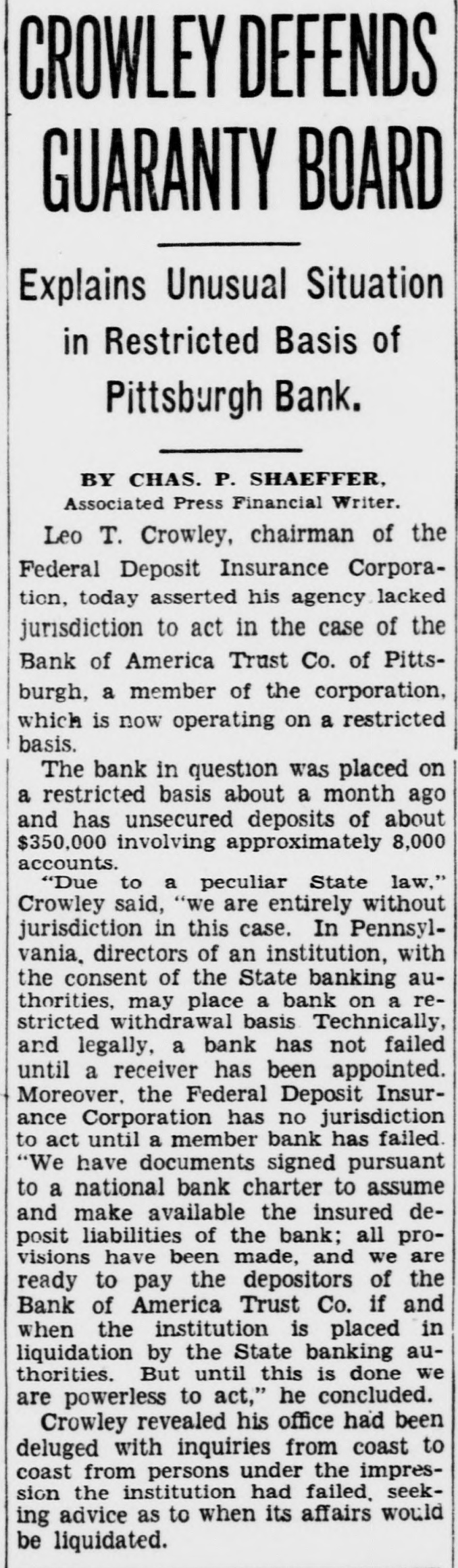

Each of the 1,789 depositors got up to the $2,500 limit, the total paid out being estimated at $125,000 out of the $241,412.84 on deposit. Payments to depositors in the Bank of America Trust Company of Pittsburg h, P a., began on July 19. It was closed by the State authorities on April 21, but C. B. Axford pay m was held up pending efforts to reorganize it. It contained $391,000 in insured deposits. That's how FDIC works. But where does the money come from? It comes out of the coffers of FDIC, which contained $147,437,983.51 in cash on Feb. 28, the date of the last report. The corporation also owned $108,776,073.38 worth of securities. These coffers were well filled from three principal sources. Uncle Sam tossed in $150,000,-

$000 from the Federal Treasury. The Federal Reserve Banks paid in $69,649,778.48 for capital stock in the corporation. The banks which joined the system paid in assessments, for the privilege of joining, $38,837,795.11. The rest came from interest on the money. The money paid out came from this common fund. FDIC will be repaid whatever percentage of the deposits the bank is able to make good. The experts figured that the FDIC had about $329,000,000 on hand July 1, and that the greatest possible loss on the first failure could not exceed 4-100ths of one per cent. It should be noted that all these statements refer to the Temporary Deposit Insurance Fund, which is quite different from the permanent fund. The permanent system, after being postponed twice al-

There was so much opposition toya the permanent plan-and its organization is so complicated-that it was delayed, while the temporary scheme was installed in order to quiet down a lot of yelping Congressmen. It is supposed to serve until the permanent plan is ready. Both plans grew out of President Roosevelt's brisk remedy for the conditions which resulted in the bank closing of 1933, from which conditions seventeen of the biggest banks in the country never recovered sufficiently to reopen. Both are included in the "Banking Act of 1933," which laid down the terms on which the banks could continue to operate. Deposit insurance was written into that law. The temporary plan called for Uncle Sam to contribute $150,000,-

"kitty" will be created to? new pay for losses. Whatever remains in the temporary fund coffers will be prorated and given back to the contributors.

New Plan Brings Howl From Bankers.

This new "kitty" is the reason for loud sqúawks from most bankers. Uncle Sam tosses in another $150,000,000 and the Federal Reserve banks are nicked to the tune of $140,000,000 for stock. They have to pay half of it at once and the balance on ninety days' notice. The rest comes from the member banks. They have to pay one-half of one per cent. of their total deposits for stock which will draw dividends, if any. They pay half their subscription in cash and the rest ready, is now scheduled to go into effect Jan. 1, 1935-unless the bankers succeed in hamstringing it. They don't like it at all. The temporary system-which is admittedly a sort of makeshift afjair, became effective Jan. 1, 1934.

