Article Text

t Receiver for National Bank. L Washington, Feb. 11.-A federal re: ceiver was appointed today for the ) American exchange National bank at Syracuse, N. Y.

81f97390057437d2None

Click image to open full size in new tab

t Receiver for National Bank. L Washington, Feb. 11.-A federal re: ceiver was appointed today for the ) American exchange National bank at Syracuse, N. Y.

Click image to open full size in new tab

From Washington. [Correspondence of the Alexandria Gazette.] Washington, Feb. 11. A delegation of Virginians, headed by General Fitzhugh Lee and including Mr. Park Agnew, of Alexandria, yesterday invited the President to attend on May 13 next the celebration of the two hundred and ninety-seventh anniversary of the first landing of the English at Jamestown. The President said that he would take the invitation under consideration and gave the committee assurances that he felt a deep interest in the exposition to be held to commemorate the settlement. Senators Martin and Daniel and some of the members of the House from Virginia accompanied the delegation of officials of the proposed Jamestown exposition. The Comptroller of the Currency has been advised by National Bank Examiner J. Van Vranken that the directors of the American Exchange National Bank of Syracuse, N. Y., voted last night to close its doors and that it has not been opened for business this morning. The comptroller has appointed Examiner Van Vranken as receiver. The comptroller is not in possession of any information as to the immediate cause of the failure. The resources and liabilities of the bank at the time of the last statement, January 22, were $906,039.08 each. The State Department is officially informed that a revolution is immenent in Honduras. Martial law has been proclaimed and a number of arrests made. One of the vessels of the Pacific Squadron will probably be sent to that country to watch affairs. The Navy Appropriation bill, which was reported to the House today carries an appropriation of $96,328,038. The cost of constructing the ships recommended is estimated as follows: One first class battleship of 16,000 tons, $7,775,000. Two first class armored cruisers, 14,500, tons, $6,505,000 each ; three scout cruisers, 3,750 tons, $2,200,000 each ; two colliers, $1,250,000 each. The Navy Department announces that it is about to send 600 additional marines to the Philippines. They will leave in two weeks.

Click image to open full size in new tab

BANK CLOSED. American National of Syracuse in Receivers Hands. Syracuse, N. Y., Feb. 11.-The American National Exchange bank of this city was closed today by National Bank Examiner Josiah Van Vankin. No statement of the bank's condition has been given out. /

Click image to open full size in new tab

TOLD IN A LINE New York-Four persons were killed in a fire which destroyed the Brooklyn Chair company's factory. New York-An alarm of fire nearly precipitated a panic in the Metropolitan opera-house last night. York, Pa.-Back water from the ice gorge near New Holland has caused the greatest flood ever known at York Haven. Syracuse, N. Y.-The American Exchange National bank of this city was closed to-day by National Bank Examiner Josiah Van Vranken. Chicago-The Press club was tendered a banquet last night, tables being laid in one of the great tunnels of the Illinois Tunnel company. Salt Lake City-The Zion founded by Brigham Young is to be invaded next August by & great host from the Zion established by John Alexander Dowie. San Francisco-W. W. Copeland, president of San Francisco Typographical union, is dead as the result of falling thru an open elevator shaft. He was connected with Iowa newpsapers twenty years ago. New York-War in the far east has affected the silk piece goods market of the United States. Prominent importing houses have just announced advances of 10 per cent on Habutal and other silk fabrics manufactured in Japan.

