Article Text

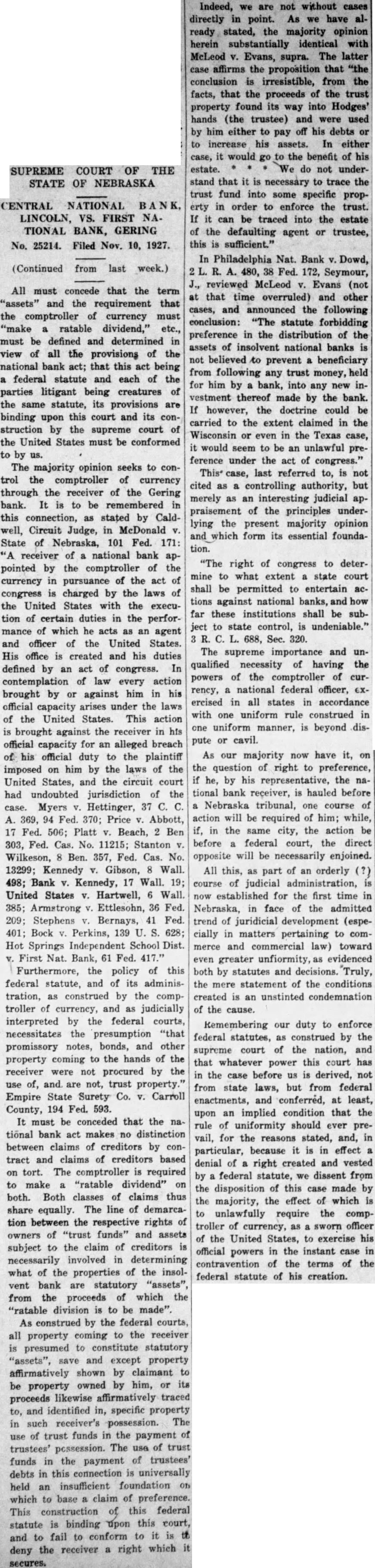

SUPREME COURT OF THE STATE OF NEBRASKA

CENTRAL NATIONAL BANK, COLN V. FIRST NATIONAL BANK, GERING (Continued from Page One) of the property constituting the foundation of plaintiff's suit, or any of the proceeds thereof, as part or whole of any specific assets which reached the possession of the representatives of the comptroller when this bank was taken over by that department. As to three items of property then carried on the books of the Gering bank as "Real estate, $11,940", Furniture and fixtures, $4,906.25", Other real estate, $14,000", it is conceded that they became the property of the Gering bank long prior to the transactions before us; that, under the circumstances of the case, it was physical impossibility for the property in suit, or of any of the proceeds thereof, to have entered into, or to have become incorporated in, any of the properties above named, or in the consideration parted with by the Gering bank for the same. The majority opinion accords the Lincoln bank preference against all the assets of the Gering bank, including even as to the items of real and personal property last set out, and makes the claim of that bank prior charge and an equitable lien against the same. As bearing on the reasons upon which the majority opinion is based, attention is called to the following excerpt: "The proposition that the trust fund did not enter into the purchase of the bank building, furniture, fixtures or bills receivable, as reason for not granting plaintiff the relief sought, will not stand the test of analysis or justify the failure to charge the mass of assets with plaintiff's claim. It destroys itslef when reduced to definite philosophy. The principal mediums of exchange in the business world are credits, commercial paper, checks, drafts and securities. Equity looks through the mere forms which property is held to substance and reason for the purpose of dealing justly with conditions as they exist. Though the converted trust funds were not originally hid in or mingled with the kinds of property enumerated, the bank indebtedness was nevertheless reduced by the proceeds used for banking purposes. The general indebtedness with which those items of property were burdened was decreased to the extent of the trust fund wrongfully verted and used by the insolvent bank. The outstanding obligations of defendant would have been greater to the extent of when the receiver took charge, if they had not been reduced by the proceeds of the notes. The financial disaster of the insolvent bank might have occurred earlier, with still greater liabilities, except for the unlawful use of the converted proceeds in banking transactions. All that seems to me to be 'manifest', in considering plaintiff's right to preference over general creditors, is that it immaterial whether the converted proceeds were used to purchase the bank building, furniture, fixtures and bills receivable or reduced the insolvent bank's indebtedness by which those items of property were burdened." Central Nat. Bank First Nat. Bank, 115 Neb. 745. True, the language just quoted appears in the former dissenting opinion by Rose, J., but the following also appears in the present majority opinion: "Four members of the court entertain the view that the dissenting opinion contains the better solution of the question presented by the appeal (Central Nat. Bank First Nat. Bank, 213 745, 115 Neb.), and it is therefore adopted as the opinion of the court." In this connection also appears the majority opinion the further statement: "That the assets augmented by proceeds of the notes is also a proper deduction from the evidence." While it is deemed that the conclusion last stated is refuted by the facts as detailed in the opinion by