000; the twelve Federal Reserve Banks to subscribe for $132,299,556.50 worth of stock in the corporation created and for all banks joining the system to pay an assessment of one per cent. of the amount of their deposit eligible for insurance (below the $2,500 limit per depositor). They had to pay one-half their assessment on joining and hold the other half available at the call of the directors of the corporation. The latter gentlemen were J. F. T. O'Connor, Controller of the Currency, and Walter J. Cummings and E. G, Bennett, appointed by the President. Since Chairman Cummings resigned on Feb. 1, his place was filled by Leo T. Crowley, who became chairman. Member banks were liable to another one-half of one per cent. assessment, if more funds were required, but the temporary plan was supposed to end July 1, 1934. It was prolonged because the permanent system wasn't yet ready. The permanent plan insures deposits up to the first $10,000, after which it guarantees threefourths of the next $40,000 and half of the remainder of each deposit. When it goes into effect must be planked down when asked for. But-and here is where the rub comes in-they are liable to assessments of one-fourth of one per cent. of their total deposits each time the directors call for more money. And the directors have to call for more money whenever the total amount paid out to depositors in broken banks amounts to as much as one-fourth of one per cent. of the total mount of deposits insured in all banks belonging to the system. There's the bogey man that has a lot of our best bankers wriggling on the anxious seat. They're afraid that, if a lot of weak banks fail, the strong ones will have to be pouring cash into the deposit fund like water into a bottomless pit. They see visions of one yelp after another for more cash. They don't like the prospect a little bit. (Of course, it looks like manna from heaven to the banker who isn't certain his bank is in a sound position.) Furthermore, there is an additional provision which gives bank stockholders heart failure. "No insured bank can pay any dividends until all assessments levied upon it by the insurance corporation are paid in full." That gives FDIC a first mortgage on every bank stock owner's dividend coupons. It brings a wail from them that resounds to high heaven.

Most Bankers Favor Temporary Scheme.

How do the bankers like the temporary scheme? Most of them are for it, according to Clinton B. Axford, editor of the American Banker. His opinion is supported by bankers interviewed. Everybody admits the poor depositor is entitled to reasonable protection. But even so, the savings banks don't "go for" it. Only sixty-six out of 567 in the country still be. long, 188 of them having withdrawn on July 1. The withdrawals included all but two of New York City's savings banks; only the Emigrant Industrial and the Franklin remaining in the system.

And out in Kansas, which had a very sad experience with State insurance of deposits, the commercial banks don't seem to like it. Only 299 joined the system and 323 stayed out. The uninsured banks, which have formed an organization to fight the scheme, report their deposits increasing just as rapidly as the member banks, The rest of the country seems to be for it, however. And how do the bankers like the permanent plan? They don't. Emphatically, they don't. They foresee dire things from it. This is especially true of the leaders. The case was summarized by Axford, who declared: "The ultimate result will be that we will face a choice between closing up most of the banks in the country and liquidating them or else adopting wild inflation to pay off."

Cite State Insurance Projects Which Failed,

The banking Cassandras point with horror to the State insurance experience of Kansas, Nebraska and other midwestern States, which adopted the Bryanesque philosophy. Kansas, they say, tried it twenty-five years ago and signed up 900 banks. The losses of the early 1920's caused assessment after assessment and bank after bank failed. Finally, when the system had piled up a $6,000,000 deficite, the law was repealed. Nebraska adopted it in 1909, after Oklahoma had blazed the trail, and 1,008 banks joined up. The system collapsed in 1929, when 106 banks failed for $30,000,000. It was repealed in 1930, after fifty more went broke. The experiment cost the good banks $17,700,000 and depositors lost $22,000,000 in unpaid deposits and interest, according to the American Banker. The same experience was repeated in half a dozen other States, with losses running up to $40,000,000. Among the most defiant opponents of the scheme is President J. M. Nichols of the First National Bank of Englewood, Ill., a suburb of Chicago. He not only refused to pay the assessment levied against his bank as a member of the Federal Reserve system, but has openly invited the authorities to sue him for it. He is the acknowledged spokesman of the opposition. In a statement to The News, Nichols said: "For the sound bank to guarantee the losses of the unsound is merely 'robbing Peter to pay Paul' and should be termed anything but insurance, It is as though an arm stunt flyer were to pay the same premium on an accident policy as does a bookkeeper in an old people's home. Summarizing his position, Nichols declared that "were it put to a test through another general withdrawal, the FDIC would be S ept away like a feather in a windstorm."

Nichols' Stand Makes Him Bankers' Hero.

As a result of his defiance of the FDIC. Nichols is a national hero among bankers today. He is being played up by various banking publications and his tart exchanges with Crowley are gleefully quoted. Nichols proudly announces that his bank is 103.7 per cent. liquid and issues statements showing that he has $6,765,000.65 available to pay off $6,520,190.05 in deposits. Deposit insurance? The depositors like it. The bankers don't.