Click image to open full size in new tab

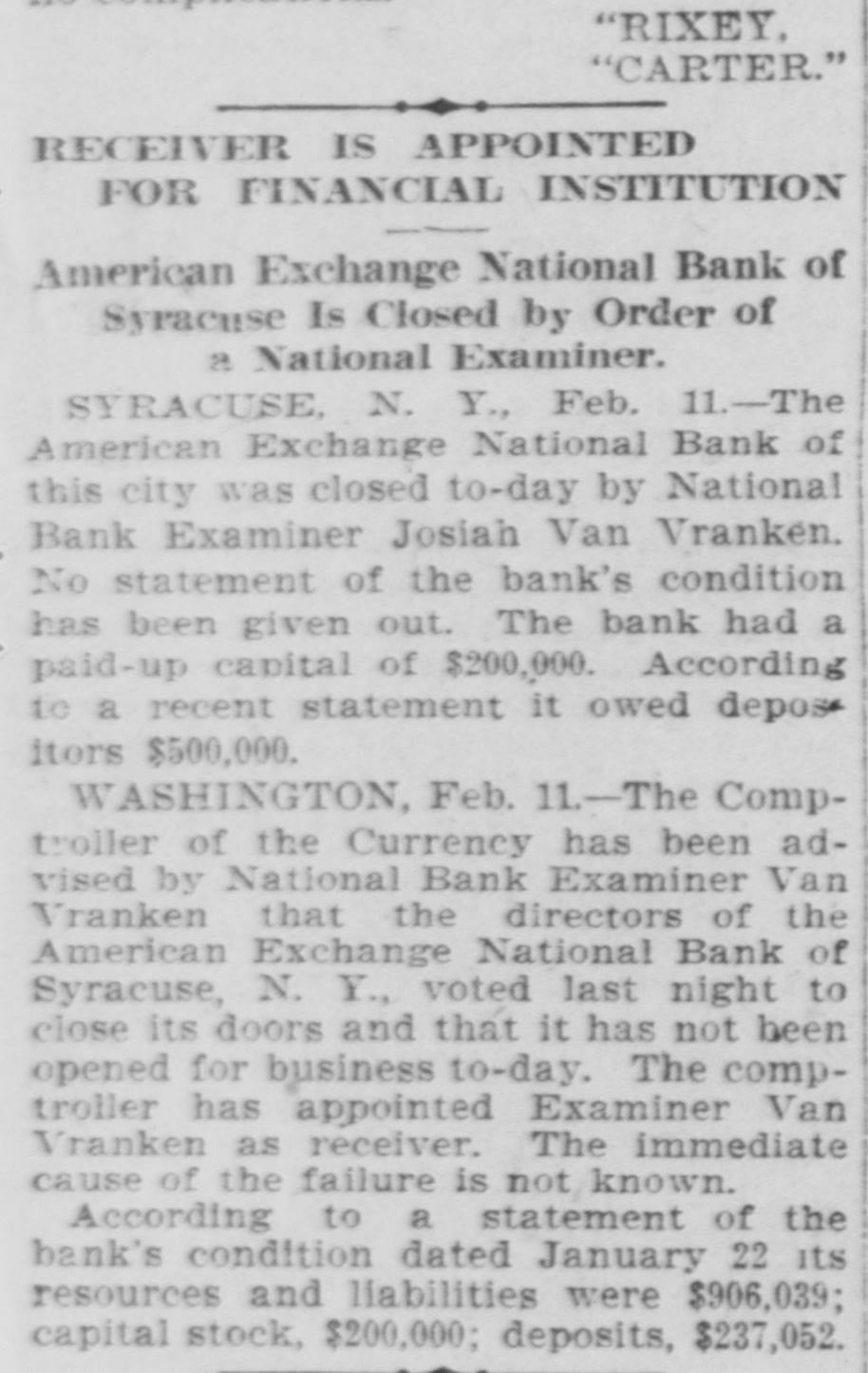

"RIXEY, "CARTER." RECEIVER IS APPOINTED FOR FINANCIAL INSTITUTION American Exchange National Bank of Syracuse Is Closed by Order of a National Examiner. SYRACUSE, N. Y., Feb. 11.-The American Exchange National Bank of this city was closed to-day by National Bank Examiner Josiah Van Vranken. No statement of the bank's condition has been given out. The bank had a paid-up capital of $200,000. According to a recent statement it owed deposit itors $500,000. WASHINGTON, Feb. 11.-The Comptroller of the Currency has been advised by National Bank Examiner Van Vranken that the directors of the American Exchange National Bank of Syracuse, N. Y., voted last night to close its doors and that it has not been opened for business to-day. The comptroller has appointed Examiner Van Vranken as receiver. The immediate cause of the failure is not known. According to a statement of the bank's condition dated January 22 its resources and liabilities were $906,039; capital stock, $200,000; deposits, $237,052.

Click image to open full size in new tab

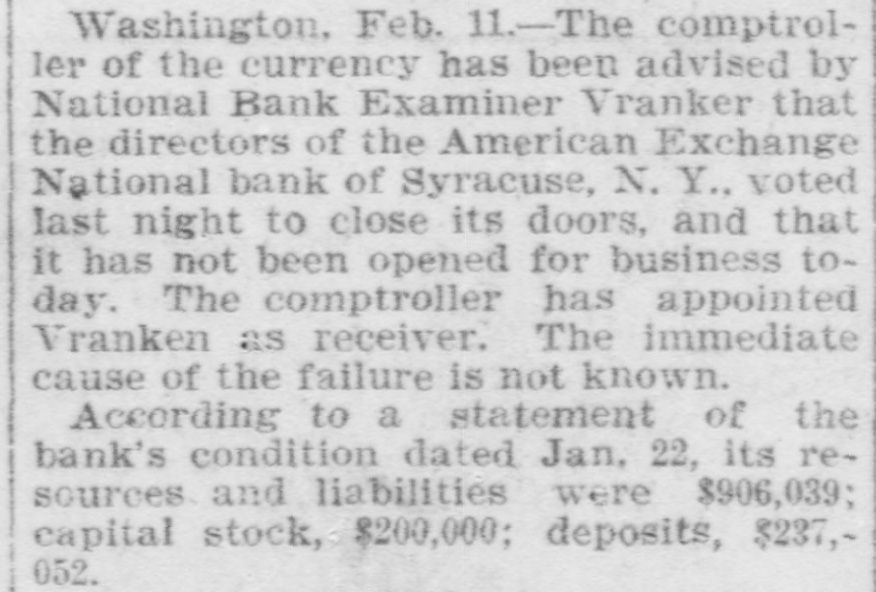

Washington, Feb. 11.-The comptroller of the currency has been advised by National Bank Examiner Vranker that the directors of the American Exchange National bank of Syracuse, N. Y., voted last night to close its doors, and that it has not been opened for business today. The comptroller has appointed Vranken as receiver. The immediate cause of the failure is not known. According to a statement of the bank's condition dated Jan. 22, its resources and liabilities were $906,039; capital stock, $200,000; deposits, $237,052.

