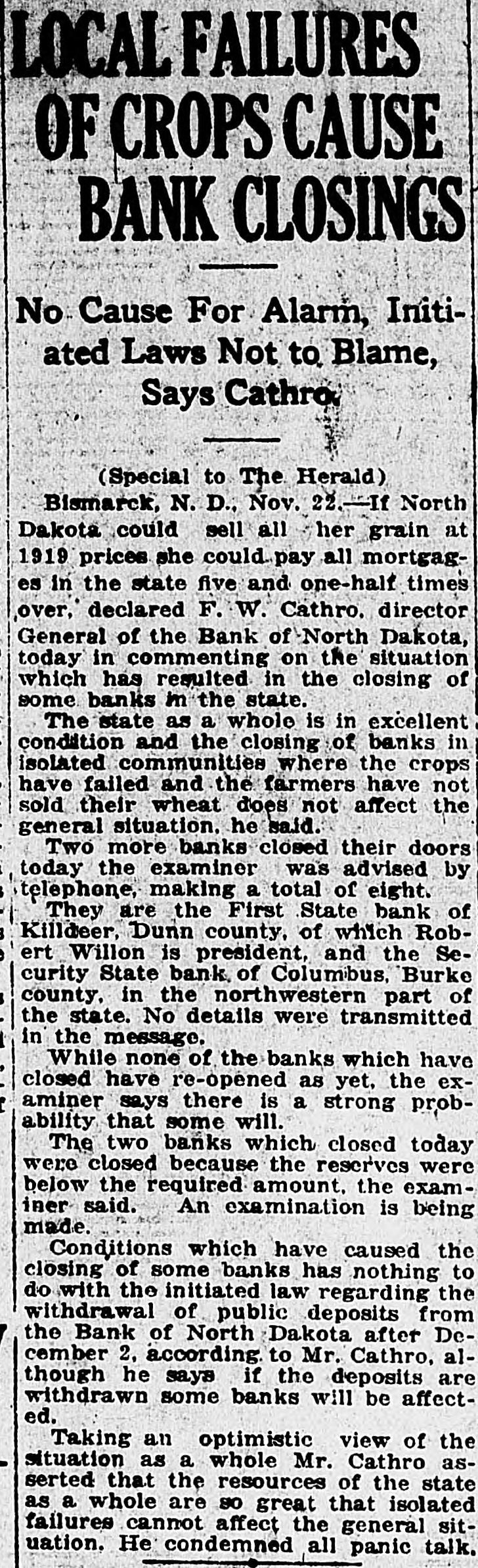

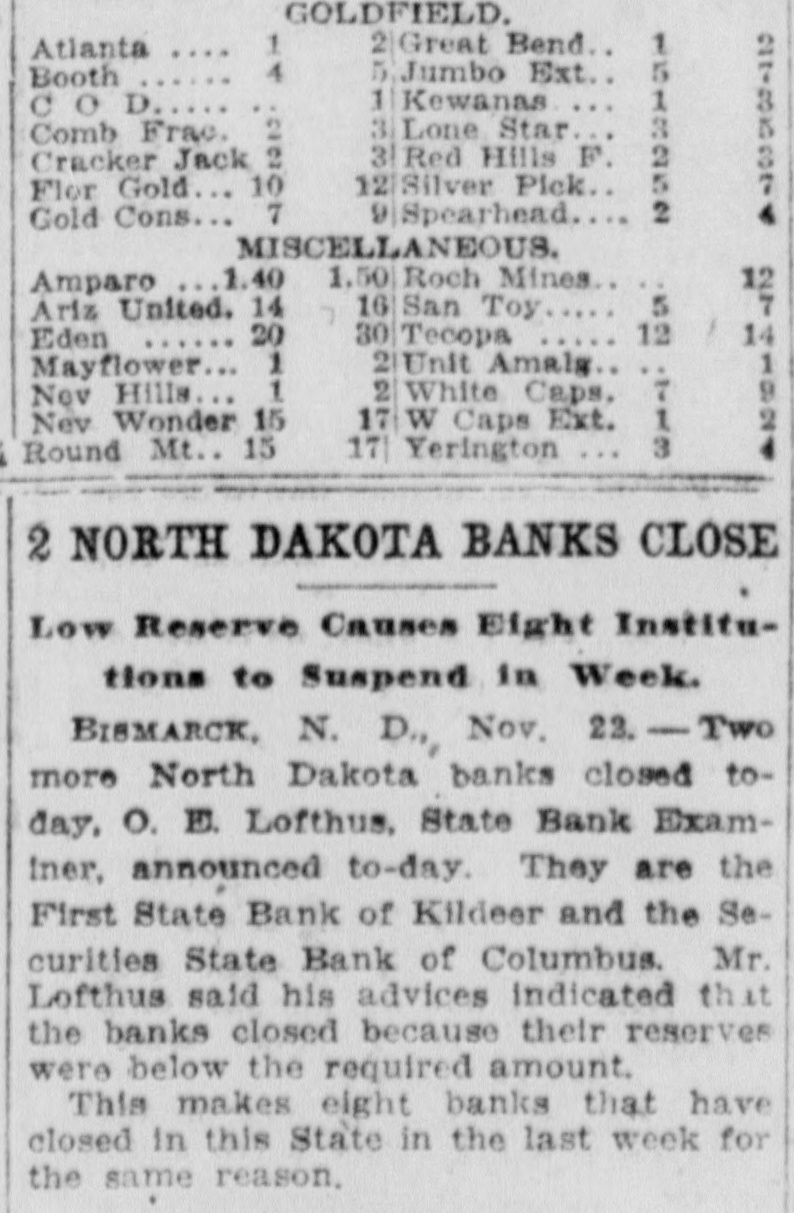

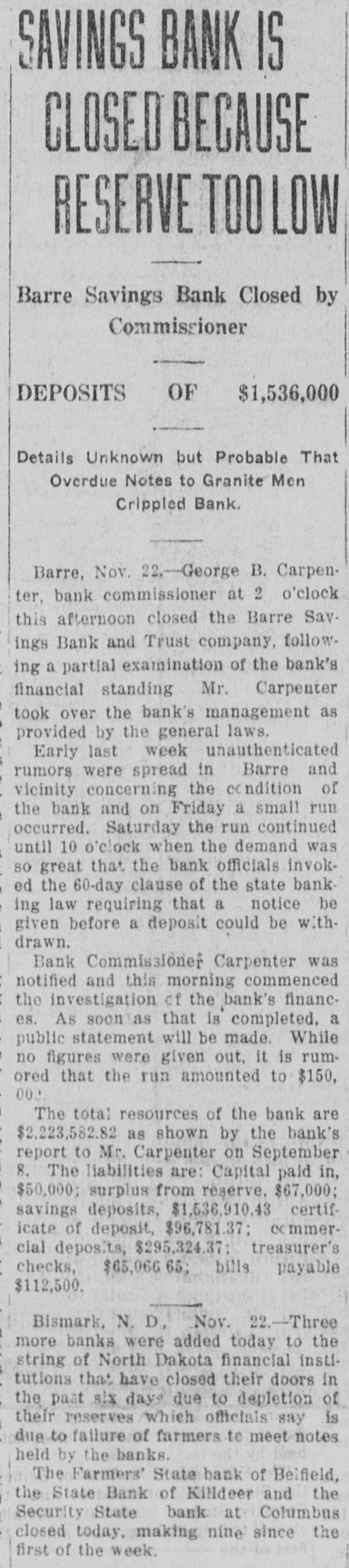

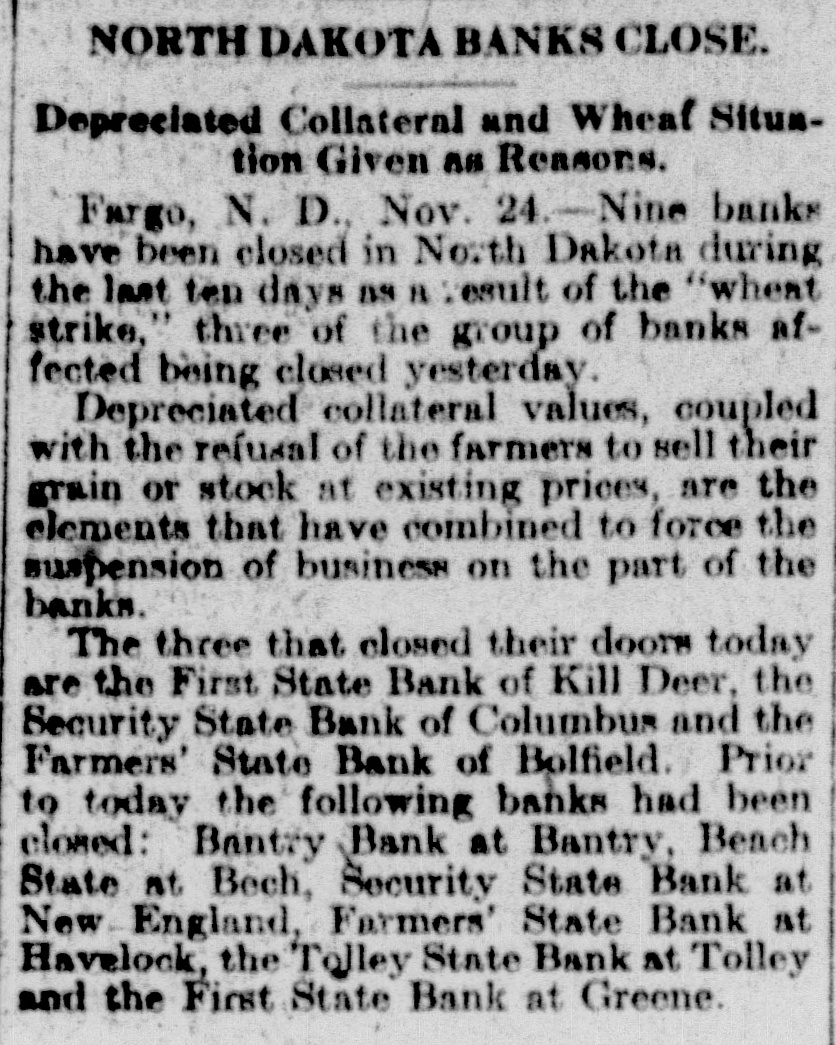

Click image to open full size in new tab

Article Text

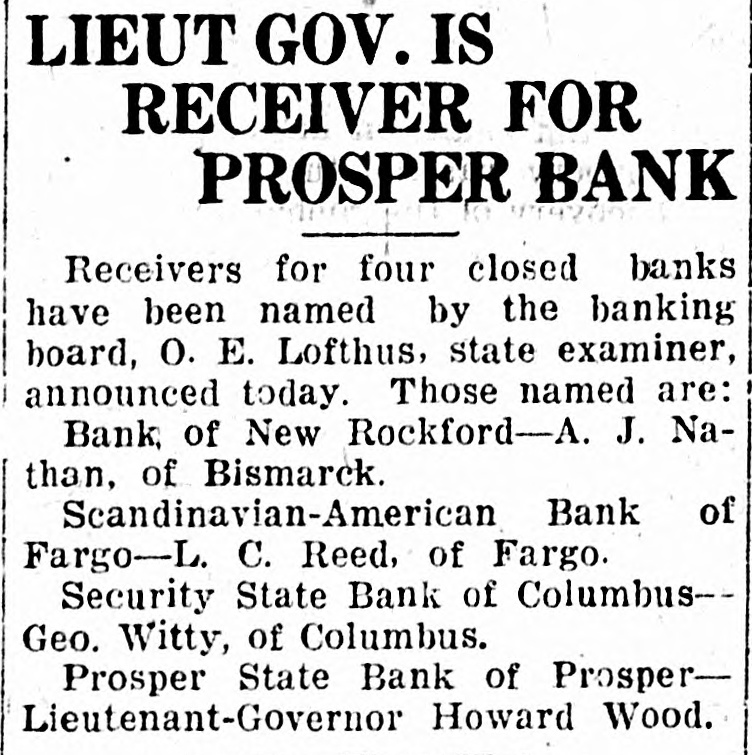

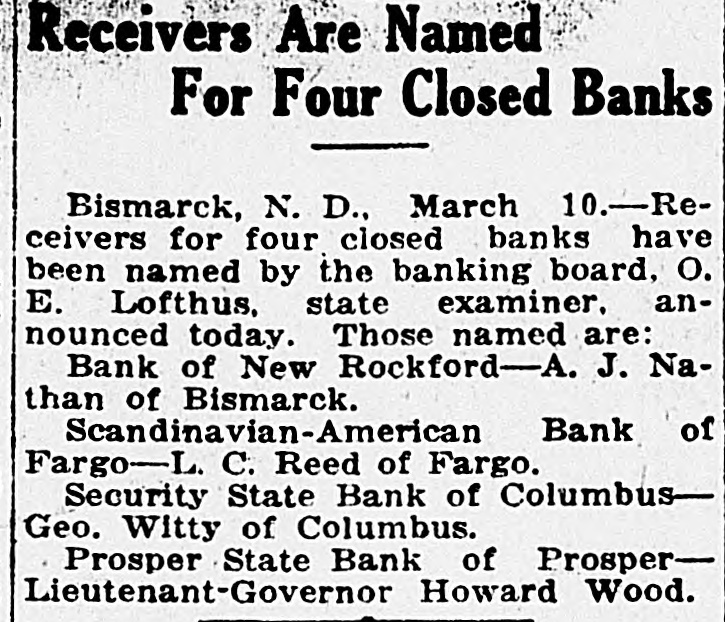

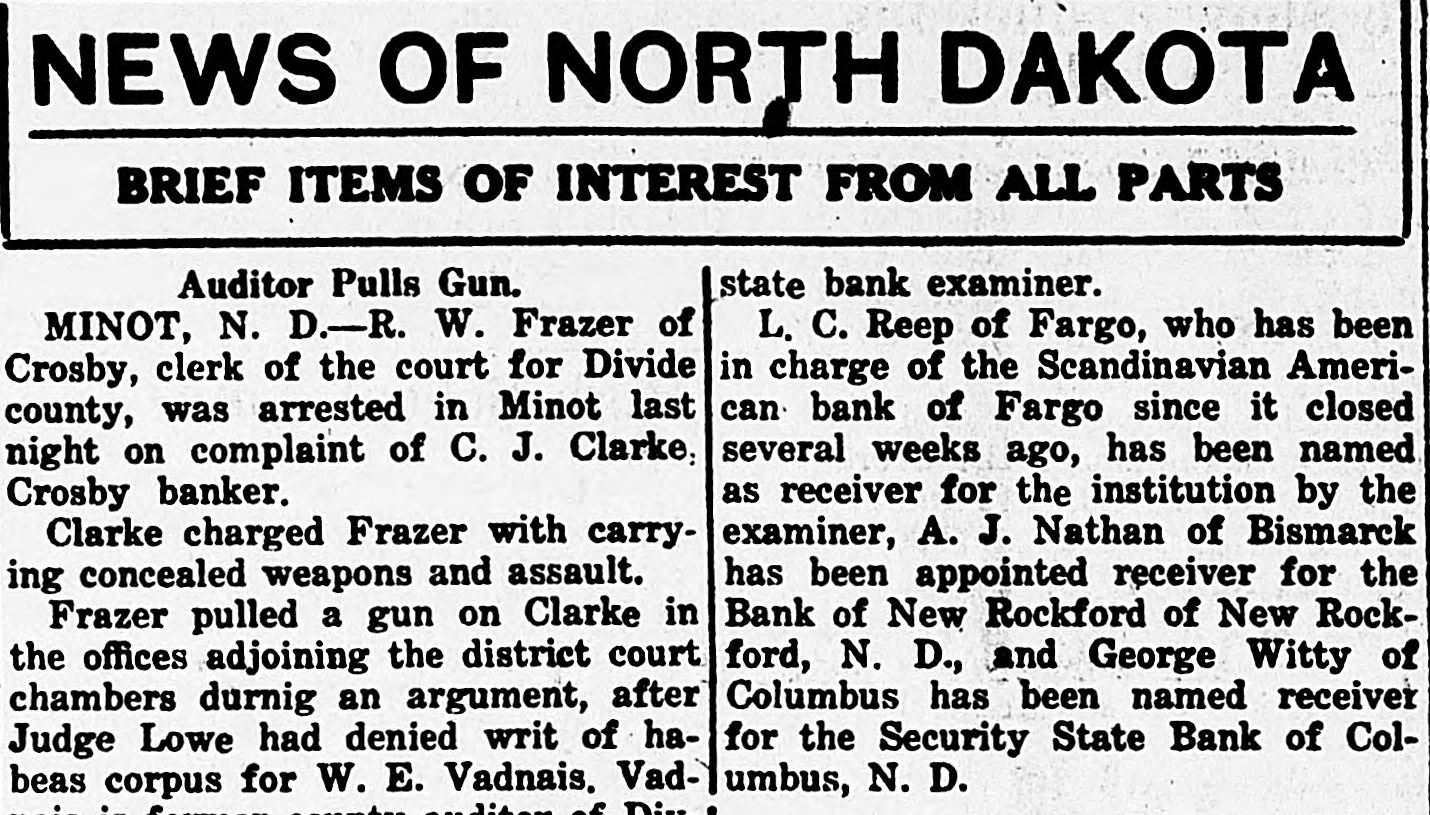

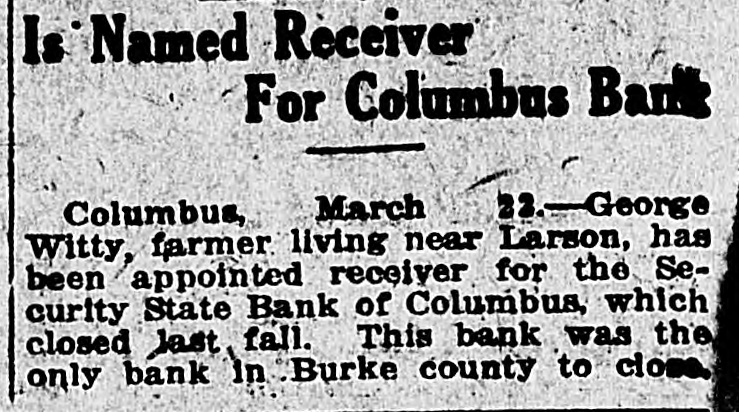

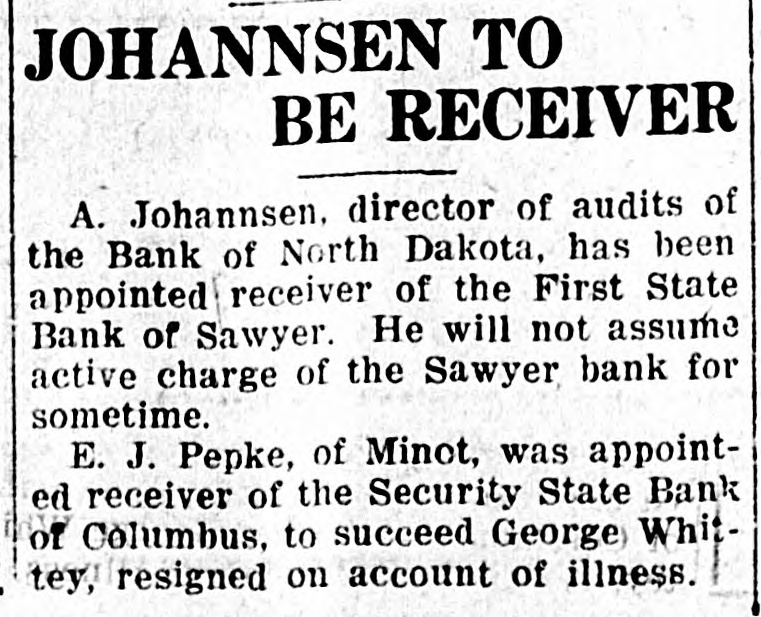

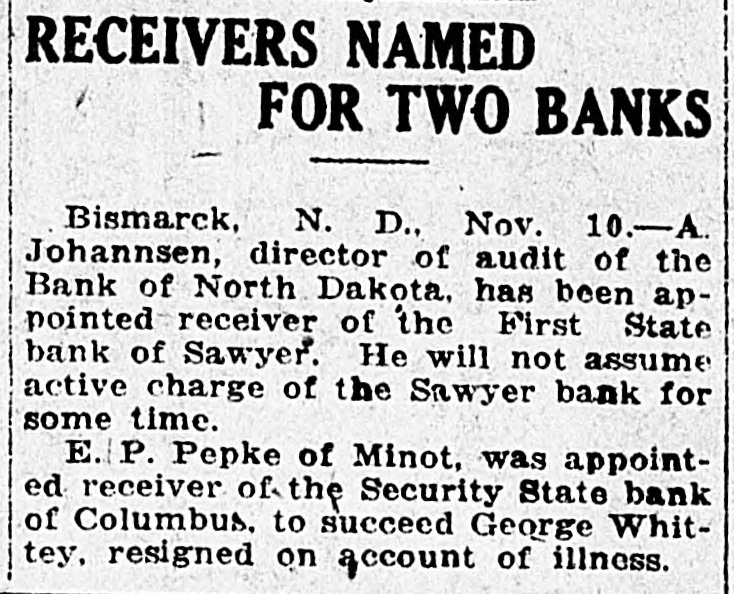

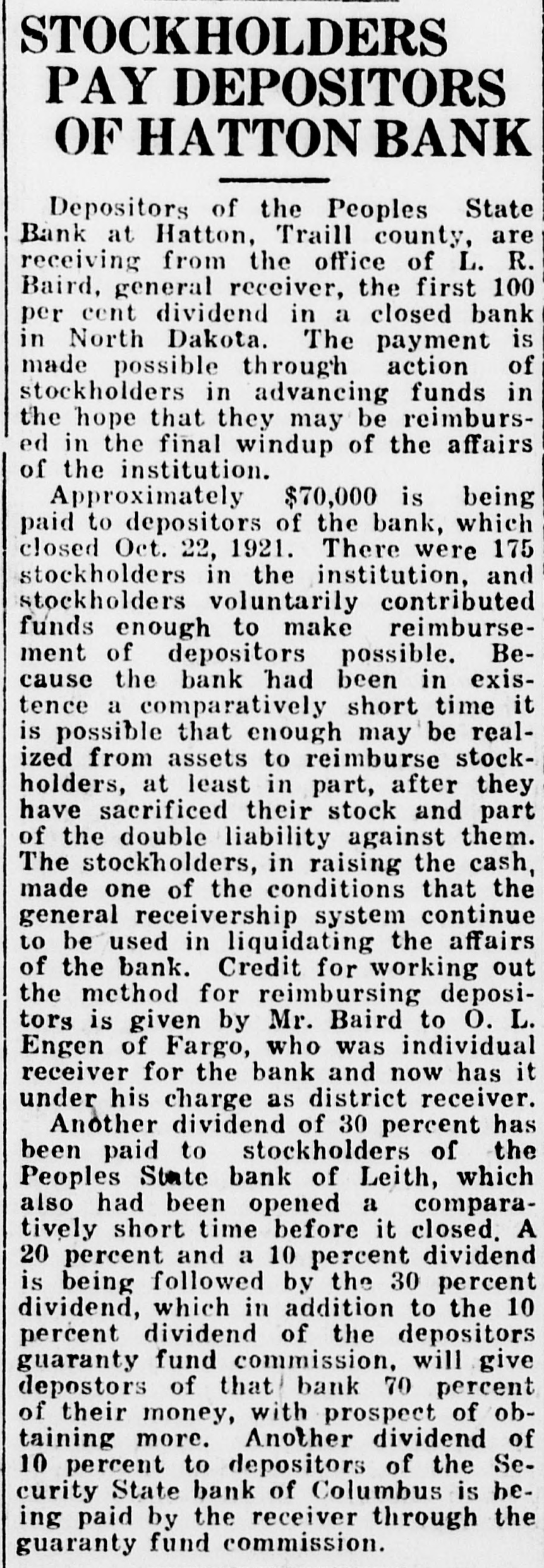

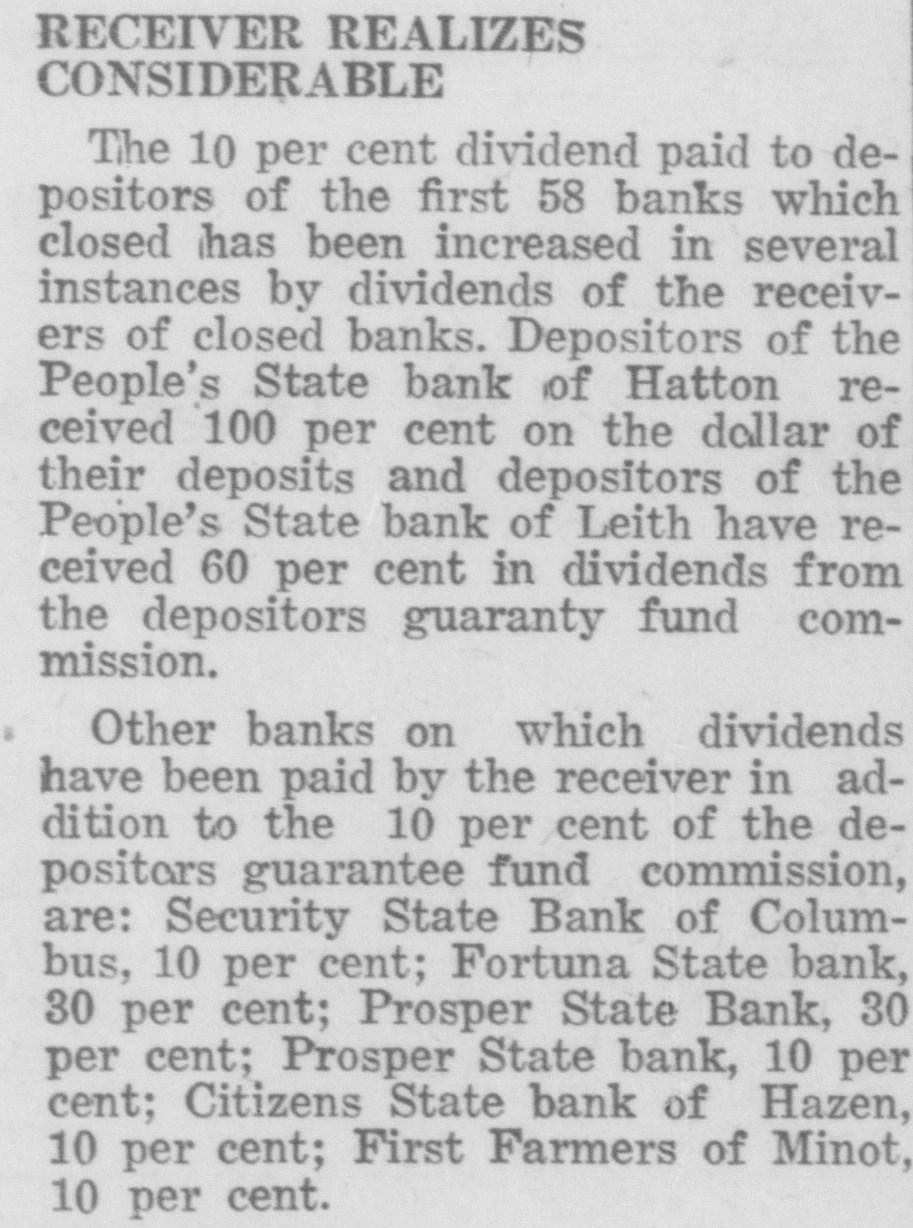

WE EXTEND OUR THANKS BULLETIN The local league organ, after maintaining the silence of the grave on curThe Free Press last week admitted rent affairs for several weeks, makes the loss of $17,688.31 on the Drake up for lost time last week by being mill. Before election the Free Press filled from end to end on dope on how assured its readers that the Drake "Big Bizz" is wrecking the "farmers' mill was making $40,000 per year. program." It is evident that the MACCABEE NOTES been "dope off editor" the job of temporarily, the Free Press and left has the league editor with no choice but to ignore everything that has been Mrs. Elizabeth Dow, of Mandan, going on. District Deputy for the W. B. A. of M. formerly known as Lady MaccaThe Record is again profusely accused of lying. That reminds us that bees, came down last Wednesday and once upon a time the Free Press outworked the town for beneficiary memfit said something about a $100 reward bers last Thursday and Friday. She succeeded in getting a large class of offer if the Record would prove statements that they claimed to be lies. new members, 11 ladies being initiated Friday night. When called, they shut up tight, as After the election and general busiEmmons county people will well remember. This time, the Record is ness session, a social session was held, closing with a fine lunch. charged with lying, but they are more This makes a membership of 23, and circumspect. They simply make the three more pledged to be taken in the charge, and let it go at that. next time they meet. Now, after waiting several weeks, This is a wonderful Benefit Associathe Free Press attacks the list of banks published by the Record Feb. tion, and there isn't any reason why it shouldn't prosper here. 10th. They say Linton banks were not included. Certainly they were not, and for the following reason: Our BANK AT BRADDOCK CLOSES original list was published simply to DOORS show what mammoth deposits were being made in some of the banks of Farmers State Bank, After Four or this state, and the capital and surplus Five Years of Existence, Gives Up. was given to show the comparative Farmers Elevator Reported Hard size of the banks so favored. The LinHit. ton banks were not included because they have not been carrying a lot of The Farmers