Good, and in the concurring opinion by Eberly, J., no good can be served by their further discussion. However, careful examination of the majority opinion, especially in view of the language of Rose, quoted, inevitably leads to the conclusion that we have before recrudescence of the philosophy and principles promulgated in the once leading, but now over-ruled, and almost universally discredited, case of McLeod Evans, 66 Wis. 401. The result arrived at, the controlling principles announced, and application made to the facts as assumed to be reflected by the record in the Wisconsin court, are in all respects identical with the majority opinion in the present case. Cole, in that opinion says in part: conclusion is irresistable, from the facts, that the proceeds of the trust property found its way into Hodges' (the insolvent trustee) hands, and used by him either to pay off his debts or to increase his assets. In either case, it would go to the benefit of his estate. We do not understand that it is necessary to trace the trust fund into some specific property in order to enforce the trust." Accordingly, that court awarded lien by preference for the entire amount received by Hodges. But, as set forth in the former majority opinion by Good, J., in this case, this doctrine was expressly overruled in Nonotuck Silk Co. Flanders, 87 Wis. 237. Without rurther discussion we will content ourselves with reference to note in Pomeroy, Equitable Jurisprudence (4th ed.) 2386, Sec. 1049, where, after stating the rule as announced in the opinion by Good, J., it continues: "The contrary holding confuses the lien with the trustee's personal liability. Such confusion harmless in its results when the trustee is solvent; but where his assets are insufficient to pay his debts, the question becomes important as between the beneficiary and the general creditors. To extend the lien in such case to the general mass of the trustee's assets is to pervert the character of the personal liability of the trustee-a 'simple' equitable to render the cestui que trust preferred creditor, irrespective of his inability to establish any right of property in a specific portion of the trustee's estate. Such, however, was the result attained, for time, by the decisions in of which have since been repudiated group of western states, nearly all by the courts which rendered them: McLeod Evans, 66 Wis. 401, 57 Am. Rep. 287, 28 N. W. 175, 214, (but see Nonotuck Silk Co. Flanders, 87 Wis. 237, 58 N. W. 383; Burnham Barth, 89 Wis. 362, 62 N. 96); Davenport Plow Co. Lamp, 80 Ia. 722, 20 Am. St. Rep. 442, 45 W. 1049, (but see Bradley Chesebrough, 111 Ia. 126, 82 W. 472; compare Whitcomb Carpenter, 134 la. 227, 10 928, 111 W. 825; McCutchen Roush, 139 Ia. 351, 115 W. 903; Myers Board of Education, Kan. 87, 37 Am. St. Rep. 263, 32 Pac. 658, (but see Travelers Ins. Co. Caldwell, 59 Kan. 156, 52 Pac. 440; Kansas State Bank First State Bank, 62 Kan. 788), 64 Pac. 634); Carley Graves, 85 Mich. 468, Am. St. Rep. 99, 48 (but see Board of Fire Water Commissioners Wilkinson, 119 Mich. 655, 44 L. R. A. 493); State Bruce, 17 Idaho 134 Am. Rep. 245, 1916C, 102 Pac. 831, (see Bellevue State Bank Coffin, 22 Idaho, 210), 125 Pac. 816); Capital Nat. Bank Coldwater Nat. Bank, 49 Neb. 786, 59 Am. St. Rep. 572, 69 W. 115, (but see State Bank of Commerce, 54 Neb. 725, 75 N. 28; City of Lincoln Morrison. 64 Neb. 822, 57 A. 885." The note, quoted, correctly indicates that in State Bank of Commerce, 54 Neb. 725, and in City of Lincoln Morrison, 64 Neb. 822, this court refused to follow McLeod Evans, supra, and denied preference as to trust funds which "might have been" or "were dissipated" in payment of the indebtedthe trustee. In City of Lincoln Morrison, supra, this position reaffirmed. and Pound, C., who liveres the opinion of this court, says, in substance: not able to agree" with the rule stated McLeod Evans, supra. Certainly, these former opinions, last referred to, have been seriously limited, or materially modified, not wholly overruled, by the latest pronouncement of the present majority.