Click image to open full size in new tab

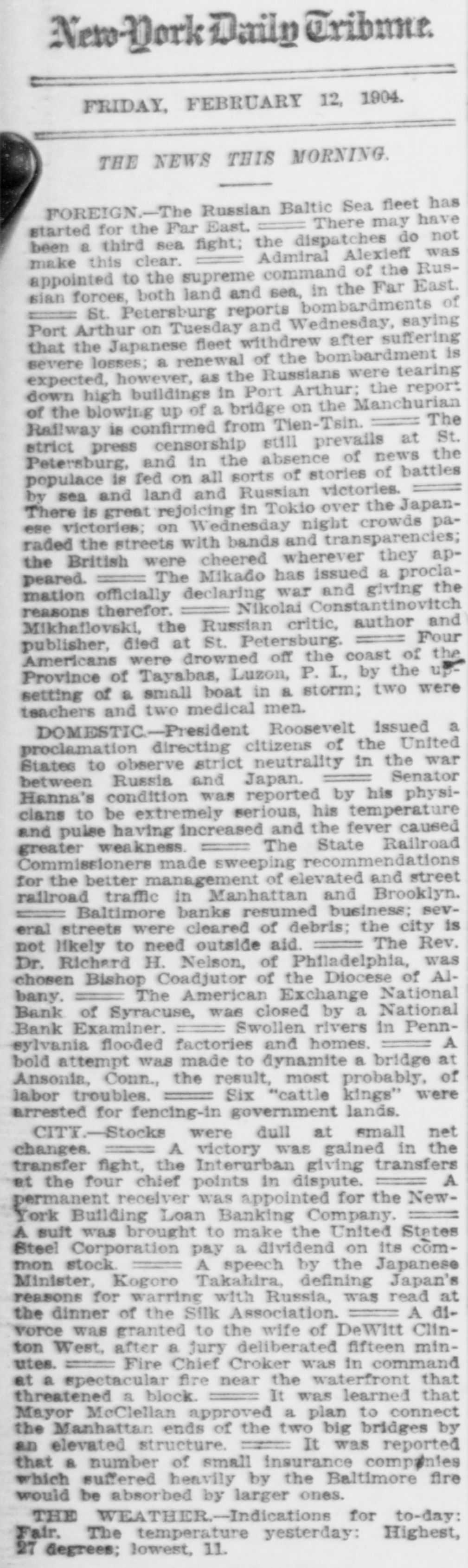

NewDork Daily Cribence FRIDAY, FEBRUARY 12, 1904. the NEWS THIS MORNING. FOREIGN.-The Russian Baltic Sea fleet have has There may started been a for third the sea Far fight; East. the Admiral dispatches Alexieff do was not this clear. make to the supreme command of Far the East. Russian appointed both land and sea, in the of forces, St. Petersburg reports bombardments saying Arthur on Tuesday and Wednesday, suffering Port fleet withdrew after is renewal of the as the Russians expected, severe that the losses; Japanese however, a Arthur; bombardment were the tearing report buildings in Port Manchurian of down the high blowing up of a bridge on the The is confirmed from Tien-Tsin. Railway censorship still prevails at the St. strict press and in the absence of news battles Petersburg, is fed on all sorts of stories of populace by sea and land and Russian victories. the Japanis great rejoicing in Tokio over paThere victories: on Wednesday night crowds ese streets with bands and transparencies; were cheered The Mikado has a the peared. the raded British the wherever issued and giving they procla- apofficially declaring war Constantinovitch mation therefor. Nikolai and reasons Mikhaflovski, the Russian critic, author Four publisher, died at St. Petersburg. were drowned off the coast of the Luzon, P. of a small boat in a storm; setting Province Americans of Tayabas, men. I., by two the were upteachers and two medical Roosevelt issued a directing citizens of war strict neutrality in proclamation States DOMESTIC.-President to observe the the Senator United between Russia and Japan. Hanna's condition was reported by his physiclans to be extremely serious, his temperature caused pulse having increased and the fever greater and weakness. The State Railroad Commissioners made sweeping recommendations street the better management of elevated and for railroad traffic in Manhattan and Brooklyn. Baltimore banks resumed business; sev- is eral streets were cleared of debris; the The city Rev. not likely to need outside aid. Dr. Richard H. Nelson, of Philadelphia, was Alchosen Bishop Coadjutor of the Diocese of The American Exchange National Bank bany. of Syracuse, was closed by a National Bank Examiner. Swollen rivers in Penn- A sylvania flooded factories and homes. bold attempt was made to dynamite a bridge at Conn., the result, most probably. of labor troubles. Ansonia, Six "cattle kings" were arrested for fencing-in government lands. CITY-Stocks were dull at email net the A victory was gained in transfer changes. fight, the Interurban giving transfers A et the four chief points in dispute. permanent receiver was appointed for the NewYork Building Loan Banking Company. brought to make the United States pay a on Steel A suit Corporation was dividend the Japanese its common stock A speech by Minister, Kogoro Takahira, defining Japan's for warring with Russia, was read at of the Silk to the wife of reasons vorce the dinner was granted Association. DeWitt fifteen A Clin- min- d1ton West, after a jury deliberated Chief Croker was in command fire near the a at utes. threatened a spectacular Fire block It was waterfront learned that that Mayor McClellan approved a plan to connect by the Manhattan ends of the two big bridges It was reported an elevated structure. that a number of small insurance companies which suffered heavily by the Baltimore fire would be absorbed by larger ones. THE WEATHER.-Indications for to-day: Fair. The temperature yesterday: Highest, 27 degrees; lowest, 11.

