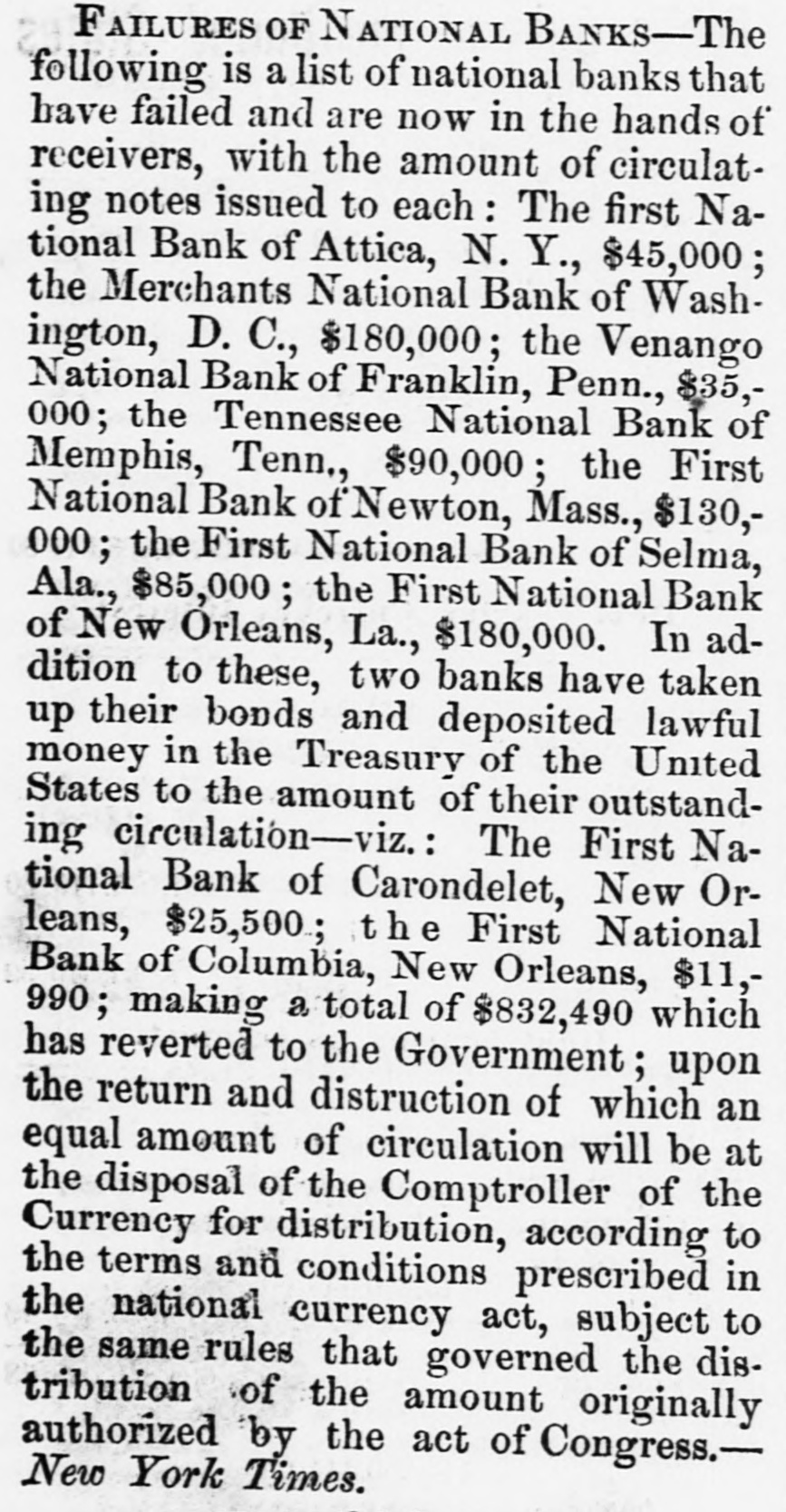

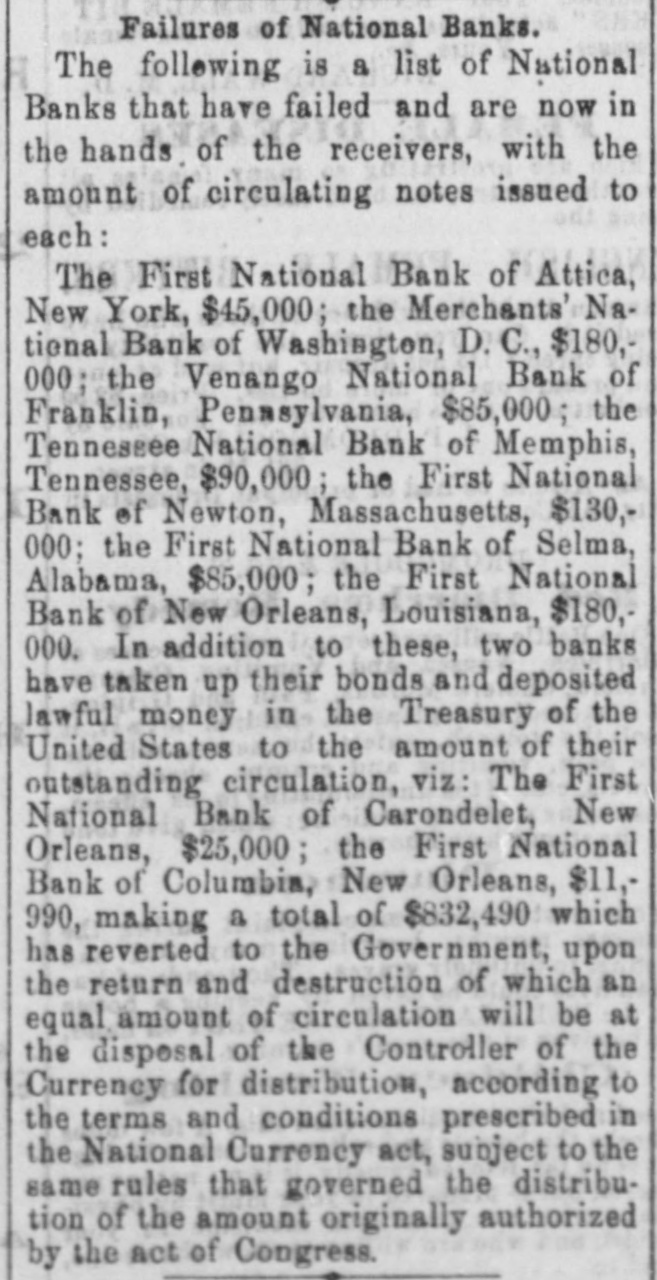

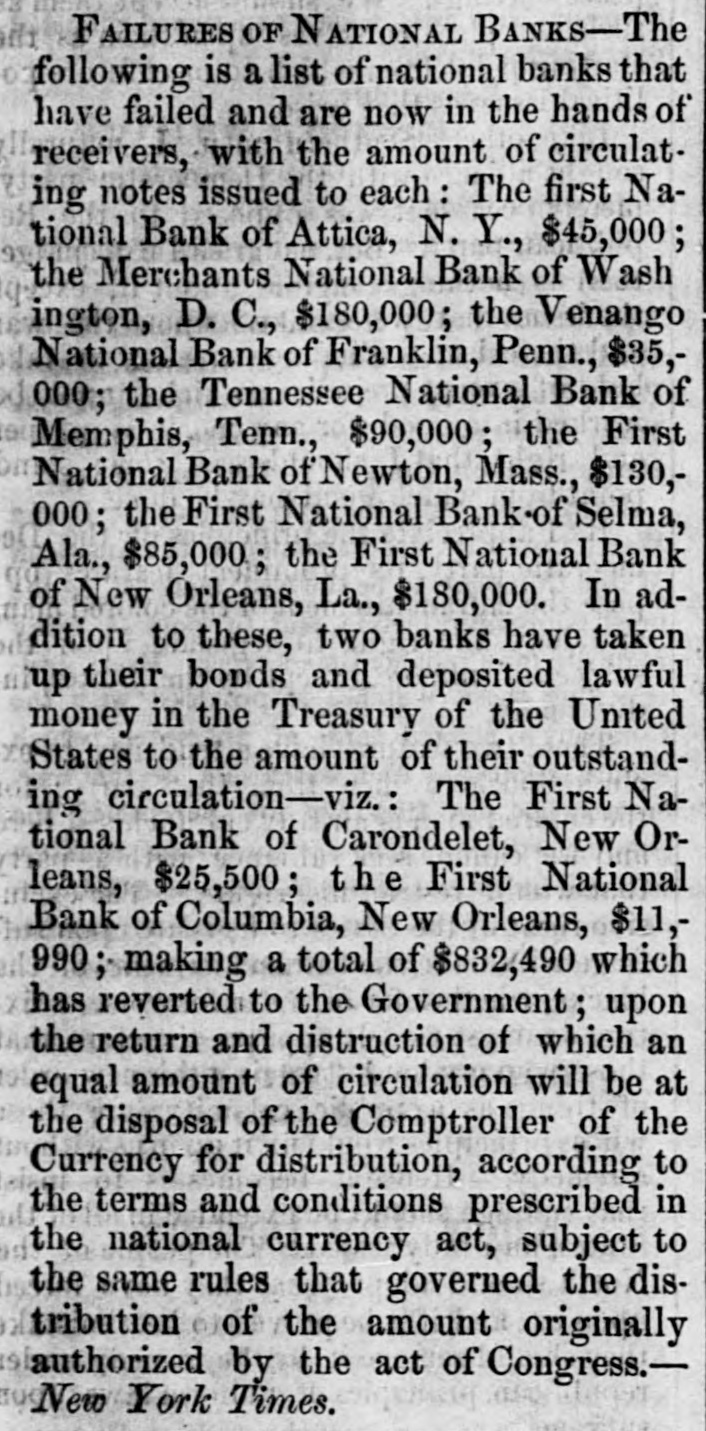

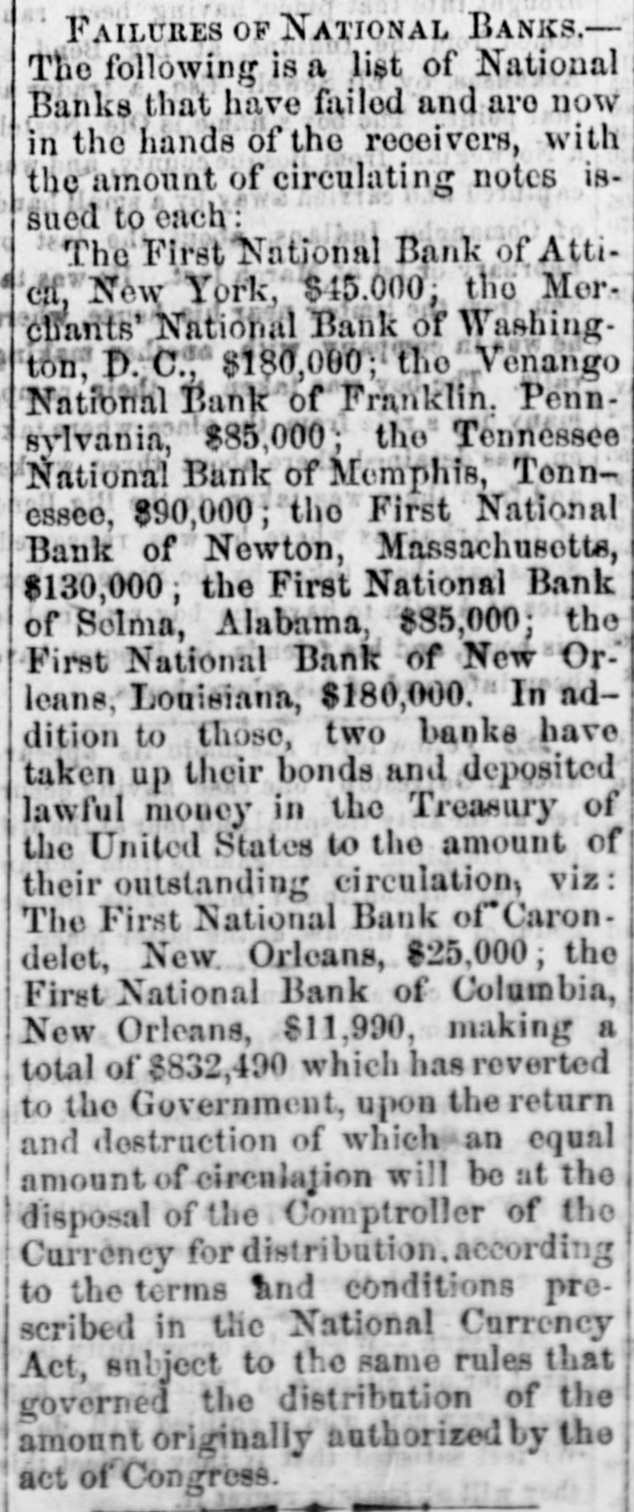

Click image to open full size in new tab

Article Text

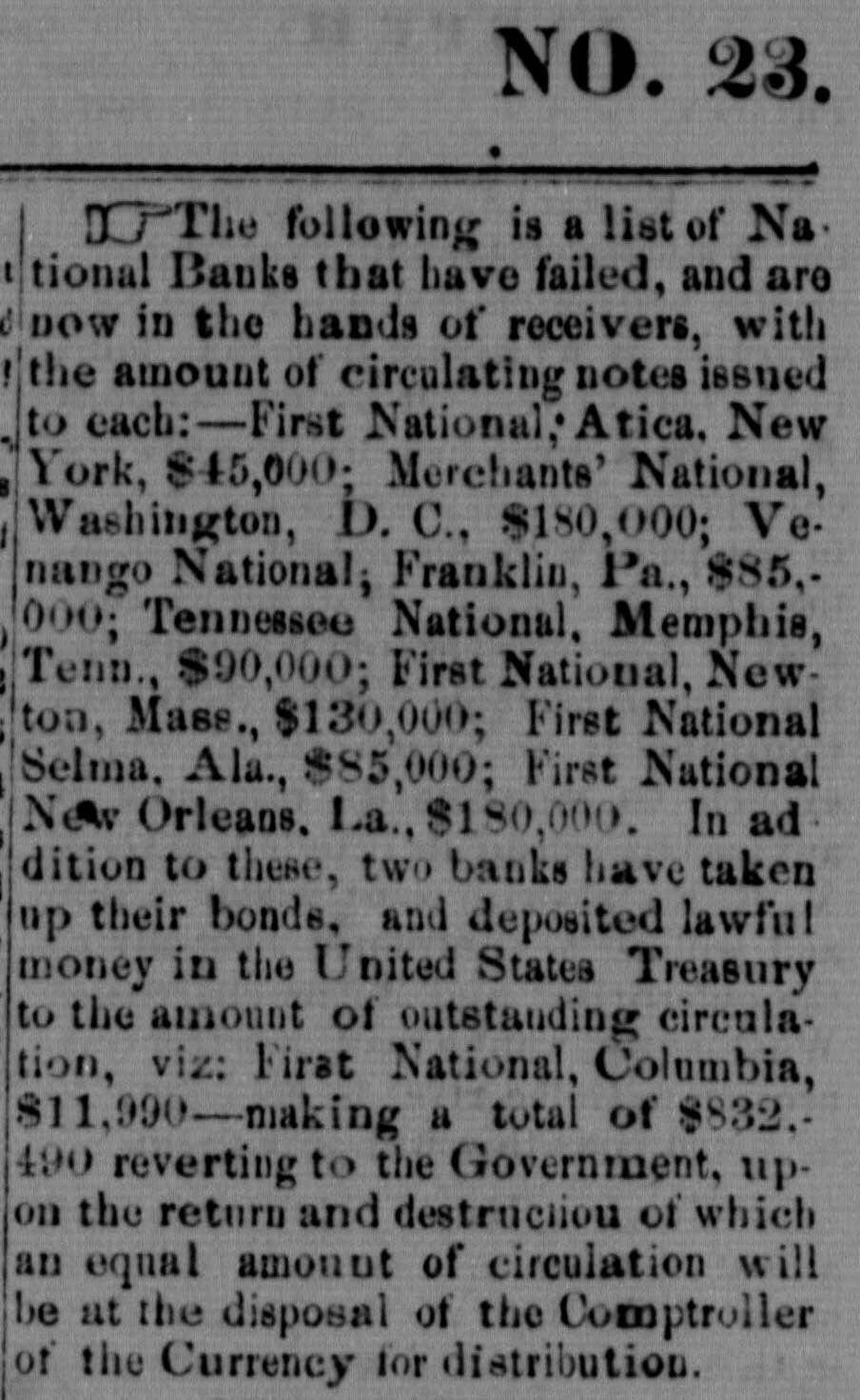

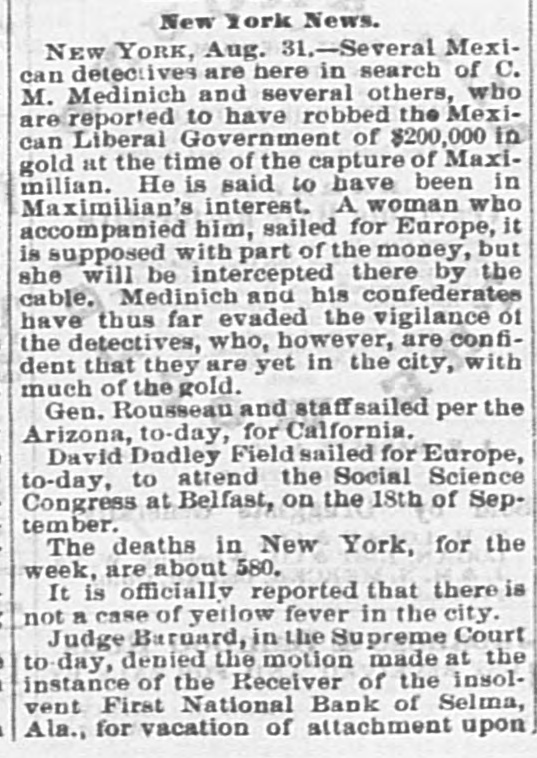

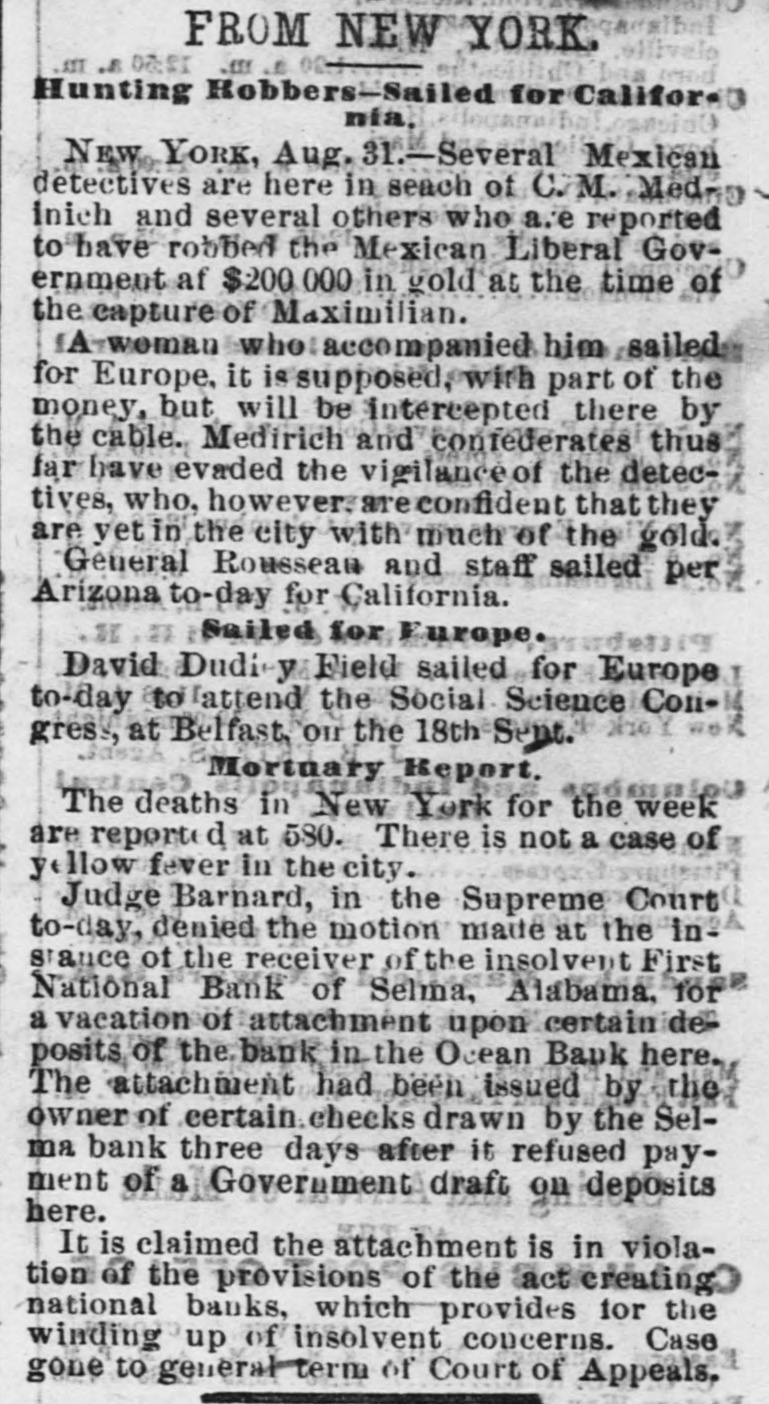

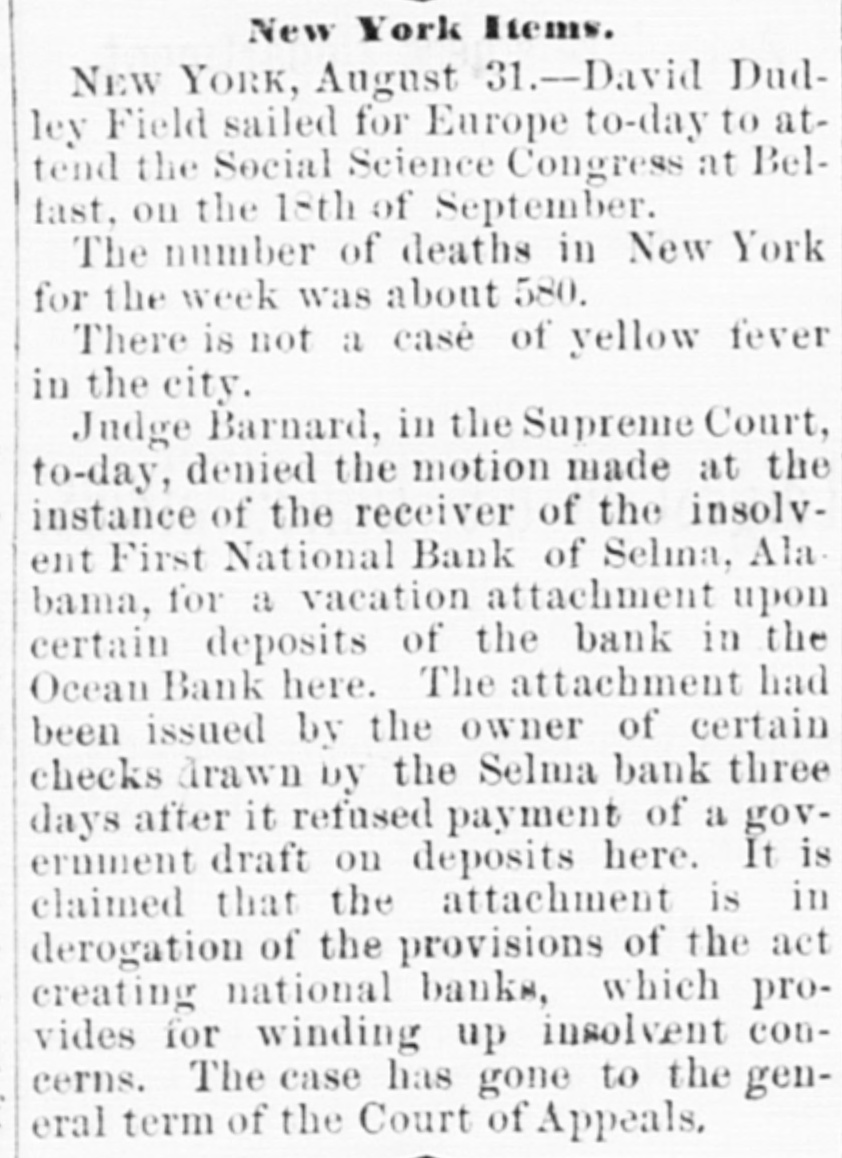

curity, or as collateral security, for any loan of money, or for a consideration shall agreeAto withhold the same from use, or shall offer or receive the custod or promise of custody of such notes as security, or as collateral security or consideration, for any lloan of money." 5th of April last the Controller was advised that bank On the in the City of New-York, with a capital of $1,000,000, a and whose average exchanges at the Clearinghouse did not exceed $300,000, was that morning creditor at the Clearing-house for $4,770,000. A8 it was evident that