Conceding that the majority are right in the instant case (which We do not), the profession is entitled to know the full effect of the same as applied to previous decisions. We earnestly protest that the public entitled to have the law stated from this bench, not only with clearness and certainty as to the disposition of the case now before the court, but also to have its full effect upon prior decisions declared. Other serious objections to the majority opinion are that it overlooks the fact that the fundamental issue here presented is controlled by the "national bank act", ignores the policy and interpretation of that act as made by the federal decisions, and fairly denies to the receiver here the right which that statute secures. Then, too, it in opposition to the trend of legal development which, as evidenced both by statute and decision, is towards greater uniformity. With reference to the national bank act, the supreme court of the United States said at very early day: consider that act as constituting by itself complete system for the establishment and government of national banks, prescribing the manner in which they may be formed, the amount of circulating notes they may issue, the security to be furnished for the redemption of those in circulation; their obligations as depositaries of public moneys, and as such to furnish curity for the deposits, and designatthe consequence of their failure to redeem their notes, their liability to be placed in the hands of a receiver, and the manner, in such event, in which their affairs shall be wound up, their circulating notes redeemed, and other debts paid or their property applied towards such payment. Everything essential to the formation of the banks, the issue, security, and redemption of their notes, the winding up of the institutions, and the distribution of their effects, are fully provided for, as in a separate code by itself, neither limited nor enlarged by other statutory provisions with respect to the settlement of demands against insolvents or their estates." Cook County Nat. Bank United States, 107 U. S. 445. The controlling question before the court in Cook County Nat. Bank United States, Supra, was whether the United States was entitled to preference against the receiver of the bank under section 3466, Rev. St. S., then existing, which provided: "Whenever any person indebted to the United States is insolvent, or whenever the estate of any deceased debtor, in the hands of the executors or administrators, is insufficient to pay all the debts due from the deceased, the debts due to the United States shall be first satisfied; and the priority hereby established shall extend as well to cases in which debtor. not having sufficient property to pay all his debts, makes voluntary assignment thereof, or in which the estate and effects of an absconding, concealed, or absent debtor are attached by process of law, as to cases in which an act of bankruptcy committed." This claim of preference on part of the government was denied by the court in the following language: "This section (national bank act) provides for the distribution of the entire assets of the bank, giving no preference to any claim except for moneys to imburse the United States for adredeeming the notes. When this reimbursement is fully provided for, the balance of the assets, as the proceds are received, is subject to ratable dividend on all claims proved to the satisfaction of the receiver, or adjudicated by a court of competent jurisdiction. Any sum remaining after the payment of all these claims to be handed over to the stockholders in proportion to their respective shares. These provisions could not be carried out it the United States were entitled to priority in the payment of demand not arising from advances to redeem the circulating notes. The balance, after reimbursement of the advances, could not be distributed, as directed, by a ratable dividend to all holders of claim; that is, to all creditors." Cook County Nat. Bank United States, supra. It may be said in this connection that this decision is in line with the executive practice as evidenced by an opinion rendered by the attorney general of the United States in 1871. 13 Opinions of Attorneys General, 528. This federal statute was again be- fore the supreme court of the United States in Davis Elmira Savings Bank, 275. New York had enacted law providing: "All the property of any bank or trust pany which shall become shall, after providing for the payment of its circulating notes, be applied in the place to the payment in full of any sum or sums of money deposited therewith by any savings bank." The receiver of an insolvent national bank, under authority of the comptroller of currency, declined to accede to demand for preferred payment under the terms of the state law, predicating his refusal on the ground that the preference was prohibited by the national bank act. The state law was sustained by the state courts, but on appeal to the supreme court of the United States the courts New York were reversed, the state law held invalid, and the preference denied. Mr. Justice White, who reviews the previous decisions of the court, in delivering the opinion of the court, says in part: "National banks are instrumentalities of the federal government, created for public purpose, and as such necessarily subject to the paramount authority of the United States. It follows that an attempt, by a state, to define their duties or control the conduct of their affairs is absolutely void, wherever such attempted exercise of authority expressly conflicts with the laws of the United States, and either frustrates the purpose of the national legislation, or impairs the efficiency of these agencies of the federal government to discharge the duties, for the performance of which they were created. These principles are axiomatic, and are sanctioned by the repeated adjudications of this court." Davis Elmira Savings Bank, supra.

(To be continued next week)