Click image to open full size in new tab

Article Text

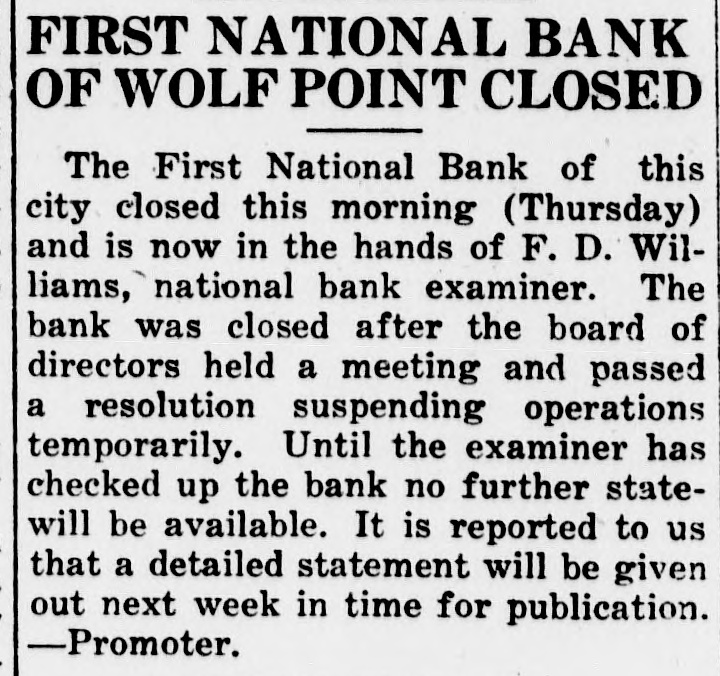

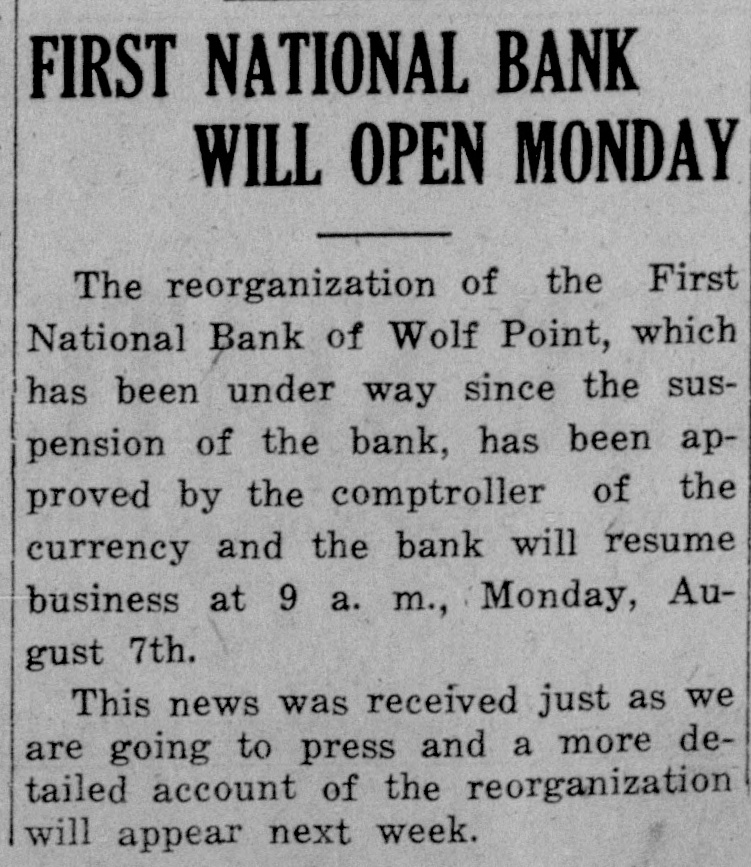

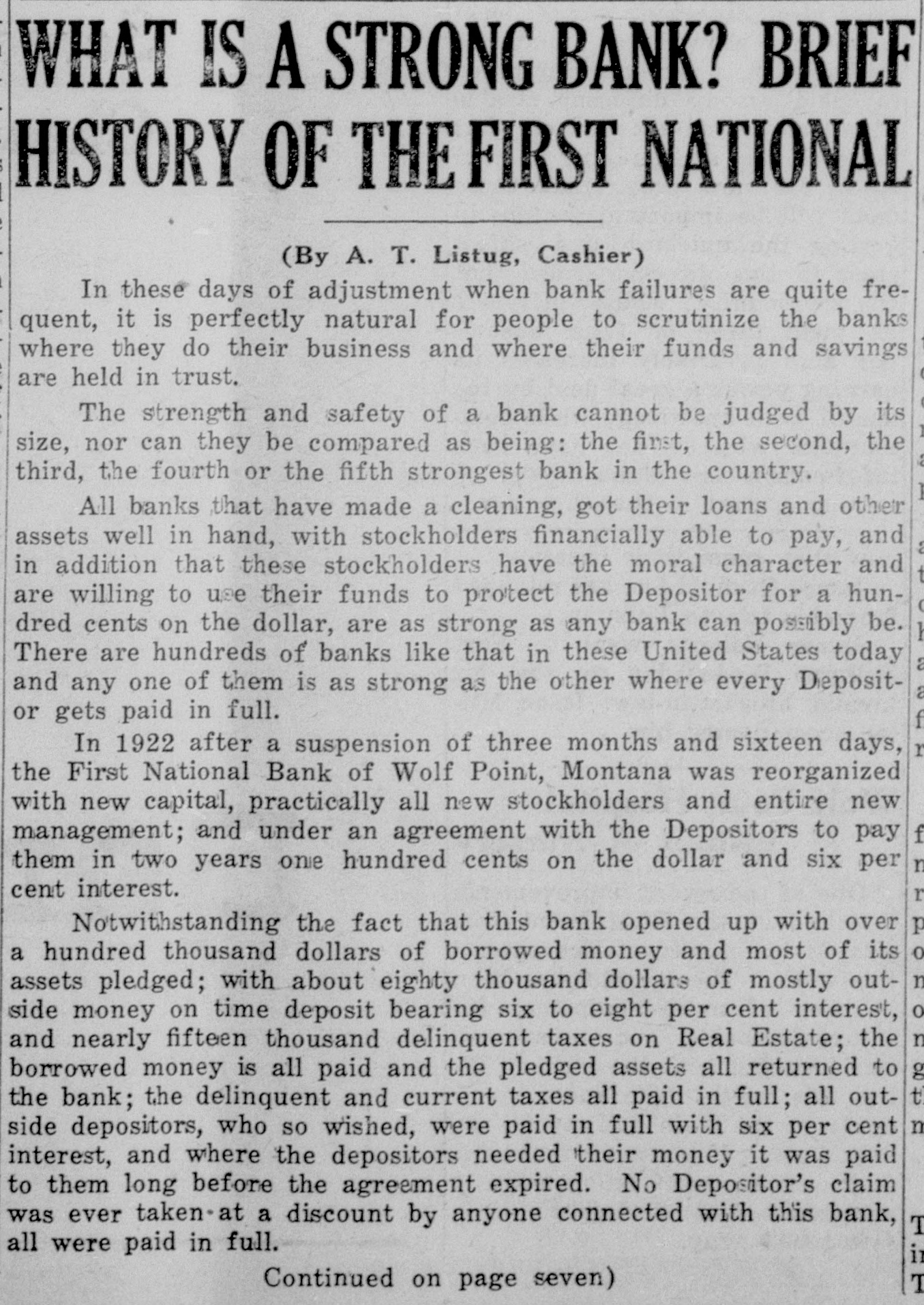

Hobart McLean and Harry Carr were in from the Southside Monday Hemstitching-My machine is at t the Buttrey-Swift store. Belle Gordon FOR SALE-Ford touring car, good condition. Ed Gits, Wolf Point. 26tf A daughter was born to Mr. and Mrs. Arthur Rensvold of the Northside on August 11. Your business, large or small, is always appreciated at "Lloyd's Store' 4-tf Phone 75. Fred Buettner, who farms up north near Tule Creek, was in after harvesting repairs today. Henry L. Lowers from the reservation, was attending to business matters in the city on Tuesday. Harry Carey's most gigantic superpicture "MAN TO MAN" at the Liberty Thursday-Friday. Some picture. B. G. Edgerton, president of the First National Bank, returned Sunday to his home at Oconomowoe, Wis. H. T. Smith has recovered from his recent illness and is again attending to his usual duties at the Mission school. Mrs. D. Stone left on Tuesday morning for Rochester, Minn., where she will enter the Mayo hospital to undergo minor operations. The Presbyterian Ladies Aid Society will be entertained by Mrs. W. L. Young and Mrs. Josiah Martin at the church on August 31. Harry McLeod was in Thursday from West Fork to meet his sister, Marie, on her return from Dillon, where she had been attending summer school. Four high school girls want positions where they can earn their board and room with private families. Address Mrs. F. Beachler, West Fork, 1t Montana. George G. Harvey, one of the prominent young businessmen of Williston, was in the city a couple of days this week representing the Maxwell car. George Maloy from Southwest was in the city on Wednesday