Click image to open full size in new tab

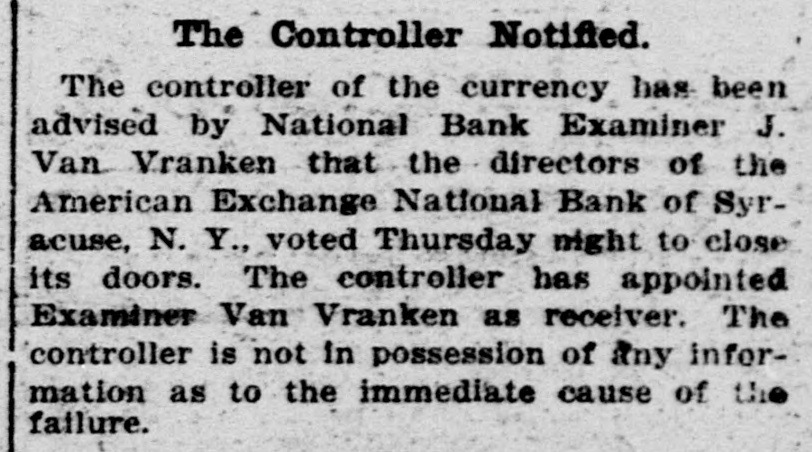

The Controller Notified. The controller of the currency has been advised by National Bank Examiner J. Van Vranken that the directors of the American Exchange National Bank of Syracuse, N. Y., voted Thursday night to close its doors. The controller has appointed Examiner Van Vranken as receiver. The controller is not in possession of any information as to the immediate cause of the failure.

Click image to open full size in new tab

After a run of ten days the Bank of Dunn, N. C., a state institution, closed its doors. Winsor T. White, of Cleveland, O., has been made president of the National Association of Automobile Manufacturers. Baltimore decided to ask for federal troops to patrol the fire-swept district, as the militiamen are needed by their employers in the effort to save business. Mayor McLane decided not to ask for outside aid at present. Secretary Taft told the house committee on insular affairs that slavery had been abolished in the Philippines by legislative action taken there. Charles F. Gould, aged 55, editor of the Evening Bulletin, fell dead while sitting at his desk in Evansville, Ind. Ice gorges in the Susquehanna river were causing great damage at Wilkesbarre, Pa., and other places. Paul Misik, convicted of the murder of Charles O'Brien, was hanged at Hartford, Conn. The Equitable national bank of New York city closed its doors, with deposits of $395,273. A banquet forty feet under Jackson boulevard, in the Illinois Telephone company's tunnel, was given by the latter to 1,200 guests in Chicago. James McDonald, under arrest at Bedford, Ind., charged with the murder of Miss Schafer, collapsed when taken to the scene of the crime. The Iowa antitrust law has been declared unconstitutional by Judge Pratt, of the Waterloo district court. Cattle raisers and shippers of the west charge railroads with conspiracy and with making freight rates excessive. President Roosevelt issued a proclamation, insisting that the citizens of the United States maintain strict neutrality in the Russo-Japanese war. August W. Machen in the postal trial in Washington concluded his testimony and the defense announced that it rested its case. In a fit of insanity at Fort Dodge, Ia., Miss Hulda Nelson killed her mother, a wealthy widow, and then committed suicide. Harlan W. Whipple, of Chicago, has been elected president of the American Automobile association. Two children, aged three and five years, of John E. Butler, were cremated in his home at Superior, Wis. Continued cold weather is a bar to spring trade in the west. Charles E. Kruger was hanged at Greensburg, Pa., for killing Constable Harry Bierer on July 9 last. At Syracuse, N. Y. the American exchange national bank closed its doors with liabilities of $500,000. Three students were expelled from McAllister university at St. Paul for hazing another student. Twenty-five independent tobacco manufacturers formed a league at a Boston meeting to fight the alleged combine. The South Carolina legislature has established a state department of commerce and immigration to secure desirable settlers. Secretary Hay's note regarding the integrity of China makes Washington the center of the world's diplomacy regarding the Russo-Japanese war. Baltimore will gain a more modern business district through the fire, according to the plans now being prepared. The banks have resumed operations and great progress was made in clearing the streets. A Great Northern passenger train at Pennock. Minn., collided with a freight train and four persons were killed.

Click image to open full size in new tab

Dunn, N. C., a state institution, closed its doors. Winsor T. White, of Cleveland, O., has been made president of the National Association of Automobile Manufacturers. Baltimore decided to ask for federal troops to patrol the fire-swept district, as the militiamen are needed by their employers in the effort to save business. Mayor McLane decided not to ask for outside aid at present. Secretary Taft told the house committee on insular affairs that slavery had been abolished in the Philippines by legislative action taken there. Charles F. Gould, aged 55, editor of the Evening Bulletin, fell dead while sitting at his desk in Evansville, Ind. Ice gorges in the Susquehanna river were causing great damage at Wilkesbarre, Pa., and other places. Paul Misik, convicted of the murder of Charles O'Brien, was hanged at Hartford, Conn. The Equitable national bank of New York city closed its doors, with deposits of $395,273. A banquet forty feet under Jackson boulevard, in the Illinois Telephone company's tunnel, was given by the latter to 1,200 guests in Chicago. James McDonald, under arrest at Bedford, Ind., charged with the murder of Miss Schafer, collapsed when taken to the scene of the crime. The Iowa antitrust law has been declared unconstitutional by Judge Pratt, of the Waterloo district court. Cattle raisers and shippers of the west charge railroads with conspiracy and with making freight rates excessive. President Roosevelt issued a proclamation, insisting that the citizens of the United States maintain strict neutrality in the Russo-Japanese war. August W. Machen in the postal trial in Washington concluded his testimony and the defense announced that it rested its case. In a fit of insanity at Fort Dodge, Ia., Miss Hulda Nelson killed her mother, a wealthy widow, and then committed suicide. Harlan W. Whipple, of Chicago, has been elected president of the American Automobile association. Two children, aged three and, five years, of John E. Butler, were cremated in his home at Superior, Wis. Continued cold weather is a bar to spring trade in the west. Charles E. Kruger was hanged at Greensburg, Pa., for killing-Constable Harry Bierer on July 9 last. At Syracuse, N. Y. the American exchange national bank closed its doors with liabilities of $500,000. Three students were expelled from McAllister university at St. Paul for hazing another student. Twenty-five independent tobacco manufacturers formed a league at a Boston meeting to fight the alleged combine. The South Carolina legislature has established a state department of commerce and immigration to secure desirable settlers. Secretary Hay's note regarding the integrity of China makes Washington the center of the world's diplomacy regarding the Russo-Japanese war. Baltimore will gain a more modern business district through the fire, according to the plans now being prepared. The banks have resumed operations and great progress was made in clearing the streets. A Great Northern passenger train at Pennock. Minn., collided with a freight train and four persons were Filled,