this large credit was not the result of legitimate business, the examiner was directed to make an exam ination of the bank, which was immediately done, 114 connection with a member of the Clearing-house committee. From the examination, which was thoroughly and carefully conducted, it appeared that deposits had been made in that bank, by one individual, upon the morning of April 5 to the amount of $4,100,000, the whole of which was drawn out upon the same day, upon the checks of the depositor, in legal-tender notes. The president of the bank denied that the bank had any interest in these trans actions, and there was no evidence of any loan, or of ad. vances in any shape. upon these deposits. These traus actions were the subject, subsequently, of an investiga tion by the Bank Committee of the House of Represent tarives, and, although it was clear that the spirit of the law had been violated, no evidence could be obtained to warrant the commencement of a suit for the recovery of the penalty prescribed in the act referred to. The in vestigation undoubtedly had the effect to prevent the repetition of similar transactions; no offenses of this been kind, on the part of any national bank, having since brought to the attention of the Controller. The New-York Clearing house Association subse quently passed a resolution declaring "that the Clearinghouse Committee be and is hereby directed, whenever it appears, in its judgment, that legal-tender notes have been withdrawn from use through the agency of any bank, members of the association, to make an immediate examination of the bank in question, and should there appear to be complicity on the part of the bank or its officials, to suspend said bank from the Clearing house until action of the association shall be taken there on." The withdrawal of currency for illegitimate purposes has, however, since been accomplished without the