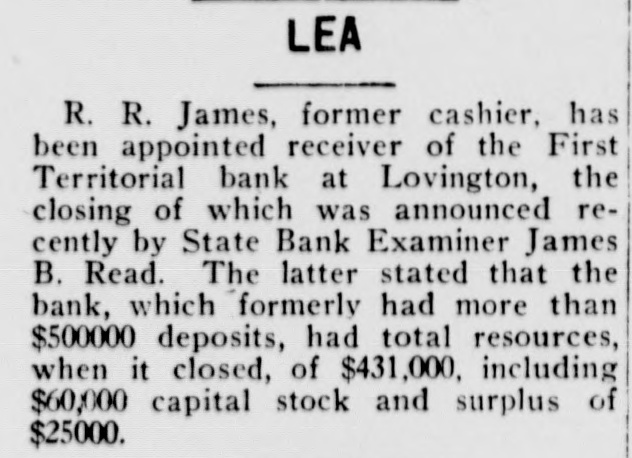

Article Text

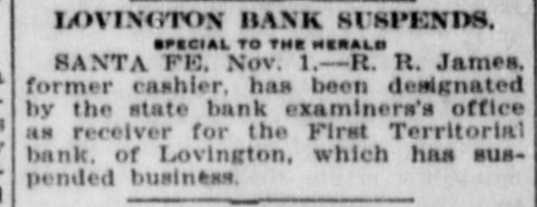

LOVINGTON BANK SUSPENDS. SPECIAL TO THE HERALD SANTA FE. Nov. 1.-R. R. James. former cashier, has been designated by the state bank examiners's office as receiver for the First Territorial bank. of Lovington, which has suspended business.