Click image to open full size in new tab

From Washington. [Correspondence of the Alexandria Gazette.] Washington, D. C., April 7. An agreement has been reached among the House leaders by virtue of which the matter of impeachment proceedings against Judge Swayne, of Florida, will go over till next December. Representative Palmer, of Pennsylvania, chairman of the sub-committee which took the testimony, will offer a resolution to that effect in the House today. It is expected that it will be adopted without debate, thus clearing the way for an adjournment of the present session of Congrees within two or three weeks. The committee is to be empowered to take additional testimony in the meantime if desired. Personal friends of the President say that his choice for the republican nomination in 1908 is Elihu Root. He says he considers Mr. Root the greatest man in the United States. A train on the Pensylvanja Railroad ran over Frank Nelson, a horse trainer, at Deanwood last night and instantly killed him. The Comptroller of the Currency has appointed John W. Schofield receiver of the American Exchange National Bank of Syracuse, N. Y., which was closed on February 11, 1904, and has since that time been in the hands of National Bank Examiner Josiah Van Vranken. Mr. Rixey has introduced in the House petitions of F. S. Harper and others and E. P. Taylor and others, of Alexandria, against the passage of a parcels-post bill. Governor Franklin Murphy, of New Jersey, is expected to succeed the late Senator Hanną as chairman of the republican national committee. Captain Seth Bullock, Superintendent of the Black Hills Forest Reserve and an old time ranch friend of the President, took luncheon at the White House today. Capt. Bullock was the President's companion in the Yellowstone Park when he made his western trip last year. The House committee on banking and currency today authorized favorable report on the Hill bill to improve currency conditions. The bill among other things authorizes the deposit of customs receipts in national banks; repeals the $3,000,000 limit on withdrawal of circulation in any one month ; abolishes the limit on the coinage of subsidiary coins and permits the issue of gold certificates in denominations of $10. Advocates of action at this session on the eight hour bill received a backset before the House committee on labor today. By a vote of six to three the committee decided to refer the subject to the Secretary of Commerce and Labor who is to investigate what the effect of the proposed legislation will be, The resolution to this effect was offered by Mr. Vreeland, of New York, and adopted, because the temper of the committee was evidently against a favorable report on the bill at this time. The democratic congressional committee will meet tonight to organize for the coming campaign. Representative Griggs, of Georgia, will surrender his place as chairman and will be succeeded by Representative Wm. S. Cowherd, of Kansas City, Mo. Charles A. Edwards, a well known political writer and secretary of the last committee, will probably succeed himself as secretary, although there is some opposition to him on the ground that he is too closely identiffed with the political tortunes of W. R. Hearst. The Census Bnreau today made public its estimates of the population of the United States. The estimates give the present population exclusive of Alaska and the insular possessions as 79,900,389, an increase of 3,905,814 over the census of 1900. According to these

Click image to open full size in new tab

AGED BANKER IN TROUBLE. Grand Jury Investigating Affairs of Defunct Institution. Syracuse, N. Y., Dec. 10.-Manning C. Palmer, president of the defunct American Exchange National bank of this city, which for several months has been in the hands of a receiver, has been taken by a deputy marshal to Utica, where the federal grand jury is now in session. Persons connected with the case refused to talk, but it is known that the grand jury has considered the bank affairs, a number of witnesses subpoenaed from this city having been examined. Mr. Palmer is seventy-four years old and one of the prominent residents of this city.

Click image to open full size in new tab

BANKER GOES BEFORE JURY. President of Defunct National Bank Is Compelled to Appear in Court. Syracuse, N. Y., Dec. 9.-Manning C. Palmer, president of the defunct American Exchange National bank, of this city, which, for several months has been in the hands of a receiver, has been taken by a deputy marshal to Utica, where the federal grand jury is now in session. Persons connected with the case refused to talk, but it is known that the grand jury has considered the bank affairs, a number of witnesses sub poenaed from this city having been examined. Mr. Palmer is 70 years old and is one of the most prominent residents of this city.