assistance of the banks. The rigid enforcement of the resolution of the Clearing-house will prevent complicity on the part of banks in such transactions; and it the New-York Stock Board and the leading banking houses will unite with the Clearing-house, and refuse to transact business with unserupulous men. who do not hesitate to embarrass legitimate business for the parpose of increasing or diminishing the values of stocks or bonds in which they are temporarily interested, they can do more to prevent such operations team any Congress enactment. INSOLVENT BANKS. Twenty-one national banks, organized in 11 different States, with an aggregate capital of $1,236,100, have failed since the organization of the system in 1863 The total circulation of these banks was $2,942,793. of which $2,441,430 has been redeemed in full, leaving a belance still outstanding of $501,363, which will also be redeemed, upon presentation to the Treasurer of the United States, from the avails of United States bonds held as security for that purpose. Of these banks, five have been finally closed (two during the past year), baying paid dividends to their ereditors. Six national banks have fatted during the past year. New-York: Of these, the Union Square National Bank, the Fourth National Bank, Philadelphia, and the Waverley National Bank, New-York, have paid their creditors in full-a settlement, it is believed, without a precedent prior to the establishment of the national system. The Eighth National Bank, New-York, has paid dividend of 50 per cent; the Ocean National Bank, New-York, a dividend of 70 per cent; and the receiver of the Ocean National Bank, and of the First National Bank of Fort Smith, Ark., estimate that the creditors of both these banks will últimately receive a dividend of 100 cents on the dollar. The Venango National Bank of Franklin, Penn.: the Merchants' National Bank of Washington. D. C. the