State Bank of Bradleague paper, and consequently dock has closed its doors. Reports haven't had great favoritism shown received in Linton are to the effect them by the Bank of North Dakota. that the bank had overextended loans However, we will now be glad to acand was no longer able to meet its commodate the local league sheet. In obligations. Being unable to secure fact, it gives up an additional chance further financial backing, the directors to bring home to our readers the vast decided to close voluntarily favoritism shown by the great Bank of North Dakota. The only bank to close in Emmons as yet, the Farmers State Bank had a Here are the figures for the Linton banks, which the Free Press seems to large list of stockhelders. When it was organized, small blocks of stock desire: as of December 3d, the date of were sold to all who would buy in the report, the Braddock neighborhood. Some Liability to sixty or seventy farmers took stock Cap. Surp. Bk. of N. D. City National in varying amounts. Its total capi$35,000 $7,508.59 First National tal amounted to $20,000, and it has 9,256.28 40,000 never been able to build up any rePeoples State 25,000 2,008.89 serve. Its last published statement Now, then, Free Press, compare the was made Dec. 29th, and showed total figures of Linton banks with those deposits of $79,008.29. Of this published in our issue of Feb. 10th, amount, $36,750.97 were time deposits, which seems to have "gotten your and a great share of these accounts goat. We republish a few samples: Busted Banks: doubtless are tied up with the bank's closing. It is said that some $6,000 Liability to belonging to the Farmers' Elevator Cap. Surp. Bk. of N.1 Co., of Braddock, was in the bank Donnybrook State $33,400 $93,534.31 when it closed, thus making that in(A bank now busted, with capital stitution short on ready money. Its and surplus less than either the First loans