Click image to open full size in new tab

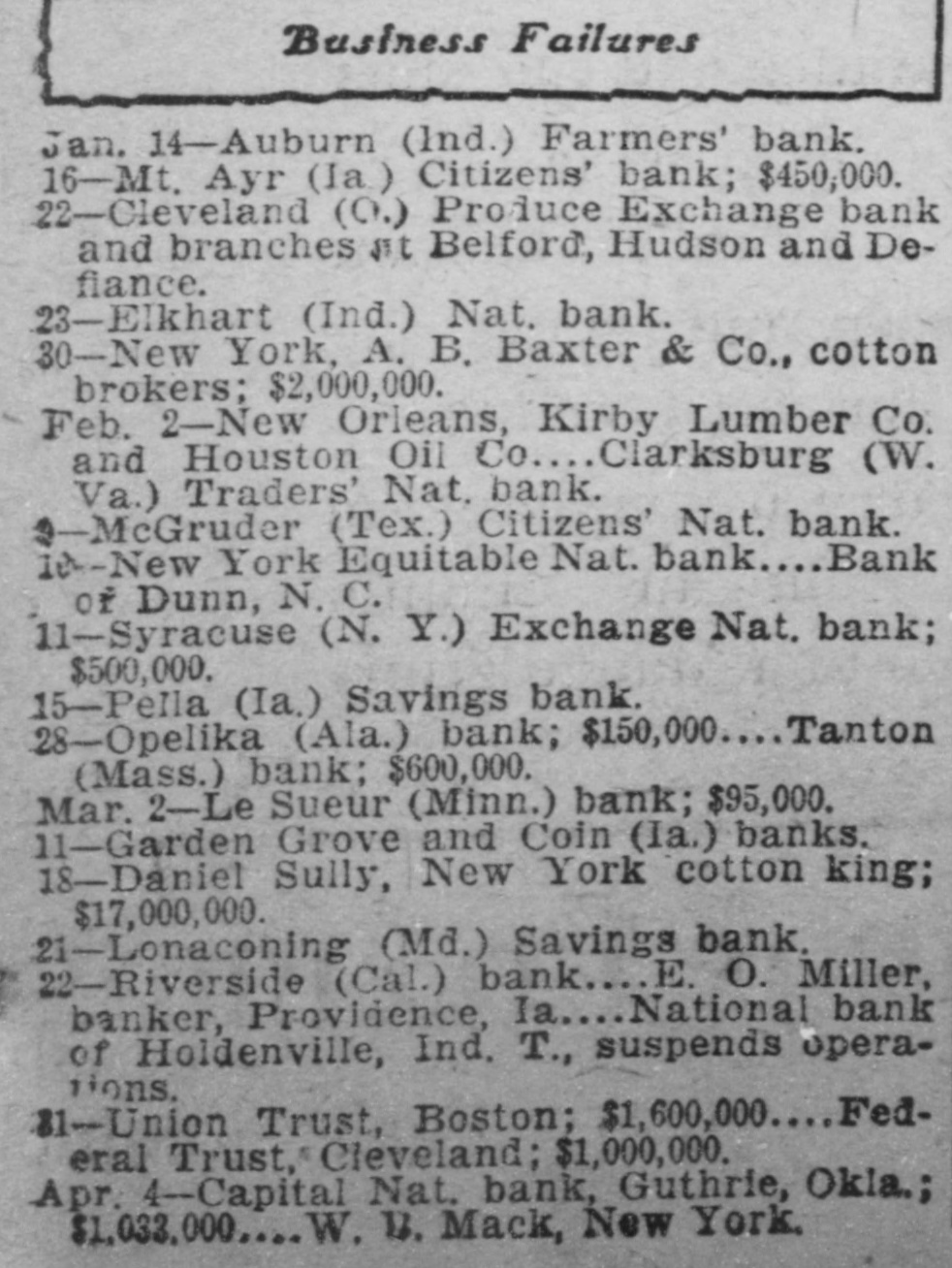

Business Failures Jan. 14-Auburn (Ind.) Farmers' bank. 16-Mt. Ayr (Ia.) Citizens' bank; $450,000. 22-Cleveland (0.) Produce Exchange bank and branches st Belford, Hudson and Defiance. 23-Elkhart (Ind.) Nat. bank. 30-New York, A. B. Baxter & Co., cotton brokers; $2,000,000. Feb. 2-New Orleans, Kirby Lumber Co. and Houston Oil Co Clarksburg (W. Va.) Traders' Nat. bank. 1-McGruder (Tex.) Citizens' Nat. bank. Id-New York Equitable Nat. bank Bank of Dunn, N. C. 11-Syracuse (N. Y.) Exchange Nat. bank; $500,000. 15-Pella (Ia.) Savings bank. 28-Opelika (Ala.) bank; $150,000 Tanton (Mass.) bank; $600,000. Mar. 2-Le Sueur (Minn.) bank; $95,000. 11-Garden Grove and Coin (Ia.) banks. 18-Daniel Sully, New York cotton king; 21-Lonaconing $17,000,000. (Md.) Savings bank. 22-Riverside (Cal.) bank E. O. Miller, banker, Providence, Ia National bank of Holdenville, Ind. T., suspends operaHons. 1-Union Trust, Boston; $1,600,000 Federal Trust, Cleveland; $1,000,000. Apr. 4--Capital Nat. bank, Guthrie, Okla.; $1,033,000 W. B. Mack, New York.