First National Bank of Selma, Ala., and the First National Bank of New-Orleans, were United States depositories. e-final dividend in favor of the creditors of the First National Bank of Vicksburg has been unexpectedly delayed by the recent presentation of a claim of the United States for money alleged to have been illegally deposited by the Collector of Internal Revenue of that district, in the year 1868. Since that time no lesses have occurred to the Government by deposits made in the national banks, although many millions of dollars have been continually on deposit with banks which are designated as depositories. The three a first-named banks, at the time of their failure, had large amount of Government funds on deposit. SURPLUS AND SPECIE-EXTENDING THE LIMIT OF SURPLUS. The law requires that every national bank shall carry one-tenth part of its profits to surplus-fund account before the declaration of a dividend, until the same shall amount to 20 per cent of its capital stock. This wise provision has been generally observed. and the returns show that the banks now have a surplus of more than $100,000,000, and considerably more than onefifth of their capital in surplus account. The act also limits the liabilities of any association, person, com pany, or corporation, for money borrowed, to one-tenth of the capital stock paid in. The Controller recommends that this limit be extended to one-tenth of the capital and surplu. which will have a tendency to 10. crease the surplus fund beyond the limit required by the law. The following table will exhibit the aggregate amount of specie held by the national banks at the dates mentioned, the coin, coin certificates, and checks payable coin held by the national banks of the City of New York being stated separately. The country banks have not heretofore separated coin in their reports: -Held NationalsBanks in New- City.-