taking out supplies. Mr. Maloy stated that threshing would be in full swing in his community next week. R. S. Dalve, of the Walters Drug Co., returned this week from a ten day vacation spent in Great Falls. He also enjoyed trout fishing in the Little Bear Paugh mountains. The Army store moved this week I from the Lamberton building on Main street to the rooms formerly occu. pied by the Wolf Point Promoter in the rear of the Security State bank. d F Tuesday and Wednesday the Libt erty Theatre will show the celebrated t James Oliver Curwood's Northwood production "GOD'S COUNTRY AND I THE WOMAN." Admission only 10 a and 35 cents. S William McConnon received the e sad news of his mother's death on Monday morning, which occured at Winona, Minn. He left on No. 2 the same morning to be in attendance at the funeral. st n Dr. Geo. A. Lhamon, eyesight to specialist, will be at the Sherman 0 Hotel, August 24, one day only. a Have your eyes examined. Thirty a years experience assures you of comA 1-t fortable fitting glasses. h th City Attorney H. A. Schoening, C. P. Swedberg and W. B. DeWitt cr left Monday for Helena to be in attendance at the Masonic Grand Lodge meeting in session there Wednesday and Thursday. ol The First National Bank of Wolf se Point which suspended voluntarily to April 19th, 1922, opened for business y August 7th. The county's deposit ge of $6,646.82, as well as all other deth posits, are worth 100 cents on the se dollar. th Wolf Point elevators are preparng to take care of the bumper crop this fall with the greatest speed posis sible. Kewanee dumps are being inW stalled this week at the Equity eleJo vator and the Wolf Point Grain Co. elevator. tie hi Mrs. loyd Montgomery, Mrs. A. co E. Knights, Mrs. F. E. Rathert and Γ. H. Fox went to Helena Tuesday from the local chanter