Click image to open full size in new tab

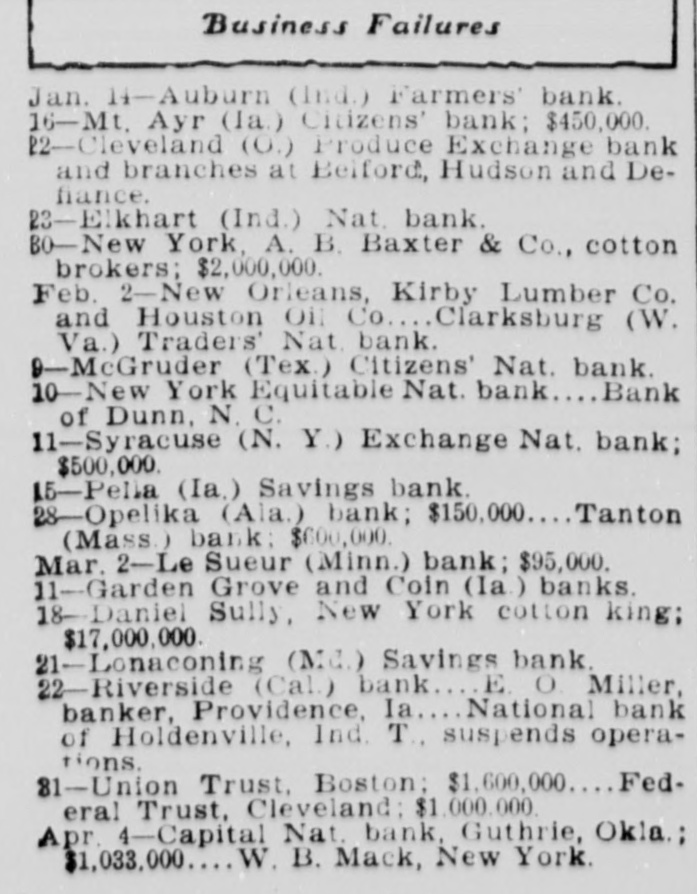

Business Failures Jan. 11-Auburn (Ind.) Farmers' bank. 16-Mt. Ayr (la.) Citizens' bank; $450,000. 22-Cleveland (O.) Produce Exchange bank and branches at Belford, Hudson and Defiance. 23-Elkhart (Ind.) Nat. bank. BO-New York, A. B. Baxter & Co., cotton brokers; $2,000,000. Feb. 2-New Orleans, Kirby Lumber Co. and Houston Oil Co. Clarksburg (W. Va.) Traders' Nat. bank. 9-McGruder (Tex.) Citizens' Nat. bank. 10-New York Equitable Nat. bank Bank of Dunn, N. C. 11-Syracuse (N. Y.) Exchange Nat. bank; $500,000. 15-Pella (Ia.) Savings bank. 28-Opelika (Ala.) bank; $150,000 Tanton (Mass.) bank: $600,000. Mar. 2-Le Sueur (Minn.) bank; $95,000. 11-Garden Grove and Coin (Ia.) banks. 18-Daniel Sully, New York cotton king; $17,000,000. 21-Lonaconing (Md.) Savings bank. 22-Riverside (Cal.) bank E. O Miller, banker, Providence, Ia National bank of Holdenville, Ind. T., suspends operations. 81-Union Trust, Boston: $1,600,000 Federal Trust, Cleveland: $1,000,000. Apr. 4-Capital Nat. bank, Guthrie, Okla.; $1,033,000 W. B. Mack, New York.