and discounts amount to $100,National or City Natioanl, of this city, 000. has ten, times as much state funds as O. R. Martini was president, Henry either Linton bank.) Reamann vice president and R. E. $20,000 Tolley State $63,588.85 McCain cashier. Mr. McCain came Security State, Coto Braddock from Mott, where he had lumbus 27,700 50,129.55 been in the machinery business, to Fortuna State 20,000 47,111.06 take charge of the bank when it was (These are all closed banks) first opened. Banks Still Running: Slope County ALLIES AWAIT INAUGURATION State, Amidon 11,500 71,381.90 First State, KloLeague of Nations to Take up U. 8. ten 20,500 65,619.33 Tangle With Harding. (The bank Lofthus was running Paris-The League of Nations counwhen appointed state bank examiner) cil stopped work on matters affecting Farmers' Bank, the United States, pending inauguraRay 12,000 53,375.69 tion of the new president. Receiving And here are Jorgen Olson's three the American protest against the banks, with total capital and surplus awarding of the Mesopotamian manof $100,300, and liabilities to Bank of date to Great Britain, the council deNorth Dakota of $256,582.89. The cided to await a decision by the Allied Supreme Council. The Allied council three Linton banks total capital and at London already had indicated that surplus of $100,000 and their total it would take no action on American liability to Bank of North Dakota is affairs until Senator Harding became $18,733.76. president. Some fine comparisons, aren't they? And we're duly glad that the league MAIL PLANES MAKE RECORD paper called our attention to the possibility of these particular compariFilers in Relay Go From Coast to Coast sons. in 33 Hours 20 Minutes. The Free Press opines that the capiHazelhurst, N. Y.-Eight bags of tal and surplus has nothing to do mail dispatched from San Francisco by with the ability of the various banks airplane at 4:30 Wednesday morning arrived at Hazelhurst field here the to meet their obligations. Quite true, indeed. But, as the state examiner is next day at 4:50 p. m., establishing a cross country record of 33 hours the only one who can get a peek at and 20 minutes, with allowance for the paper in these various banks, the time zone changes in the coast to above is the most we can do to give coast flight. the people a line on relative condiThe mail was transferred from plane tions. to plane in a relay flight ordered by the Postoffice department to establish We might, however, state that the a new cross-continent mail record. evidence at the hearing in Bismarck shows that the state bank examiner's Kaiserin's Condition Worse. fieldDoorn, Holland-The physician atmen some be office showing had had reports of the from banks its to tending former Empress Augusta Vic toria considers her condition too seriin rotton condition which were being