Click image to open full size in new tab

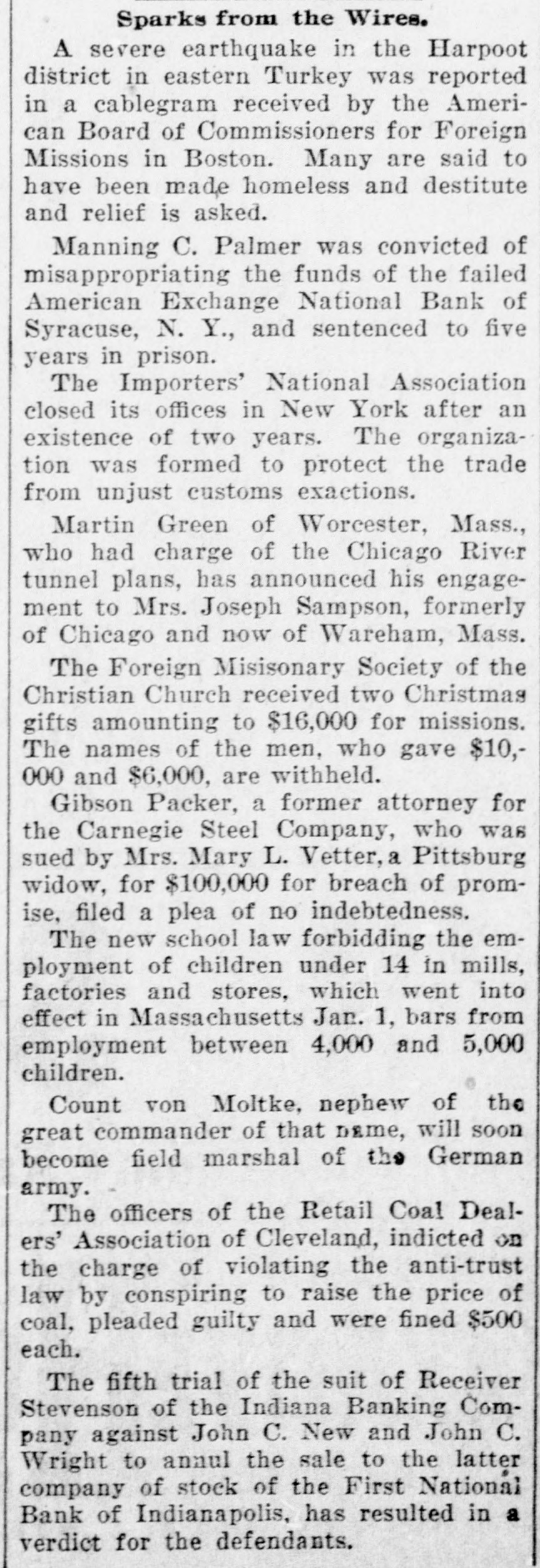

Sparks from the Wires. A severe earthquake in the Harpoot district in eastern Turkey was reported in a cablegram received by the American Board of Commissioners for Foreign Missions in Boston. Many are said to have been made homeless and destitute and relief is asked. Manning C. Palmer was convicted of misappropriating the funds of the failed American Exchange National Bank of Syracuse, N. Y., and sentenced to five years in prison. The Importers' National Association closed its offices in New York after an existence of two years. The organization was formed to protect the trade from unjust customs exactions. Martin Green of Worcester, Mass., who had charge of the Chicago River tunnel plans, has announced his engagement to Mrs. Joseph Sampson, formerly of Chicago and now of Wareham, Mass. The Foreign Misisonary Society of the Christian Church received two Christmas gifts amounting to $16,000 for missions. The names of the men, who gave $10,000 and $6,000, are withheld. Gibson Packer, a former attorney for the Carnegie Steel Company, who was sued by Mrs. Mary L. Vetter, a Pittsburg widow, for $100,000 for breach of promise, filed a plea of no indebtedness. The new school law forbidding the employment of children under 14 in mills, factories and stores, which went into effect in Massachusetts Jan. 1, bars from employment between 4,000 and 5,000 children. Count von Moltke, nephew of the great commander of that name, will soon become field marshal of the German army. The officers of the Retail Coal Dealers' Association of Cleveland, indicted on the charge of violating the anti-trust law by conspiring to raise the price of coal, pleaded guilty and were fined $500 each. The fifth trial of the suit of Receiver Stevenson of the Indiana Banking Company against John C. New and John C. Wright to annul the sale to the latter company of stock of the First National Bank of Indianapolis, has resulted in a verdict for the defendants.

Click image to open full size in new tab

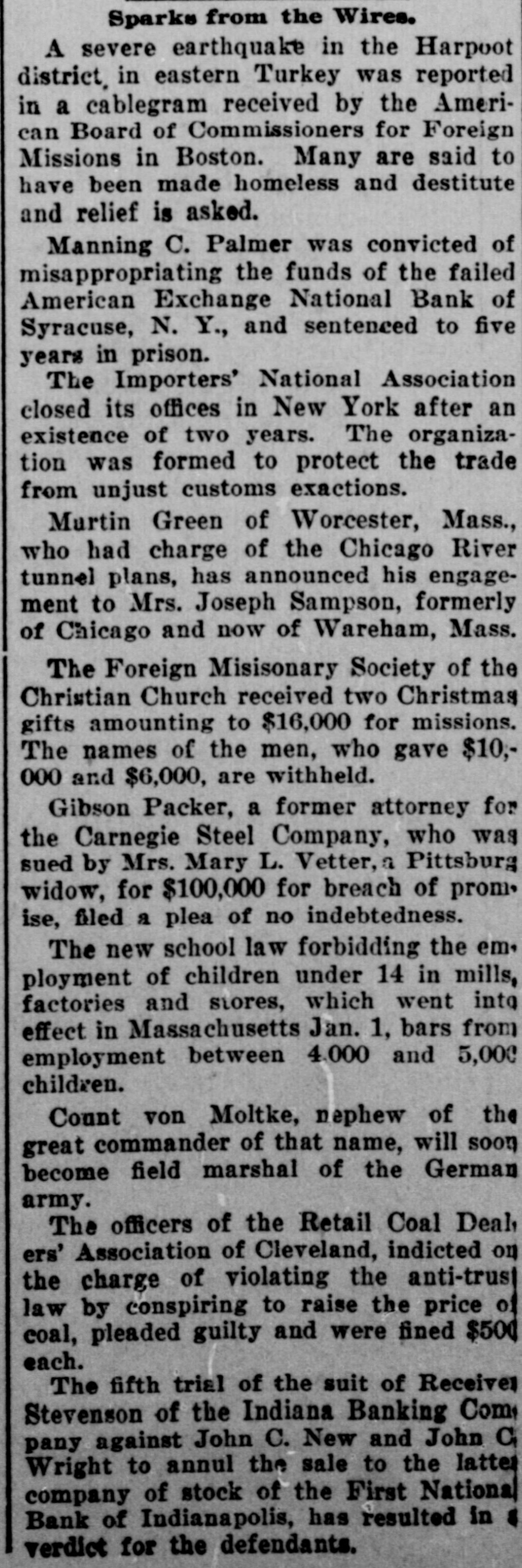

Sparks from the Wires. A severe earthquake in the Harpoot district. in eastern Turkey was reported in a cablegram received by the American Board of Commissioners for Foreign Missions in Boston. Many are said to have been made homeless and destitute and relief is asked. Manning C. Palmer was convicted of misappropriating the funds of the failed American Exchange National Bank of Syracuse, N. Y., and sentenced to five years in prison. The Importers' National Association closed its offices in New York after an existence of two years. The organization was formed to protect the trade from unjust customs exactions. Murtin Green of Worcester, Mass., who had charge of the Chicago River tunnel plans, has announced his engagement to Mrs. Joseph Sampson, formerly of Chicago and now of Wareham, Mass. The Foreign Misisonary Society of the Christian Church received two Christmas gifts amounting to $16,000 for missions. The names of the men, who gave $10;000 and $6,000, are withheld. Gibson Packer, a former attorney for the Carnegie Steel Company, who was sued by Mrs. Mary L. Vetter, a Pittsburg widow, for $100,000 for breach of prom. ise, filed a plea of no indebtedness. The new school law forbidding the employment of children under 14 in mills, factories and stores, which went into effect in Massachusetts Jan. 1, bars from employment between 4.000 and 5,00€ children. Count von Moltke, nephew of the great commander of that name, will soon become field marshal of the German army. The officers of the Retail Coal Deal ers' Association of Cleveland, indicted on the charge of violating the anti-trust law by conspiring to raise the price of coal, pleaded guilty and were fined $500 each. The fifth trial of the suit of Receiver Stevenson of the Indiana Banking Com pany against John C. New and John C Wright to annul the sale to the latte company of stock of the First National Bank of Indianapolis, has resulted in s verdict for the defendants.